Innovation cycles and financial markets

What history teaches us about technological revolutions

This article aims to provide a better understanding of economic transformations, investor behaviour, and financial market dynamics during periods of technological revolution. As history tends to repeat itself, useful lessons can be drawn from previous cycles to perhaps even anticipate certain stages of the current innovation cycle.

Innovation and creative destruction

The history of industrial and technological revolutions is fascinating, rich, and extensively documented. Each of these advances, from the sextant to GPS, the steam locomotive to the automobile, the hot air balloon to aviation, the first machines to automation, and printing to the digital revolution, has profoundly transformed the world and propelled productivity and prosperity.

But such upheavals in work organization and social habits have rarely been met without apprehension and concerns. Trades, business practices and even entire industries have disappeared, swept away by the creative destruction that comes with any wave of profound innovation.

In this context, today’s fears of the artificial intelligence (AI) revolution are neither new nor exceptional.

Investor enthusiasm

At the beginning of each technological innovation cycle, the shares of pioneering companies tend to outperform spectacularly. Amid widespread enthusiasm, investors extrapolate recent returns, driving valuations far beyond economic fundamentals. This dynamic is accompanied by a narrative based on exceptional growth prospects and, recurrently, on the idea of a paradigm shift. Previous valuation benchmarks are then considered obsolete.

The enthusiasm generated by certain companies sometimes resembles a cult. Their leaders become iconic figures, adored by investors and the general public alike, embodying the spirit of progress. Henry Ford was celebrated for his industrial innovations, but also for his visionary management style and his emphasis on human capital. His public image helped make him an icon of industrial capitalism.

Harold Geneen (ITT) in the 1960s and Bill Gates (Microsoft) and Jack Welch (GE) in the 1990s also embodied, each in their own way, charismatic leadership associated with periods of technological and financial expansion. They have often been perceived as visionaries capable of redefining the rules of the game, thus reinforcing narratives of rupture and paradigm shift.

The inevitable arrival of competition

History teaches us that the main risk facing dominant companies during periods of technological revolution lies less in disappointing future growth—as skeptics or “non-believers” argue—than in the emergence of new competitors capable of offering better-performing or lower-cost products. Nokia and Research in Motion (RIM) are prime examples. In 2007, Nokia held 50% of the global mobile phone market share. That was before the arrival of RIM’s BlackBerry and Apple’s iPhone. Similarly, since the arrival of competition, Tesla’s market share has been in sharp decline.

Competition is ruthless

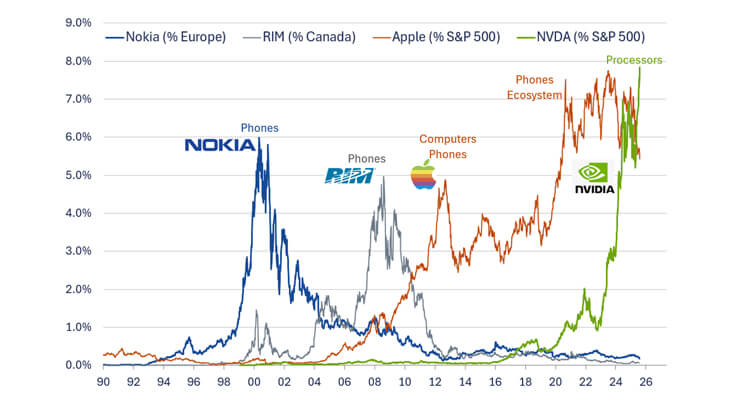

Weighting of securities as a percentage of their respective markets

Sources: DGAM, LSEG, August 2025

Description of the chart of securities as a percentage of their respective markets

This chart shows the weighting of selected stocks in their respective markets: Nokia in Europe, RIM in Canada, Apple and NVDA in the S&P 500 from 1990 to 2025.

A vertical scale shows the percentage, ranging from 0% to 9%.

There are four curves representing the market weighting of a stock over time.

General trends observed

- Nokia dominated until the early 2000s, then declined.

- RIM peaked around 2008 before dropping off.

- Apple has shown steady growth since the 2000s, peaking around 2020.

- NVDA has surged since the late 2010s, reflecting its growing influence in the tech sector.

The spread of new technologies is driving strong demand and attracting a growing number of new players. This is leading to increased competition, overinvestment, and overcapacity. Ultimately, there is downward pressure on the prices of innovative technologies, and the initial benefits become commoditized.

Ultimately, the economic benefits of the technological revolution are captured by companies that have effectively integrated it into their operations. Indeed, history shows that productivity gains tend to shift toward end users, who benefit from more efficient technologies at decreasing costs.

The current innovation cycle: Winners take all, for now

The enthusiasm around AI is prompting investors to take almost unprecedented risks. The valuations of some companies are skyrocketing, driven by the hope that they will dominate the future. This kind of behaviour is not new: we saw it with the railways in the nineteenth century and the digitalization of the economy in the 1990s. Each time, recent trends are extrapolated, and the markets get carried away—that is until they sell off.

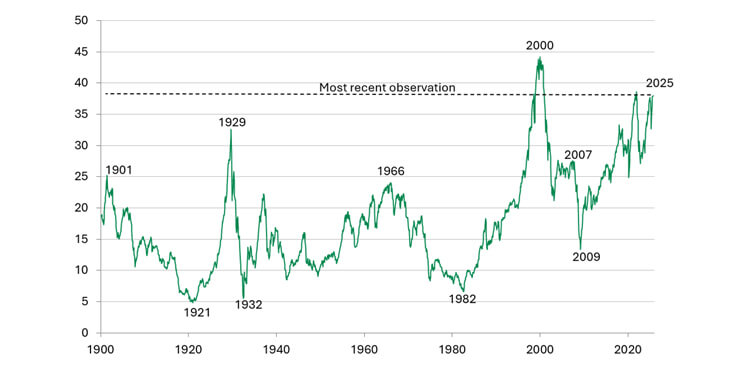

The US stock market has rarely been so expensive

Average S&P 500 P/E ratios in real terms, adjusted for cycles (10 years)

Sources: DGAM, Robert J. Schiller, August 2025

Description of the Chart showing the average S&P 500 P/E ratios in real terms, adjusted for cycles (10 years)

This chart shows the average real price-to-earnings (P/E) ratio of the S&P 500, adjusted over 10 years to account for economic cycles from 1900 to 2025.

A vertical scale shows the real, cycle-adjusted price-to-earnings ratio, from 0 to 50.

A curve corresponds to the fluctuations in price-to-earnings ratio over the years. Each point on the line represents the average real P/E ratio for a given year.

General trends observed

- Significant peaks are seen in 1929, 1966 and 2000.

- In 2025, the ratio approaches 40, indicating historically high market valuations.

How long will this period last, when a few winners seem to be taking it all? It’s hard to say. But history shows that competition inevitably intensifies. Margins tighten, market share fragments and yesterday’s leaders may quickly lose their lead. Big tech companies are unlikely to let Nvidia maintain a monopoly. The arrival of DeepSeek, which challenged the need for chatbots to rely on Nvidia’s high-end products, gave us an early taste in the beginning of 2025. In a single day, Nvidia shed nearly $600 billion of its market cap—the biggest drop ever for a listed company.

The risks of extrapolation

We’re in the early stages of the AI era. There are still many unknowns and variables to consider. At this stage, it’s extremely difficult to distinguish the real long-term benefits for different industries from mere speculation. As technology continues to advance at a rapid pace, this distinction will need to be continually reevaluated.

Current technical challenges are a good example. Today, the energy required to power energy-intensive processors and the water consumption needed to cool them are major issues. In 2000, the challenges were slow bandwidth, the very high cost of data storage, and low computing power. However, these problems were quickly overcome thanks to technological advances.

Extrapolating today’s technologies into the future is a risky, if not naïve, approach. We’ve seen that this is also the case for the competitive environment. Each innovation cycle ends up attracting a multitude of competitors, leading to overcapacity—as was the case with railways or fibre-optic networks. As a matter of fact, China is already said to be experiencing overcapacity in its data centres.

The leaders of the last decade rarely remain the dominant companies

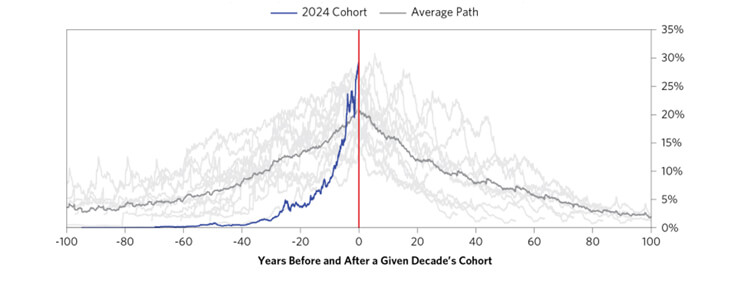

Share of total market capitalization of the top 10 US companies, by decade

Source: Bridgewater, June 2024

Description of the Chart of the share of total market capitalization of the top 10 US companies, by decade

This chart shows the evolution of the market capitalization share of the ten largest U.S. companies, compared across different decade-based cohorts.

Time period covered: From -100 to +100 years around each cohort

A vertical scale shows the percentage (%) of total market capitalization (ranging from 0% to 35%).

Each line represents the market share trajectory of the top ten companies from a given cohort. The blue line shows the 2024 cohort, the black line shows the historical average, and the gray lines represent other cohorts.

General trends observed

- Companies that dominate in one decade tend to lose market share in subsequent decades.

- The 2024 cohort currently holds a high share, but historical patterns suggest this dominance may decline over time.

A competing product doesn’t have to be intrinsically better to capture market share. For instance, it could be 20% less efficient but 40% cheaper and 50% less energy-consuming, or it could be better designed to meet a specific need, such as application-specific integrated circuits (ASIC).

With this hindsight, some recent announcements may be cause for skepticism. The build-out of nuclear power plants to provide energy for data centres raises questions. A power plant takes at least 10 years to build and costs 10 times more than solar or wind. But no one can predict the energy consumption of processors in 2035. Some even go so far as to imagine data centres in space...

The fear of being replaced by a machine

Apocalyptic scenarios abound about the future dominance of AI, especially once artificial general intelligence (AGI) arrives. Whether rightly or wrongly, these themes are popular because our brains naturally pay more attention to negative stimuli due to an evolutionary bias.

The fear of unemployment and “being replaced by a machine” has been a recurring theme in every technological revolution for the past 200 years. But robots and AI can only produce goods and services if there is consumer demand for them. There will likely be creative destruction, productivity gains, and greater prosperity in the long run. But the transition won’t be a purely economic phenomenon for those personally affected by it.

Some occupations will be spared, however. Pink-collar jobs, namely those with a strong relational, empathetic or care component, will be especially resilient to this upheaval. Such jobs will be needed as the aging of the world’s population accelerates over the next 25 years. Skilled trades that require hands-on work and constant adaptation to a varied environment, such as plumbers and electricians, will also be resilient.

Conclusion and implications

The history of innovation cycles calls for a cautious attitude toward today’s giants. Their dominance could be challenged not by pessimistic scenarios but, in the opposite case, by increased competition. Rapid adoption of new technologies across all sectors is creating opportunities elsewhere, especially among end users—a potential that is still poorly reflected in the valuations of mid-cap stocks in particular.

Since January 2025, announcements of investments in AI and data infrastructure have crossed the US$500-billion threshold, driven by a strong commitment by the Trump administration. Although the scale of the projects is unprecedented, their implementation and profitability remain uncertain. Several initiatives seem to be motivated more by geostrategic considerations than by economic logic, particularly the desire of some nations for greater data sovereignty. This dynamic has revived the risk of technological overcapacity, already seen during previous investment cycles.

Moreover, Washington’s isolationist attitude serves as a catalyst for foreign competitors. China’s Huawei and Cambricon, for example, are stepping up their efforts to build an autonomous AI infrastructure, illustrating once again that constraint drives innovation—confirming the adage that necessity is the mother of invention.

Jean-Pierre Couture

Economist and Senior Portfolio Manager

This document was prepared by Desjardins Global Asset Management Inc. (DGAM), for information purposes only. The information included in this document is presented for illustrative and discussion purposes only. The information was obtained from sources that DGAM believes to be reliable, but it is not guaranteed and may be incomplete. The information is current as of the date indicated in this document. DGAM does not assume any obligation whatsoever to update this information or to communicate any new fact concerning the subjects, securities or strategies discussed.

The information presented should not be construed as investment advice, recommendations to buy or sell securities, or recommendations for specific investment strategies. Under no circumstances should this document be considered or used for the purpose of an offer to purchase units in a fund or any other offer of securities in any jurisdiction. Nothing in this document constitutes a declaration that any investment strategy or recommendation contained herein is appropriate for an investor's circumstances. In all cases, investors should conduct their own verification and analysis of this information before taking or refraining to take any action with respect to the securities, strategies and markets that are analyzed in this report.

No investment decisions should be based solely on this document, which is no substitute for due diligence or the required analyses on your part to justify a decision to invest.