Unless you’re lucky enough to win the lottery, saving is a good strategy to achieve your financial goals, even the small ones. Here are 4 tips to help you get motivated to save, stick with it, and get the most out of it.

1. Embrace the joys of saving money

Don’t think about saving as something you only do for things like a house, kids or retirement.

Think about it for the short term, too. It’s an important tool in your life for a lot of different things. And you should start by establishing small, achievable goals. You want to make sure that the amount you need to save is realistic, and that you’ll have it when you need it.

You can—and should—save up for just about anything that you want but you’re not quite ready to go out and buy today. Like new skis or skates. Or for something a little bigger, like a 2-week #VanLife vacation around the Great Lakes.

- Start with a realistic plan, like this one

- Let yourself get rationally exuberant

- Repair, reuse and recycle (local and green!)

- Set achievable goals

It’s tempting, right?

2. Make it a habit

We could go on about savings for hours. But let’s make it quick. You can do yourself a big favour by closing your eyes, using your imagination and visualizing the road to your target:

- Imagine you have a goal and set up an automatic transfer of $50 per week

- That money goes into a separate account or savings plan

- In 1 year (52 weeks), you’ll have $2,600

Now go through that same exercise for your other goals. Just change the amount you’ll need and the time you’ll need to save it. It gives you a pretty accurate picture of what you need to do.

3. Take advantage of compound interest

Making money while you sleep? Why not? Let’s go back to that $2,600 saved up over a year. Maybe you found a great little used car you’re ready to buy. Great, let’s hit the road!

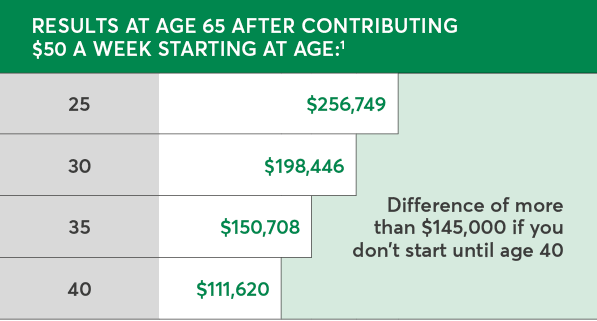

Now let’s also see what happens if you keep saving $50 a week between the ages of 25 and 65. Based on a 4% annual compound rate, you'll accumulate around $250,000. Of that $250,000, about $150,000 will come from interest or returns (the 4%).

Can you forecast returns and interest on your savings?

It all depends on the investment product you have. When you purchase guaranteed investments (like term deposit certificates), you'll know their maturity date and return rate. The principal is also guaranteed at maturity. However, when you invest in the stock market (stocks and mutual funds), returns aren't guaranteed. Depending on your goals, the nature of your investments, your investment horizon and tolerance for market fluctuations, your advisor can help you make any necessary adjustments. You can also contact them if you ever need assistance! Until then, it can be a good idea to get familiar with the pitfalls to avoid.

4. Savings: Put them where it makes sense

You’ve got options. You just need to find the right one for your particular savings goal.

Daily expenses

Think of your everyday account as your main account. You use it to manage your daily transactions, deposit money, make withdrawals, send or receive transfers, pay bills and deposit cheques.

- Ideal for regular banking and everyday expenses

- Zero interest, so only keep as much in there as you need

You can use this account for small purchases or everyday payments that you don't have to save up for.

Short-term goals

If you’re saving a few dollars because you became a home baker this past year, or if you need to start saving for a new game console, try the Savings goals tool, available on AccèsD.

- Choose the project you want to save for

- Set your goal (for example, a total of $3,000)

- Slect the account in which your project amount will accumulate

- Set the amount and frequency for your automatic transfers

TFSA, for the medium or long term

A tax-free savings account (TFSA) is a tax-sheltered plan that lets you save money and earn interest without paying tax. You can choose a savings or investment product within the account depending on your goals, plans and investor profile. What's more, the best thing about a TFSA is that any withdrawals you make aren't taxed. They're also added back to your contribution room the following year.

- Perfect for medium- or long-term goals

- Withdrawals aren’t taxable

- Annual contribution limit

You can use the account to save up for anything from a new car to a dream vacation!

Planning to buy your first home? Consider contributing to an FHSA.

If becoming a homeowner is one of your goals, you might want to consider opening a tax-free first home savings account (FHSA). It's a great way to save up for a down payment on your first home. You can also combine this savings vehicle with the Home Buyers' Plan (HBP).

Are RRSPs worth it?

A registered retirement savings plan (RRSP) is a long-term savings solution that uses the magic of compound interest. Any amounts you withdraw from an RRSP are taxed, except in these 2 circumstances:2

- For example, to buy your first home: withdraw up to $60,000 tax-free, but refundable, to make a down payment (Home Buyers’ Plan, or HBP)

- To go back to school: withdraw up to $20,000, tax-free but refundable, thanks to the Lifelong Learning Plan (LLP).

You can access your money long before you retire! There are a lot of reasons to start contributing to an RRSP as soon as possible.

After a few months or years, you’ll reap the benefits of your discipline. Well done! Saving can be a long road with some tempting off ramps along the way. But staying the course can really pay off.

1. Example based on an estimated 4% annual compound rate and a balanced portfolio (50% fixed-income securities and 50% equities).

2. Certain terms and conditions apply.

1. Example based on an estimated 4% annual compound rate and a balanced portfolio (50% fixed-income securities and 50% equities).

2. Certain terms and conditions apply.