- Francis Généreux

Principal Economist

Economic News

US Real GDP Growth Comes in Lower than Expected, but Consumer Spending Holds Up

January 30, 2025

Highlights

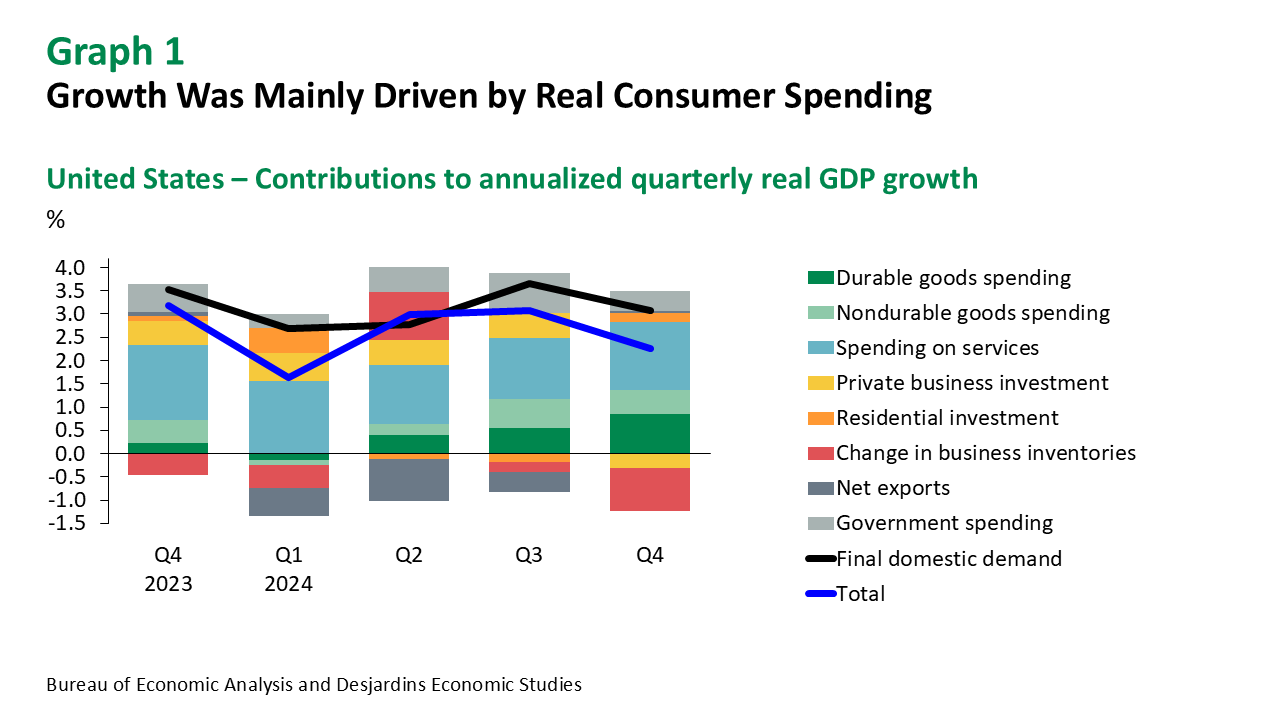

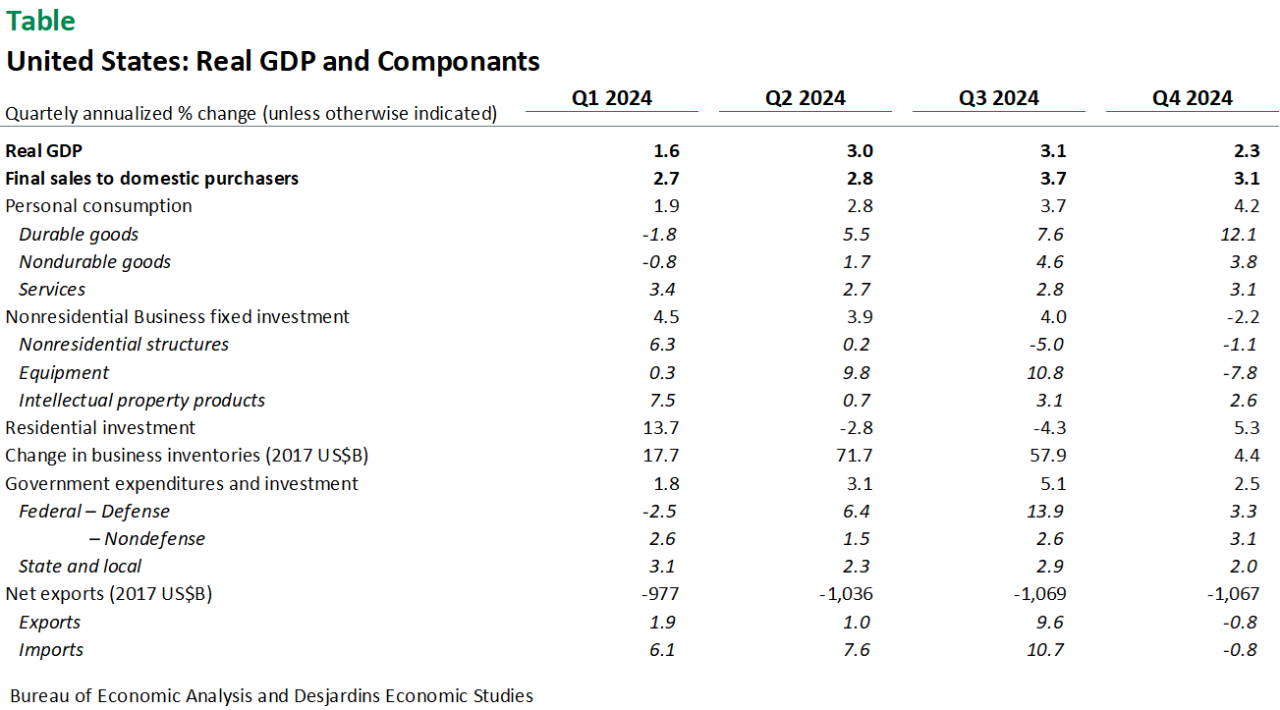

- According to the advance estimate released by the U.S. Bureau of Economic Analysis, real GDP increased at an annualized rate of 2.3% in the fourth quarter of 2024. This was lower than the gains of 3.1% in the third quarter and 3.0% in the second.

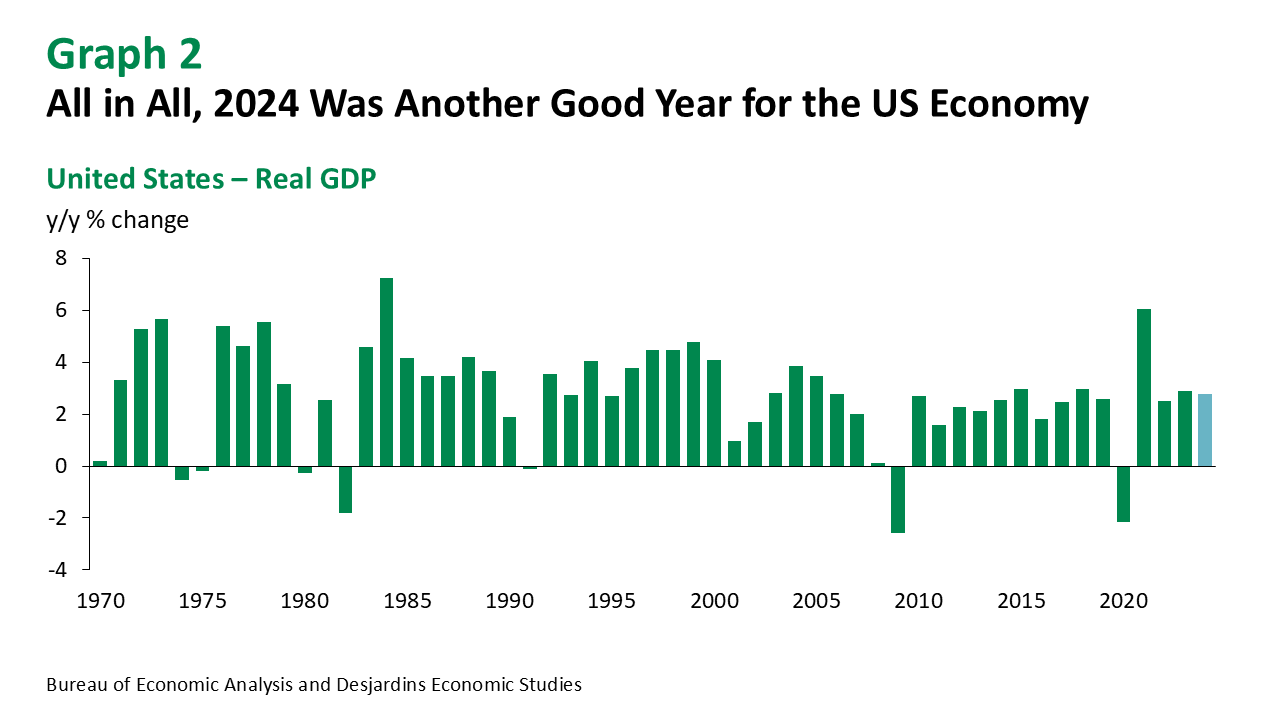

- For the year, real GDP expanded 2.8% after posting growth of 2.9% in 2023.

Comments

The fourth quarter result was the slowest US economic growth we’ve seen since the first quarter of 2024, but an annualized gain of 2.3% is anything but poor. Final domestic demand rose 3.1% in the fourth quarter, another solid showing after the previous quarter’s 3.7%.

Within domestic demand, real consumer spending made a healthy contribution. This component accounts for more than 70% of GDP, and its 4.2% annualized growth is the highest since the first quarter of 2023. This performance from consumers was remarkable amid persistently high interest rates and faltering confidence levels ahead of the election. The resilience of the labour market and income—real disposable income increased at an annualized rate of 2.8% in the fourth quarter—clearly helped.

However, business investment was more disappointing. Nonresidential construction fell for the second consecutive quarter, while the surge in construction investment from the US manufacturing sector over the past few years has now petered out. Spending on equipment declined, likely due to a pullback after two strong quarters. However, the strike that affected the aerospace sector clearly had an impact. Even the 2.6% rise in investment in intellectual property products was disappointing, as this figure has historically been higher. The change in private inventories, which fell from US$57.9B to just US$4.4B in 2017 dollars, detracted from growth. We would have thought that concerns that the new Trump administration would impose tariffs sooner or later would have encouraged companies to build up their inventories, but they didn’t. The drag from this component—it shaved 0.93 points off fourth-quarter real GDP growth—is both surprising and disappointing. This may only be a postponement as the imminent threat of US tariffs remains. At the same time, the decline in both exports and imports in the fourth quarter was unexpected.

Government spending made a slight positive contribution to real GDP growth in the fourth quarter. However, growth in military spending was lower at 3.3% after 13.9% in the third quarter. It remains to be seen whether the numbers will change much in early 2025 given the flurry of recent announcements by the new Trump administration.

US real GDP growth remained strong overall in 2024 and continues to outpace the other major advanced economies. Eurozone real GDP only grew 0.7% in 2024. Of course, President Trump’s policies, starting with the possibility of higher tariffs, are the wildcard that will impact where we go from here.

Implications

US real GDP growth was somewhat disappointing in the last quarter of 2024. Consumption remains strong, but businesses appear more cautious. Temporary effects may have had an impact, but other disruptors could also generate uncertainty in 2025.