- Francis Généreux

Principal Economist

Essentials of Monetary Policy

The Federal Reserve Delivers Another Rate Cut, but a Pause Now Appears Likely

December 10, 2025

According to the Federal Reserve (Fed)

- The Fed lowered its policy rates by 25 basis points. The target range for the federal funds rate now stands between 3.50% and 3.75%.

- Available indicators suggest that economic activity has been expanding at a moderate pace. Job gains have slowed this year, and the unemployment rate has edged up through September. More recent indicators are consistent with these developments. Inflation has moved up since earlier in the year and remains somewhat elevated.

- In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee is attentive to the risks to both sides of its dual mandate and judges that downside risks to employment rose in recent months.

Comments

The Fed’s decision appears to have been somewhat more difficult this time. While it was clear during the previous two meetings that it would opt for a 25‑basis‑point cut to its policy rate, the current circumstances introduced a bit more uncertainty. That said, the consensus still anticipated a rate cut, though with less unanimity than in September or October. There were also more signs of dissent within the Federal Open Market Committee. Nine members voted in favor of the cut, while two preferred to hold rates steady and another favored a deeper 50‑basis‑point reduction.

It is worth recalling that the Fed had to drive through the fog, to use the expression employed by Chair Jerome Powell in October. The absence of numerous official indicators from the federal government beyond September, as well as the lack of third‑quarter real GDP data, meant that policymakers had to make their decision without having all the information at hand. Certainly, other indicators remain available and the Fed can rely on its extensive network of contacts, but the impact of the shutdown on data releases was likely mentioned repeatedly during the meeting.

Alongside today’s decision, the Fed released its updated projections. These show little change compared to September. The main revision is a more optimistic outlook for real GDP growth at the end of 2026, which is now expected to reach 2.3%, up from 1.8% (reflecting a post‑shutdown rebound). At the same time, headline inflation for the end of 2026 was revised slightly lower. Meanwhile, projections for the unemployment rate, core inflation, and both real GDP and headline inflation for 2027 and 2028 remain largely unchanged. The forecast for the federal funds rate is also unchanged from September, still calling for one 25‑basis‑point cut in 2026 and another in 2027.

In his press conference, Jerome Powell reiterated that the situation remains challenging for the Fed, with risks to inflation tilted to the upside (at least temporarily) and risks to employment tilted to the downside—and deteriorating in recent months. Under these circumstances, the Fed is likely to remain cautious. While Powell again emphasized that decisions will be made meeting by meeting and that there is no predetermined path for monetary policy, it seems increasingly plausible that a pause in rate cuts could be on the horizon. The limited changes in today’s statement compared to October, along with the Fed’s projections, point in that direction. Powell’s responses to journalists’ questions also suggested a willingness to wait. That said, the Fed will receive several key indicators before its next meeting, which could change the outlook—especially if the labor market continues to show signs of weakening.

Implications

The Fed has lowered rates by 25 basis points three times since late summer. As it approaches the neutral rate, it now has room to wait and see how the economy evolves, particularly if labor market conditions worsen further or if the Trump administration’s protectionist policies exert more upward pressure on inflation. A pause in rate cuts therefore appears likely during the first half of 2026.

2025 Schedule of Central Bank Meetings

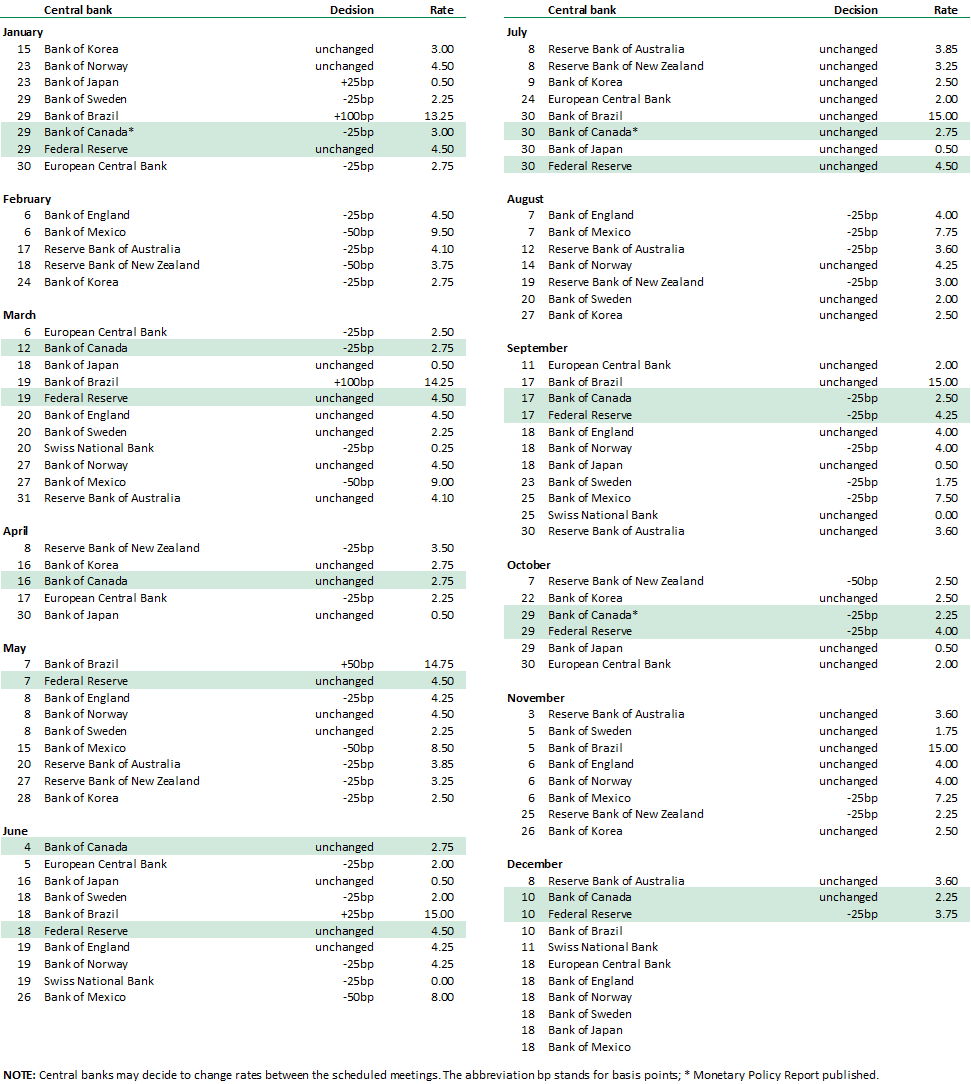

2026 Schedule of Central Bank Meetings