- Francis Généreux

Principal Economist

Economic News

United States: September’s (Delayed) Results Show a Modest Improvement in Hiring

November 20, 2025

Highlights

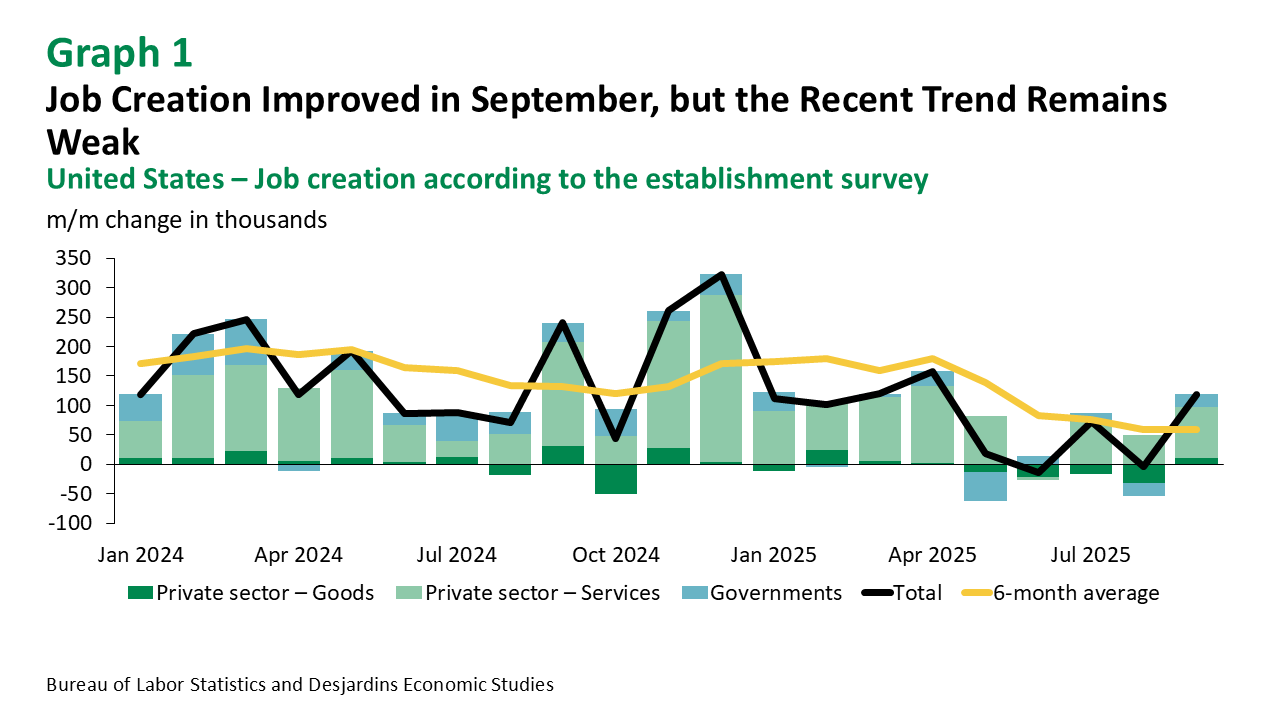

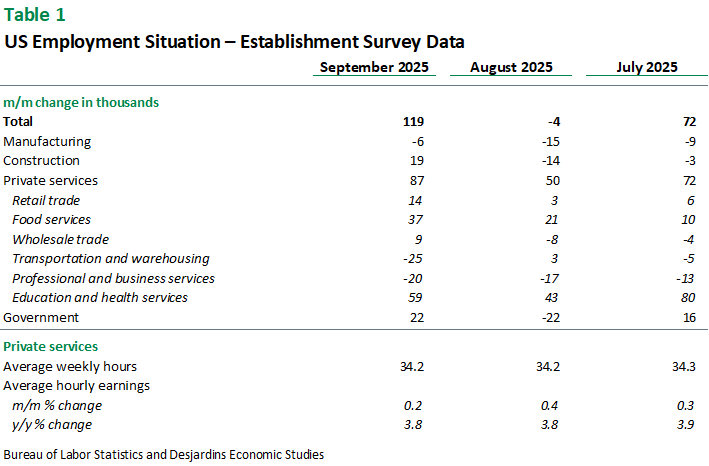

- The establishment survey indicates a net gain of 119,000 jobs in September, following net layoffs of 4,000 workers in August (revised from +22,000) and a gain of 72,000 in July (revised from +79,000).

- Average hourly earnings rose 0.2% in September. The year-over-year change held steady at 3.8%.

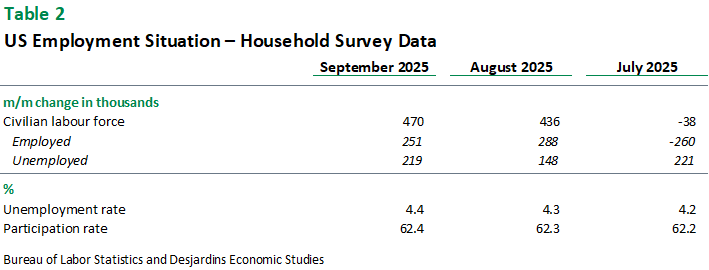

- The unemployment rate increased from 4.3% in August to 4.4% in September, its highest level since October 2021.

Comments

Due to the budget impasse, this labor market report was long overdue. At least the news is relatively positive. The 119,000‑job gain is more than double the consensus forecast (+51,000). Even the household survey, despite the uptick in the unemployment rate, looks solid thanks to a healthy increase in labour force participation and job creation.

Gains were also fairly broad-based in the establishment survey. The share of the 250 tracked industries reporting higher employment rose from 49.0% in August to 55.6% in September—the highest proportion since last February. Construction posted its first monthly increase in employment since May and its strongest gain in a year.

However, that’s where the good news ends. There are also signs of weakness, even concern, in the September data. Manufacturing—a sector prized by the Trump administration—recorded its fifth consecutive month of net job losses, totaling 58,000 positions shed since May. Previous results of overall job creation were revised downward and continues to fluctuate, with net contractions in June and August. The 6‑month average for net job gains stood at just 58,500 in September, half the level seen a year ago. Finally, the unusually mild weather in September, with no tropical storms making landfall in the United States, may have provided a boost.

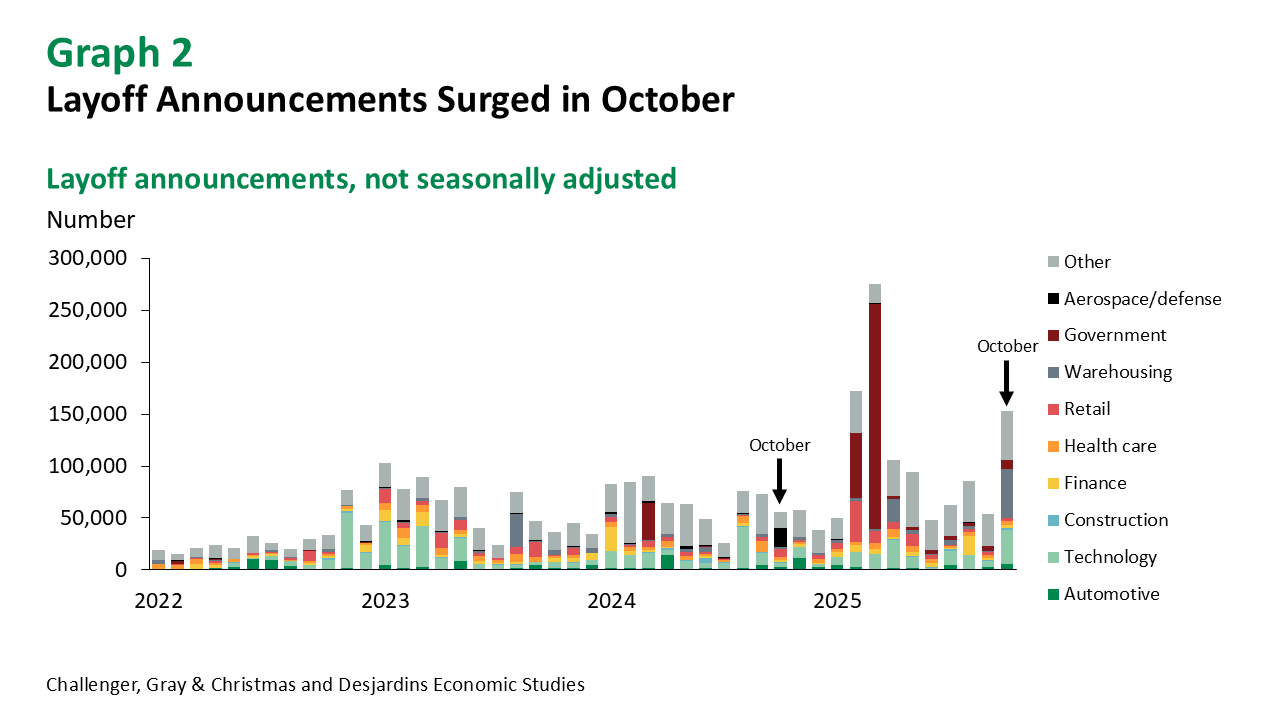

It’s important to remember these figures are for September only—data we should have received on Friday, October 3, 48 days ago. Since then, the longest budget standoff on record has temporarily affected the economy and labour market. We also know that net hiring likely weakened significantly in October due to earlier federal government layoffs that will be reflected after a grace period. We’ll have to wait nearly another month for fresh labor market results. October’s establishment survey data won’t be released until December 16, alongside November’s figures, and there will be no household survey results for October. With no official employment numbers available before the next Federal Reserve meeting, attention will remain on alternative indicators. For now, we know that layoff announcements surged in October and the ADP survey shows relatively weak private-sector job creation. However, initial jobless claims remain fairly stable.

Implications

September’s job creation exceeded consensus expectations, and even the rise in the unemployment rate doesn’t look overly troubling. That said, the delay in publishing these figures limits their usefulness. The coming months—particularly October—are likely to be weaker, continuing the recent stop-and-go pattern in hiring.