- Jimmy Jean, Vice-President, Chief Economist and Strategist

Tiago Figueiredo, Macro Strategist • Oskar Stone, Analyst

Investment Strategy and Interest Rate Analysis

Downside Risks Remain at the Forefront Heading into 2026

December 9, 2025

Economic Trends and Interest Rates

Most developed market (DM) central banks are expected to finish normalizing interest rates in 2026. Deficit spending, moderating inflation, and geopolitical and fiscal risks will also be common drivers of DM rates next year. In the UK, bonds should benefit from continued Bank of England easing. While the recent budget helped compress risk premiums, fiscal sustainability remains a concern, and we maintain a bias toward further curve steepening. In Europe, the central bank is likely to stay on hold, with risks tilted toward additional easing. Defence and infrastructure spending will remain key priorities, particularly outside Germany where consensus is harder to achieve. Political uncertainty in France also warrants attention, leaving us neutral on euro fixed income. Japan is unlikely to break trend, with policymakers continuing to raise rates as inflation remains elevated, wage growth accelerates and fiscal reforms are introduced. JGBs remain under pressure, but given historically steep curves, we expect flattening from current levels.

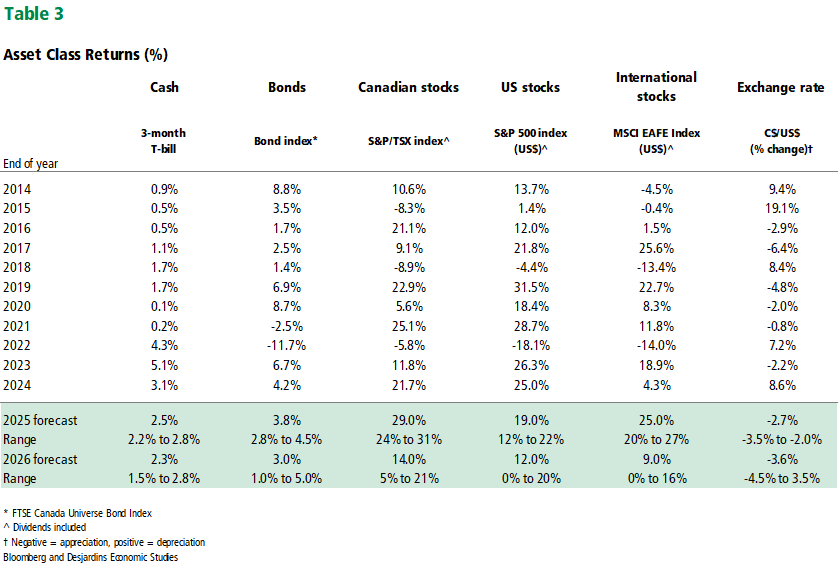

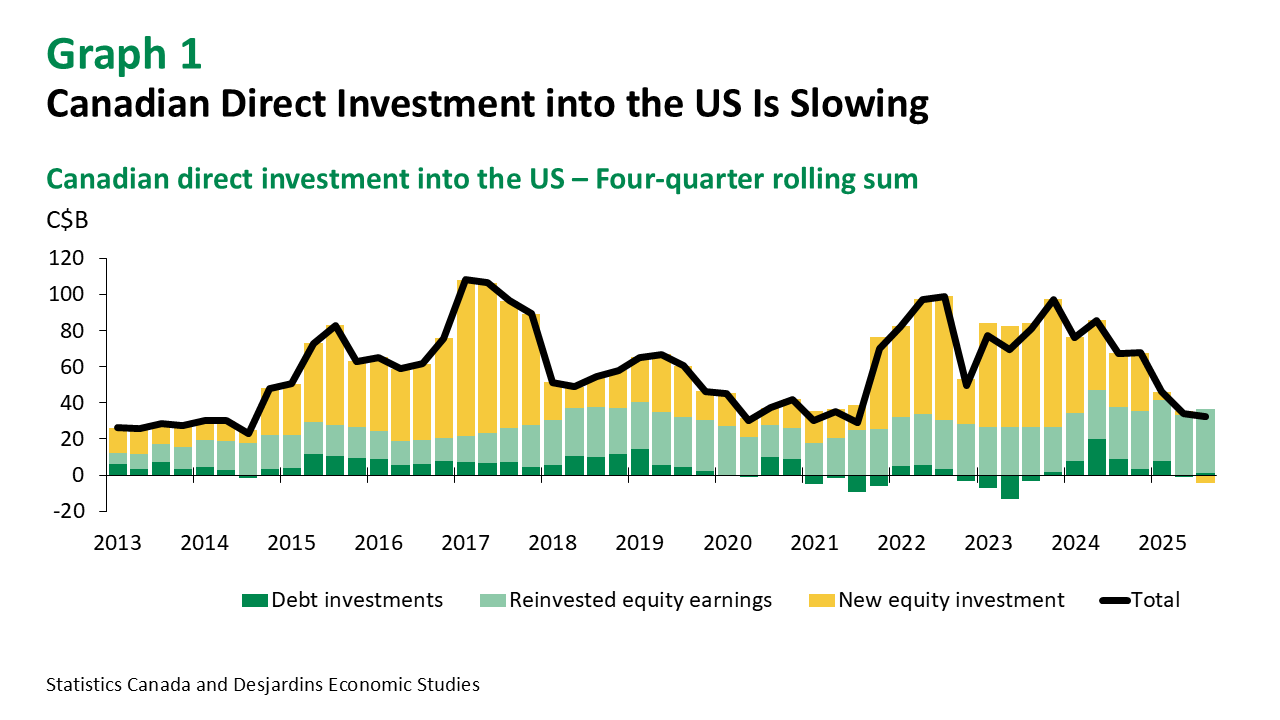

Canada is unlikely to be a major source of volatility in 2026. Budget 2025 preserved fiscal stability in the near term, with defence spending commitments set to roll out gradually. Accelerated approvals for national infrastructure projects may support business investment over the long run. Foreign direct investment (FDI) into Canada has been improving, and more notably, FDI from Canada into the US has been slowing (graph 1). Most fiscal stimulus won’t begin to impact the economy until the second half of the year. We expect the Bank of Canada to remain on hold, though further labour market deterioration could create room for additional easing in the first half. Overall, we see curves reaching peak steepness early in the year before flattening as markets start to price in the first rate hike.

Flows into Canadian bonds are expected to slow but remain resilient. The Bank of Canada’s easing cycle provided a strong tailwind in 2025, but as the likelihood of further cuts fades, front-end demand should moderate. Further out the curve, however, we see continued scope for investors to add exposure. Longer-dated yields are likely to remain broadly stable throughout the year, while term premiums should compress from elevated levels—particularly if fiscal surprises are avoided in the spring update (graph 2).

A range of risks complicates the outlook for US rates, but we expect yields to decline further and the curve to steepen by the end of 2026. The path lower will not be linear. Following the December FOMC meeting—where we anticipate another 25bp cut—the Fed is likely to remain on hold through the first half of the year. Policymakers remain concerned that inflationary pressures, driven by past tariffs and new sector-specific measures, could push consumer prices higher in 2026. Inflation derivatives continue to price in notable upside risks. Unless the labour market deteriorates unexpectedly, we see the Fed shifting its focus back toward inflation in 2026.

Central bank balance sheet policy will probably turn less restrictive in 2026. The Bank of Canada has already ended quantitative tightening (QT) and will begin purchasing treasury bills by the end of the year, with a return to the GoC bond market likely deferred until 2027. The Fed is in a similar position, having concluded QT and shifted to reinvesting maturing mortgage-backed securities into Treasury bills. Persistent funding pressures and recent Fed commentary suggest balance sheet growth could resume before year-end. The ECB and BoE appear comfortable with the current pace of runoff, while the BoJ may accelerate QT next year. Although central banks are no longer the dominant buyers of government bonds, their retreat leaves pricing to other investors, who demand fair value. This shift in ownership should keep upward pressure on global yields in 2026. Issuance plans will be closely watched, particularly in the US, where an extension of weighted average maturity (WAM) is widely expected. Shifting issuance towards longer-dated securities would add to duration supply and reinforce our view of higher long-end yields and continued curve steepening.

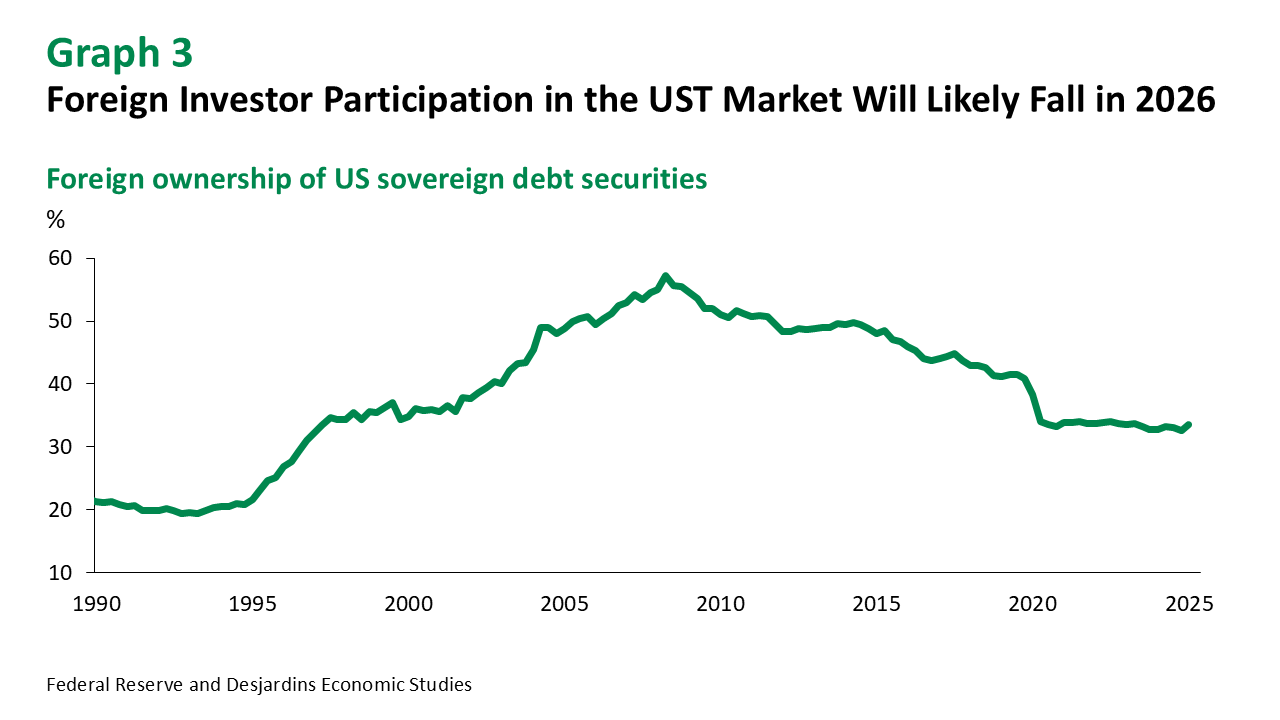

The rotation away from US Treasuries is likely to remain a key theme in 2026. Foreign participation in USTs should continue to decline as investors seek safety in other markets (graph 3). The outlook for term premium is less clear, with the Fed’s potential return to the UST market likely to dampen that measure. Outright sales of Treasuries remain unlikely, as US debt is still the primary conduit for recycled USD export proceeds and the preferred global savings vehicle. However, the marginal dollar now has alternatives—for example, higher JGB yields raise the hurdle for additional investment from Japan. Importantly, however, we see the bar for rotation away from US corporate credit and equities to be much higher than the bar for rotation away from US Treasuries.

Exchange Rates

We continue to see the Canadian dollar strengthening in 2026, although this should manifest more in the second half of the year. While USMCA negotiations are likely to weigh on the Canadian dollar in the first half, once negotiations conclude and the path forward becomes clear, the uncertainty premium weighing on the loonie should dissipate.

Equities and Credit

Heading into 2026, we remain constructive on equities and expect the performance gap between the US and the rest of the world to narrow. The consensus anticipates a broadening of earnings growth. We share that view, although we are slightly less optimistic on overall earnings growth. The US is likely to avoid recession, and with midterm elections in the fall, significant shifts in economic policy appear less probable. Federal Reserve easing, particularly in the second half, should provide additional support for valuations.

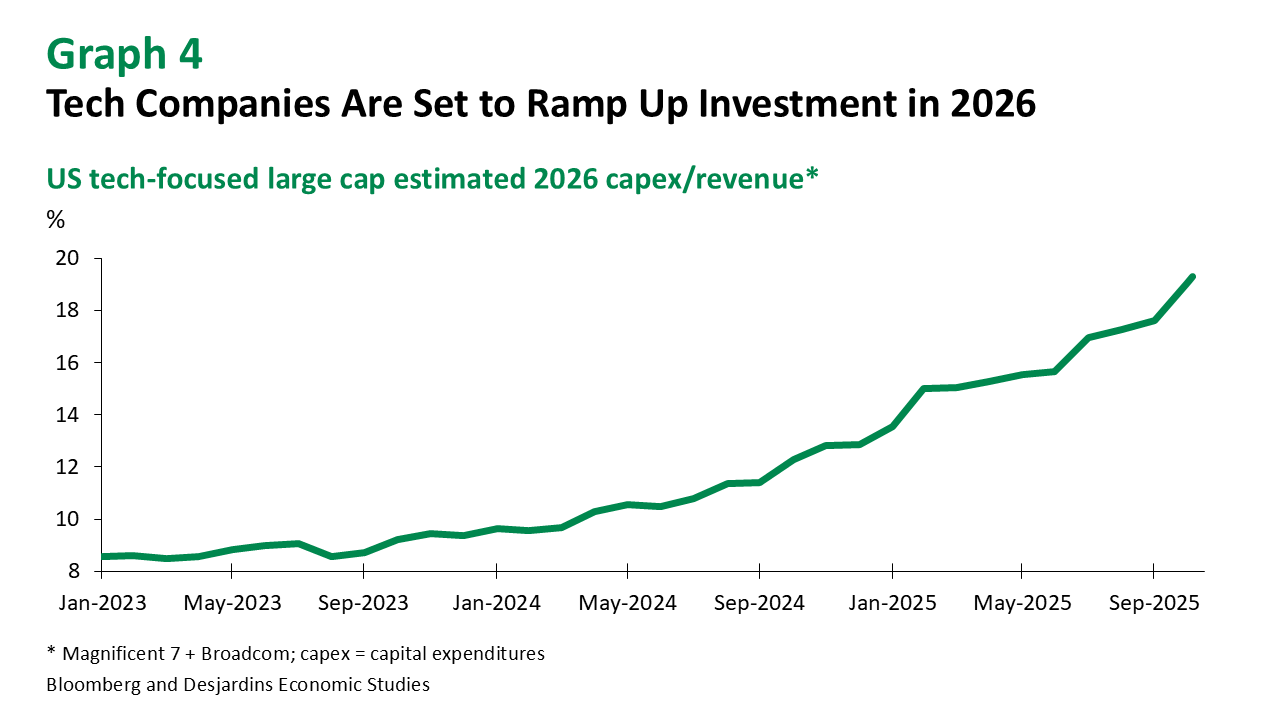

While the AI infrastructure buildout should continue to drive returns in 2026, it also introduces downside risks. The path from AI infrastructure investment to realized earnings remains unclear, leaving equities vulnerable to disappointment on adoption timelines or monetization metrics. Beyond adoption, there is also the risk of a reshuffling within the AI hierarchy. While success by some companies does not necessarily come at the expense of others, markets are likely to trade it that way in the near term—as evidenced by the performance gap between Alphabet and NVIDIA in November. Meanwhile, rising debt issuance among hyperscalers (i.e., tech companies making large investments in AI infrastructure) underscores the growing need to deliver earnings growth in 2026, particularly as capex spending intentions have surged relative to projected revenue (graph 4).

The recent market volatility appears driven more by profit-taking than by fundamental concerns. With year-to-date equity returns ranking in the top percentiles, the surge in tech bond issuance this fall likely provided investors with an opportunity to lock in gains. Excluding the move in Oracle credit default swaps—which seems idiosyncratic—other names are trading at or slightly above spreads on the broader investment-grade CDX index, which itself remains very tight. As such, we are not alarmed by the recent choppiness and remain constructive into year-end, though any rally is likely to be a gradual grind higher.

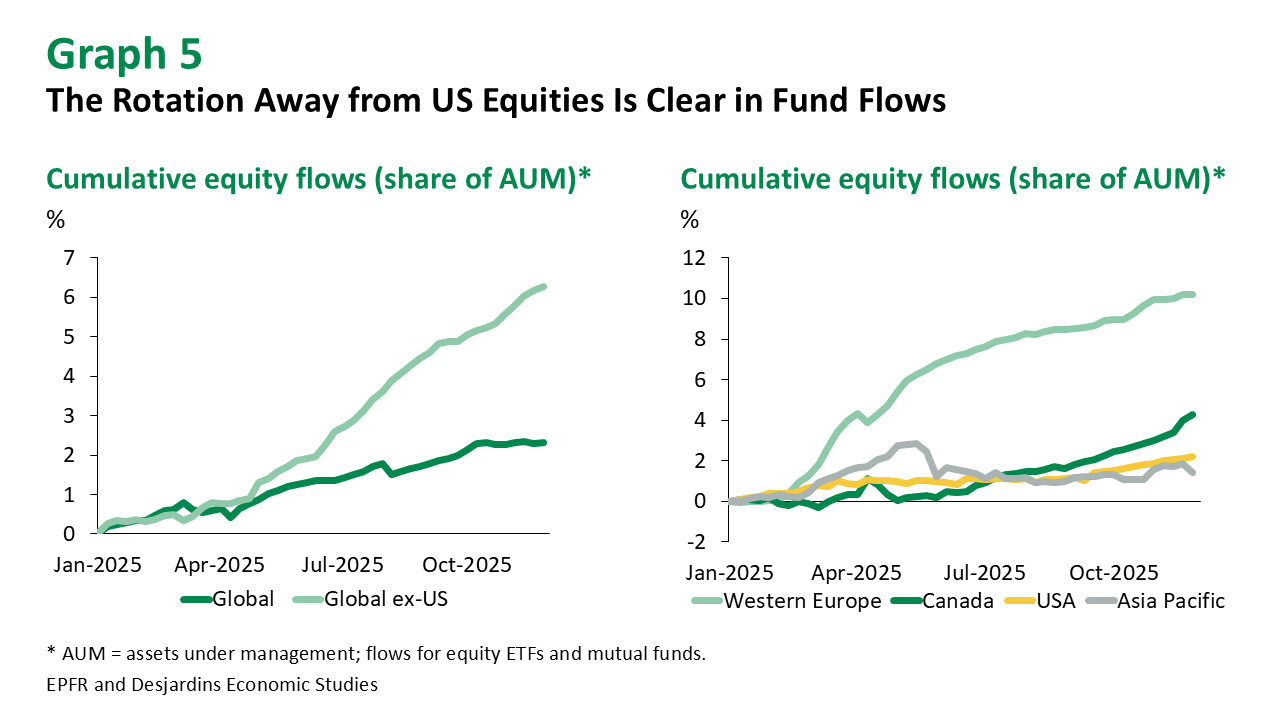

Diversification away from tech-heavy US indices is likely to continue in 2026. Elevated commodity prices should benefit markets with greater exposure to resource sectors, supporting our view that the TSX will outperform the S&P 500. Canadian banks add to the TSX’s appeal, having navigated the mortgage renewal cycle with relative ease so far thanks to the aggressive cutting cycle from the Bank of Canada. Mutual fund and ETF flows into Canadian equities have already outpaced flows into the equities of other jurisdictions, and we see scope for this trend to persist into next year (graph 5). With policy becoming increasingly focused on domestic issues worldwide, equity markets have become less synchronized—a dynamic that should continue to drive asset allocation away from the US at the margin.

Investors should continue to look beyond bonds for diversification. While stock–bond correlations have turned negative, markets are still pricing in a significant premium on upside inflation risks. Recently, part of that premium has been driven by concerns that AI data centres could strain energy markets in the future. Managing commodity exposure—whether direct or indirect—will remain a critical component of asset allocation. Periods of prolonged market stability despite policy uncertainty, as seen this summer, also present opportunities to secure inexpensive downside hedges.

Looking ahead, two key risks stand out. First, the US economy could prove significantly weaker than expected. In that scenario, bonds would likely outperform, but equities could face a sharper correction than usual. Much of this stems from the likelihood that economic weakness would delay AI adoption as companies tighten spending. Second, the AI theme itself has become highly concentrated. With US equities accounting for roughly 65% of the MSCI World Index and household wealth heavily concentrated in stocks, any meaningful decline in leading AI names could quickly morph into a broader market event. Heightened concentration within US indices amplifies this risk, making the trajectory of AI-driven growth a critical factor for global markets in 2026.