- Jimmy Jean, Vice-President, Chief Economist and Strategist

Mirza Shaheryar Baig, Foreign Exchange Strategist

FX Analysis

Stay the Course

January 15, 2026

Highlights

- The US dollar is set to weaken broadly this year as the greenback loses its yield advantage, making it cheaper for asset managers to raise hedges.

- CAD may be soft in Q1 on trade-related uncertainty. But the loonie is poised for solid gains, assuming positive momentum on the CUSMA review.

- The eurozone outlook is lacklustre, with downside risks. We expect EUR to weaken on crosses like EURCAD, EURAUD and EURCNY.

- Japanese authorities are increasingly uncomfortable about rising bond yields and the falling yen. Intervention risks are rising. Meanwhile CNY gains are likely to extend as authorities signal a desire for exporters to move up the value chain.

- MXN fundamentals remain supportive, but speculative long positioning is now worryingly high.

Overview

Despite volatility early in the year, we expect the loonie to rebound broadly in 2026, supported by tighter rate differentials, rising commodity prices and government measures to spur business investment. We maintain our forecast for a weaker US dollar this year, although it will come with a rotation away from European currencies towards commodity and emerging market currencies.

USD

Losing Support

Since “Liberation Day,” most economists have revised their US growth forecasts higher while remaining cautious on other advanced economies. Two points stand out:

- First, given the starting point, there is considerable room for the US to disappoint—or for other economies to exceed expectations. Markets typically react when expectations change, not when they are simply met.

- Second, the US dollar fell sharply when US growth expectations collapsed in Q2 last year, but it merely traded sideways when expectations recovered. This points to an asymmetric sensitivity: in the current regime, the greenback is reacting more sharply to downgrades than to upgrades.

This comes down to the fact that the market is very long US dollars. Many non‑US institutional investors are overweight US equities, typically with low forex hedge ratios. In addition, the Fed’s reaction function is skewed in a similar way: large cuts if the labour market weakens versus modest cuts if conditions remain stable. Either way, the bias is toward lower US rates.

We maintain our forecast for a weaker USD vs. most currencies in 2026.

CAD

Shifting Stronger, Avoiding Landmines

The Canadian dollar strengthened in December on narrowing interest rate differentials implied by forwards but retraced some of those gains in the new year due to worries of a potential oil supply glut south of the border. This highlights the ongoing tug of war between fundamentals and political noise, which should remain a key feature of markets in 2026.

Our story is broadly unchanged: We expect the loonie to extend gains against most currencies, but the path won’t be smooth. Investors should be ready for noise around the CUSMA review and a soft economy. But assuming positive momentum, more clarity on the trade deal should spur business investment. Furthermore, Canadian asset managers are likely to increase forex hedge ratios as the cost of hedging is set to cheapen this year on the back of Fed rate cuts.

What if Western Canadian Select prices fall even further, particularly if Venezuelan oil exports are diverted to the United States? Our economics colleagues argue that fear may be overstated External link.. Moreover, Canada’s energy exports are shifting too. Crude oil flows through the TMX pipeline now feed refineries in China, where they command a premium over WCS. And LNG exports to the Asia‑Pacific region should surge this year as the LNG Canada facility in Kitimat, BC, ramps up to full capacity. This points to greater resilience of energy exports. Above all, there seems to be a growing political consensus around investing in east–west energy corridors to reduce reliance on the US market.

We expect USDCAD to be volatile in Q1 on trade headlines, but trend lower thereafter, assuming there is more clarity on trade talks ahead of the July deadline for CUSMA review. We have upgraded our year-end forecast slightly to 1.34 from 1.35 and see the pair falling below 1.30 by the end of 2027.

EUR

Shine Wears Off

Little has changed since our update in December. We remain of the view that the eurozone will muddle through, though there are downside fiscal and political risks to the outlook.

We expect a lacklustre year in the euro area, with growth between 1.0% and 1.5%. Fiscal risks lurk in the background as a number of potential crisis triggers remain unresolved, namely high public debt, rising NATO spending commitments, Ukraine war cost burden (which the US has largely passed on to European allies), policy paralysis in France and an unstable coalition government in Germany. Moreover, Europe is short energy and remains vulnerable to supply disruptions and a rebound in oil prices.

The ECB has signalled that its easing cycle is likely over, with the possibility that rising inflation or geopolitical pressures could tip the balance toward tightening later in 2026.

Against that backdrop, we believe the euro is overvalued. It outperformed most G10 peers last year, which we expect will reverse this year. In other words, we forecast euro weakness on crosses like EURCAD, EURAUD and EURCNY. We expect the euro will track sideways against the US dollar—strengthening on bouts of USD weakness, then retreating as fiscal and political risks resurface.

We continue to expect a broad range in EURUSD between 1.15 and 1.20 in 2026, but some weakness in EUR vs. CAD and other major currencies.

JPY

Intervention Risks Are Mounting

The tension created by the simultaneous collapse in JGBs and the yen is approaching a critical point. We believe the risk of a joint intervention in FX and bonds has increased significantly.

Ten-year JGB yields have surged by about 40 basis points over the past two months. Unlike the very long end, where yields have been climbing for some time but has sparse debt outstanding, the 10‑year tenor is critical for the Ministry of Finance, as it represents the point where the government refinances most of its obligations. We estimate that every 10bps rise in Japan’s weighted average maturity debt (around 9Y) would add ¥1.2 trillion or 0.2% of GDP to the cost of debt servicing.

Meanwhile USDJPY remains perilously close to last year’s high despite repeated verbal intervention from authorities. Indeed, negative real rates in yen deposits and higher rates in the US have encouraged market participants to use the yen as a funder.

We expect authorities will use a combination of tools to stabilize the bond and FX markets. There may be direct intervention in the FX market to establish a ceiling in USDJPY around 160, while Japanese public pension funds may be encouraged to buy JGBs, which now earn positive ex-ante real rates (nominal bond yields minus break-even implied inflation).

Finally, key members of PM Takaichi’s growth council have offered public support for the BoJ’s policy normalization since last month, signalling greater latitude for the Bank to raise interest rates.

We maintain our year-end USDJPY forecast of 150. Authorities are becoming uncomfortable with the simultaneous fall in JGBs and the yen and may intervene directly or indirectly in the coming weeks.

CNY

Involuntary “Involution”

We remain optimistic on the CNY. In recent notes we have argued that China will tolerate a sizable ~5% appreciation of its nearly pegged currency. The CNY moved strongly higher in December, and we think there is more in store for 2026. Despite recent gains, the PBoC’s trade-weighted “CFETS” basket has only managed to recover last year’s losses.

The story is relatively simple: China’s trade surplus is surging despite US tariffs thanks to the global competitiveness of Chinese car and battery companies and deepening ties with the Global South. Narrowing rate differentials have reduced the cost of hedging for exporters, which is encouraging more of them to hedge or settle their forex earnings.

Moreover, the government’s “anti-involution” campaign—which aims to discourage self-defeating price wars in strategically important industries—has now become part of the currency calculus. Authorities have often signalled to exporters that they cannot rely on a cheap currency forever and should move up the value chain. The recent appreciation has driven home that point.

We maintain our forecast of 6.75 and 6.50 for 2026 and 2027, respectively.

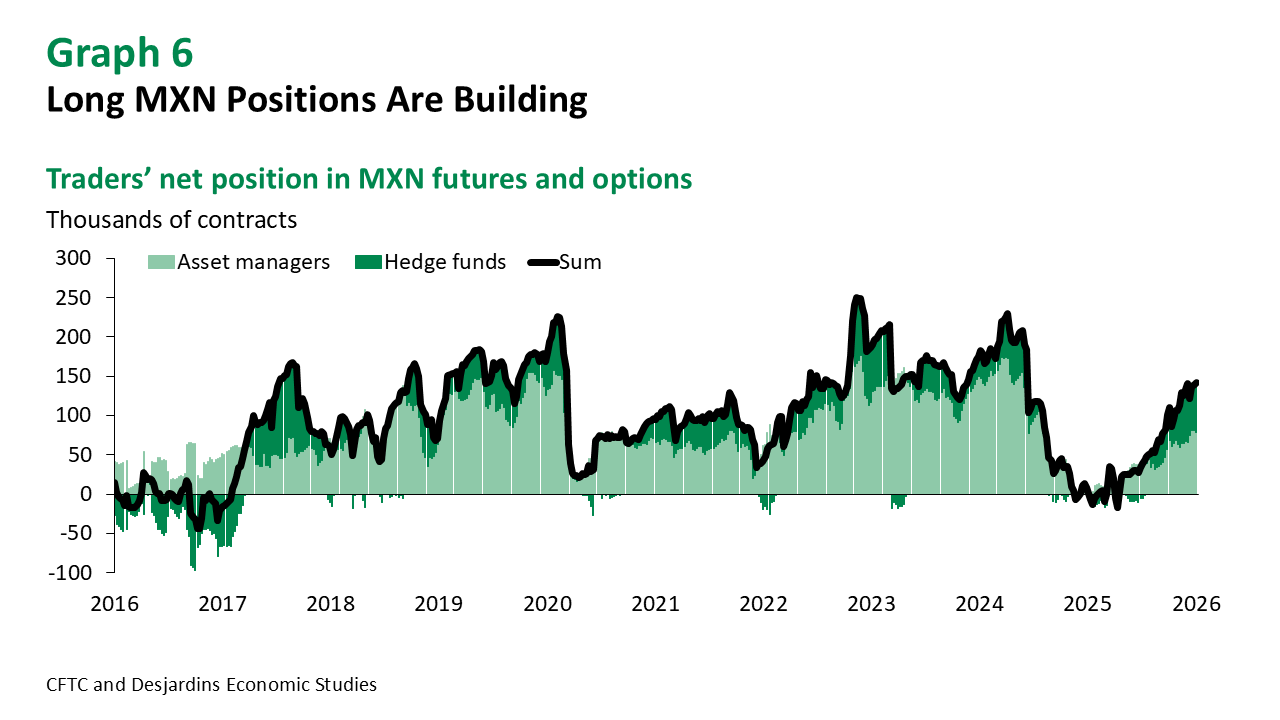

MXN

Mind the Carry Bets

USDMXN fell below 18.00 last month as carry traders piled into the currency amid low FX volatility. To be fair, MXN's profile remains attractive relative to EM peers on a volatility-adjusted basis. Banxico’s credibility is well established, real rates are high and the current account is balanced. Thus, macro risks are contained.

However, we are growing concerned about a correction due to the buildup of long MXN carry trade positions by speculative investors. This is evident in the CFTC data on futures and options, as well as record-breaking inflows of ~USD20 billion into government bonds last year (Q1–Q3 available data). This calls for some caution on the peso, which now appears vulnerable to a positioning squeeze if global risk appetite were to deteriorate.

We maintain our forecast for MXN to appreciate gradually to 17.80 by the end of 2026, but we flag the rising probability of a risk-off correction given the buildup of carry trade positions.

Forecast Table