- Jimmy Jean, Vice-President, Chief Economist and Strategist

Mirza Shaheryar Baig, Foreign Exchange Strategist

FX Analysis

Finding Rock Bottom

December 12, 2025

Highlights

- Job numbers have been encouraging, but the Canadian economy is not out of the woods yet.

- Data quirks in the Labour Force Survey and trade negotiations with the Trump administration could make the coming months bumpy.

- We still forecast the CAD to strengthen to 1.35 by year-end 2026, but there may be some volatility on trade headlines in Q1.

- The Fed will be cutting rates next year while most other central banks hold steady or hike. Fed independence will be under the spotlight, but a major policy misstep is not in our baseline.

- The US dollar should be softer next year, but we expect gains will be skewed towards commodity currencies and the RMB. We expect limited upside in EUR or JPY next year.

Overview

The Canadian dollar underperformed most of its trade partners this year but is now finding its feet. We expect the loonie to rebound next year, supported by tighter rate differentials, rising commodity prices and government measures to spur business investment. But the path will not be smooth. Investors should be ready for noise around trade negotiations and domestic politics. Commodity and emerging market currencies should benefit from a weaker US dollar and higher commodity prices, but we expect the euro and the yen to be held back by domestic risks.

CAD

Good News at Last!

The Canadian dollar surged after Statistics Canada reported that the unemployment rate fell from 6.9% in October to 6.5% in November—a welcome development given that unemployment had been trending higher for the past three years.

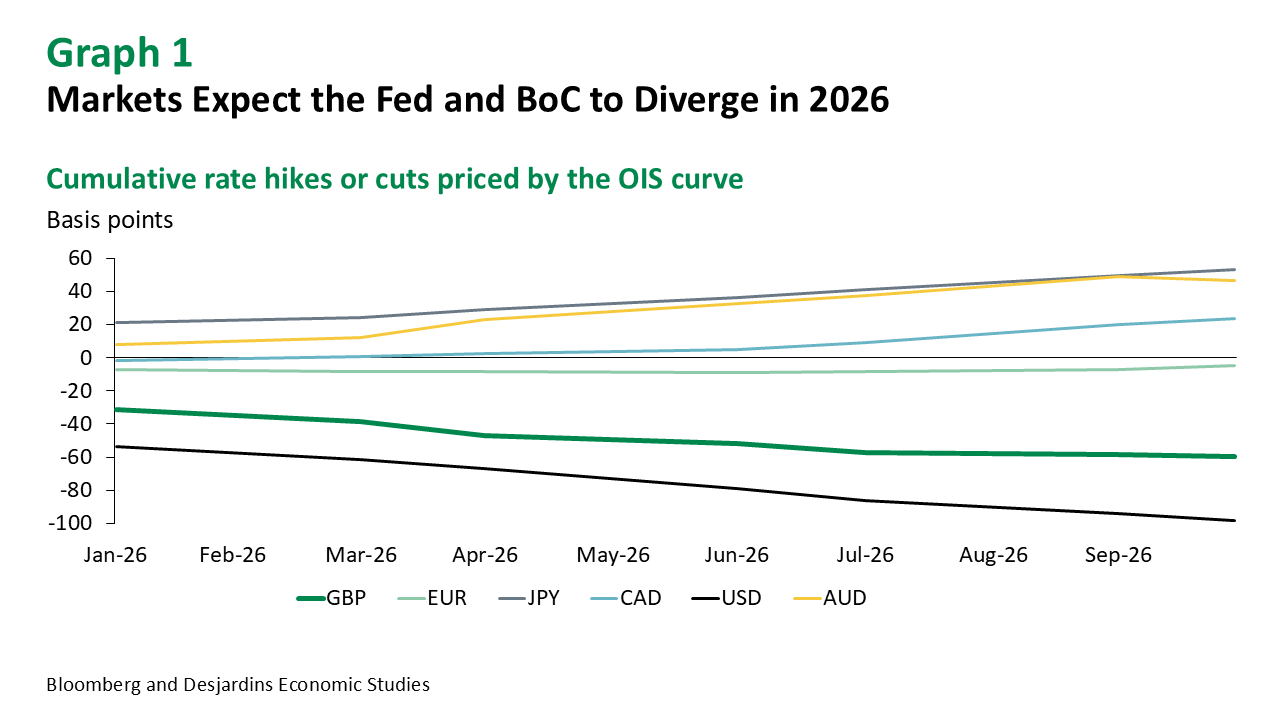

The OIS market now fully prices in a Bank of Canada rate hike within the next year, which would lift the overnight rate to 2.5%. In contrast, markets expect the Federal Reserve to lower its funds corridor to 3.00–3.25%. If these projections materialize, the policy rate gap would shrink from the current 150 basis points to just 50 basis points by the end of next year.

Separately, growing adoption of AI by private businesses and the government’s push to raise business investment could help boost productivity, which has lagged relative to the US over the last 25 years. Canada’s is well positioned to benefit from the AI infrastructure boom, particularly as it drives foreign demand for some of its commodities. These factors pose upside risks to our CAD forecasts but are not part of our baseline.

Still, the market may be running ahead of fundamentals. While the jobs report looks encouraging, most of the gains were in part-time positions, and roughly half the decline in the unemployment rate reflects a lower participation rate (fewer people looking for jobs). Adding to the uncertainty, the upcoming CUSMA review could generate disruptive headlines in Q1—such as a President Trump threatening to walk away from the agreement—echoing the theatrics seen earlier this year.

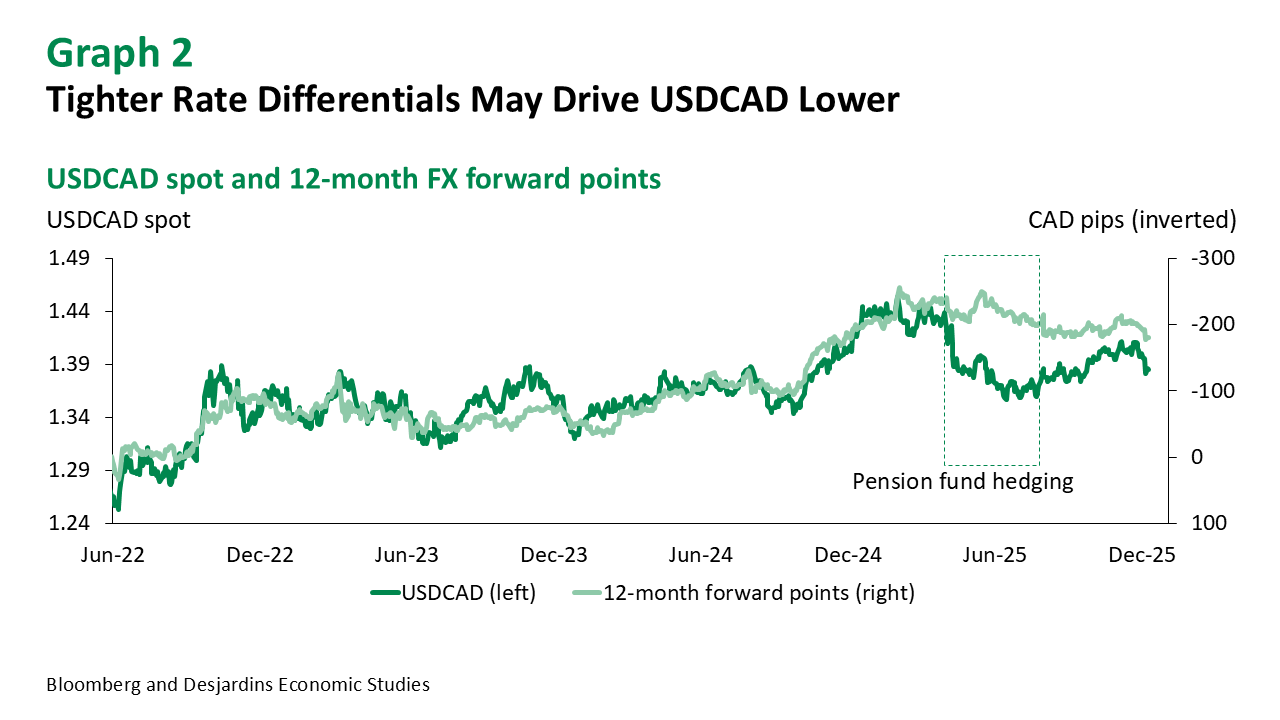

We expect the loonie to extend gains against most currencies next year, but the path won’t be smooth. Investors should be ready for noise around trade negotiations and domestic political developments (such as the Quebec 2026 election, which could have important consequences). While the broader trend points to CAD appreciation, navigating these landmines will be key to capturing upside without getting caught in sharp reversals.

USD

Fed Independence Under the Spotlight

It’s no secret that the Trump administration favours low interest rates and a weaker dollar. Jerome Powell’s term as Fed Chair ends in May 2026, and the president has signalled he will announce a successor early next year. Markets expect that to be Kevin Hassett, currently his top economic adviser.

But political influence over monetary policy is only part of the story. Whoever takes the helm will inherit a very different world.

The US economy is navigating multiple structural shocks—higher tariffs, tighter immigration, deregulation and the rise of AI. Hassett has argued that these shifts justify a more flexible approach to inflation targeting. This is not an unreasonable claim. In fact, market-implied inflation expectations have held steady this year, though they’re still above the Fed’s 2% goal.

What does this mean for the dollar? Two key channels:

- Narrower rate differentials. The Fed is set to cut rates next year while most other central banks stay put. We expect a terminal rate near 3%, with cuts likely in H2. While this aligns with consensus, we think institutional investors—especially pension funds—will raise FX hedge ratios on US assets, given sensitivity to front-end swap points.

- Falling real rates. The “de-dollarization” narrative could gain traction if the Fed stays dovish despite upside inflation surprises. For now, the greenback still earns positive real rates, but a meaningful drop driven by a soft-on-inflation Fed would be a major headwind.

We forecast a 2% decline in the trade-weighted dollar next year, factoring in the first channel but not the second, which we currently see as a risk rather than a baseline.

EUR

Inner Weakness

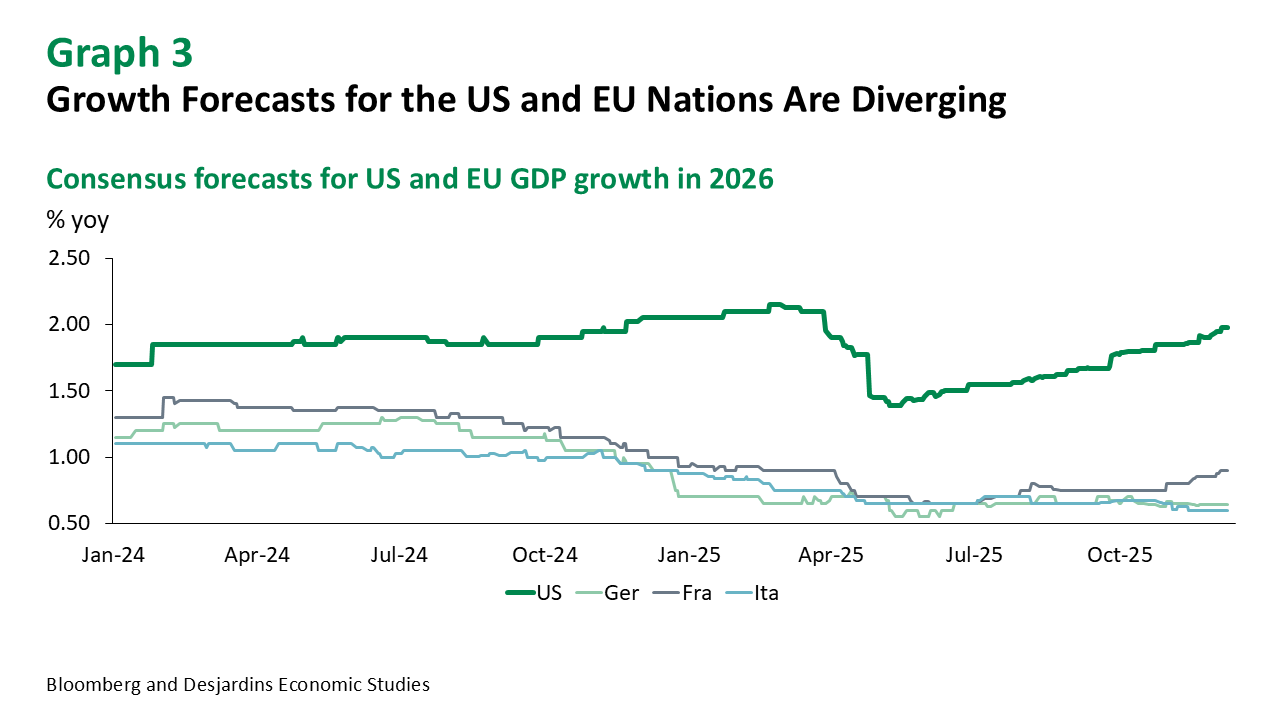

Most economists have scaled back expectations for a self-sustaining euro area recovery fuelled by Germany’s fiscal push. While Berlin’s policy shift is notable, three persistent headwinds continue to weigh on the outlook: the highest energy costs among OECD economies, intensifying competition from China and an overvalued euro.

The ECB has declared victory in bringing inflation to 2% and has signalled that policy is on hold. We expect rates to remain unchanged through 2026, though markets may begin pricing in some risk premium for a potential tightening cycle in 2027.

Meanwhile, Europe’s internal fault lines are deepening. While no major countries face elections next year, 2027 will see contests in France, Italy and Spain. To boot, Germany’s coalition looks fragile: recent polls show CDU/CSU support slipping to 24–25%, now trailing the far-right AfD, which leads national polls for the first time.

The euro outperformed most currencies in 2025, but we expect it to trade largely sideways next year—strengthening on bouts of USD weakness, then retreating as fiscal and political risks resurface. Overall, we anticipate a broad range between 1.15 and 1.20.

JPY

Go for Broke

Prime Minister Takaichi delivered on her populist agenda with a ¥21.3 trillion (around 3% of GDP) stimulus package featuring cash handouts, household subsidies and the removal of the gasoline tax.

This push means Japan’s fiscal deficit will widen from an already hefty 3.8% of GDP, though the government insists stronger tax revenues and nominal growth will keep the shortfall near current levels.

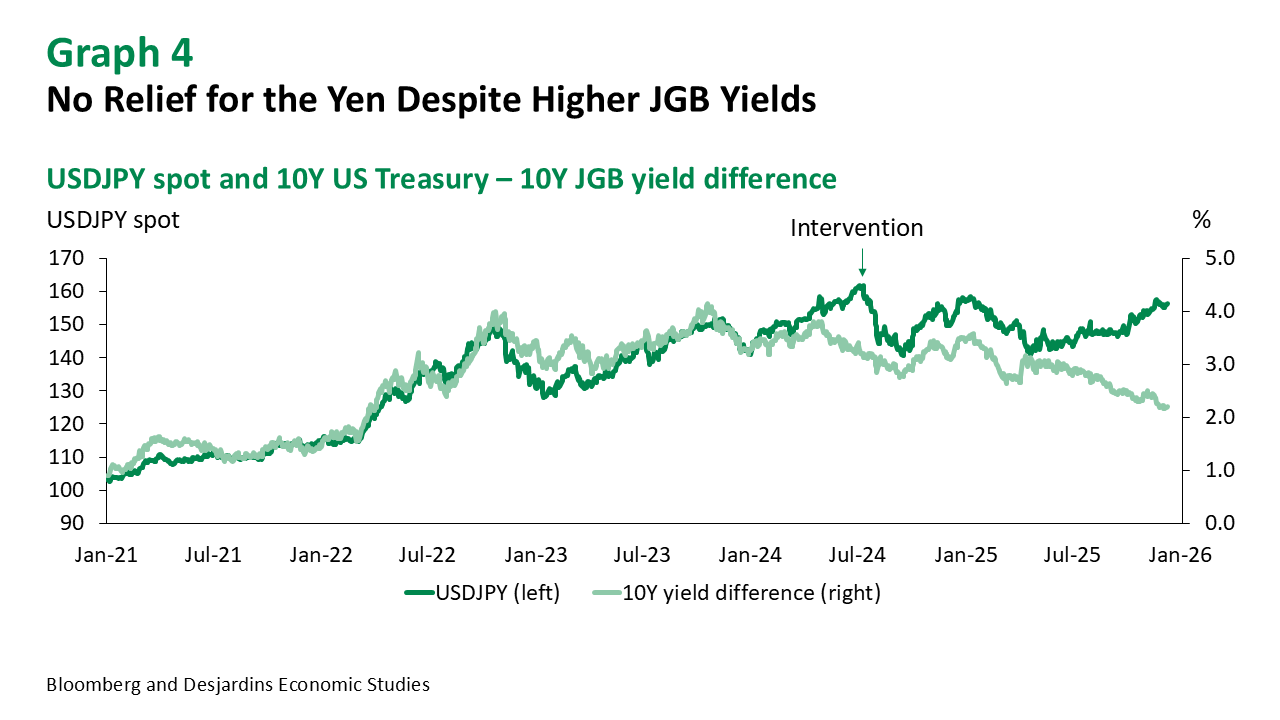

Markets remain unconvinced. JGB yields have climbed, with the 10‑year now approaching 2%. Higher yields have done little to support the yen. The traditional link between 10‑year yield differentials and USDJPY has broken down as bond markets react to aggressive fiscal spending.

How long can this last? A weak yen has become the pressure valve for ultra-loose fiscal and monetary policy. Verbal intervention from the Ministry of Finance and a likely BoJ hike in December may buy time—but time for what?

We believe the Takaichi administration intends to ride the stimulus wave and call early elections in the spring of 2026 to restore the LDP’s parliamentary majority. Once that goal is achieved, we expect a pivot toward fiscal discipline and normalization of real rates. This underpins our forecast of USDJPY at 150 by end‑2026. But the risks are skewed higher for USDJPY.

CNY

Surplus Surge

US–China trade tensions have eased following the landmark meeting between Presidents Trump and Xi in Busan in late October. President Trump is scheduled to visit Beijing in April 2026, with a reciprocal state visit from Xi planned afterward.

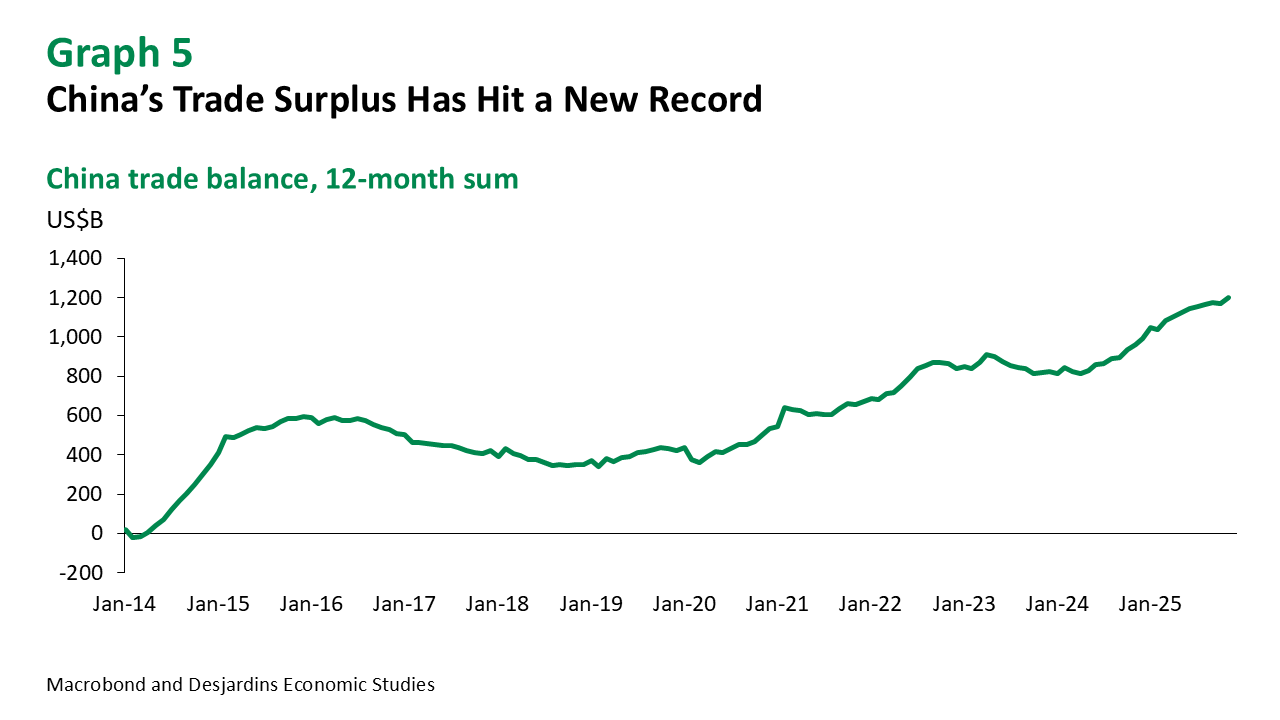

Meanwhile, Chinese exporters continue to gain ground. We estimate that China’s share of global exports rose to around 20% in November, near its post-Covid peak of 20.4%. On a rolling 12‑month basis, China’s trade surplus hit a record US$1.18 trillion in November.

To be sure, there are several explanations for China’s rising trade surplus, including weak domestic demand, growing dominance in electric vehicles and deeper ties with the Global South. But an undervalued exchange rate is a factor as well. On a simple CPI-based purchasing power parity basis, we estimate that the RMB is now more undervalued than it was 20 years ago, when it was pegged to the US dollar at 8.28! For perspective, a foreign visitor to Shanghai can expect to pay about US$250 for a night’s stay in a 5-star hotel, less than half the cost in Toronto or Vancouver.

With trade tensions on pause, we expect the PBoC to allow a meaningful appreciation of the renminbi. We have penciled in a 5% rise against the USD next year, marking a notable shift from recent trading ranges.

MXN

Carry On

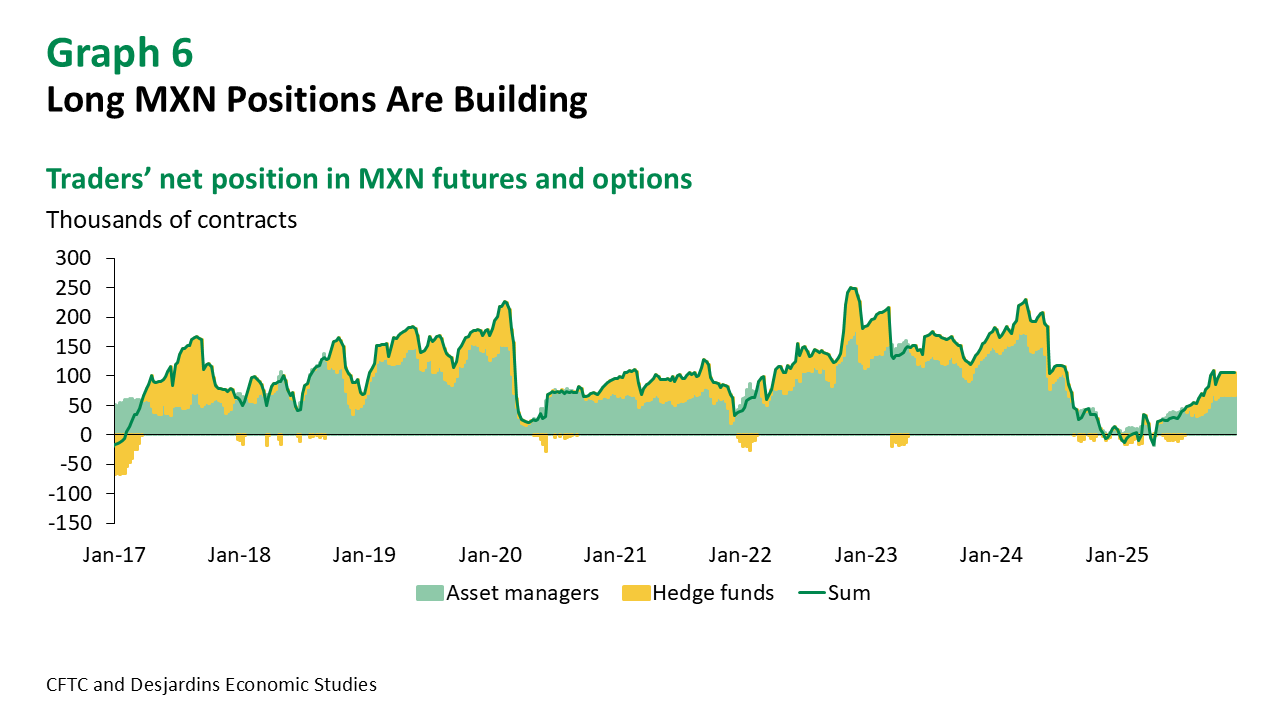

Banxico’s rate cuts have reduced the policy rate spread between Mexico and the US from 600bps at the start of the easing cycle to 350bps. The central bank is now signalling that it is at the end of its easing cycle. We expect one final cut in December followed by a long pause. As such, carry should stabilize around current levels or improve gradually on Fed rate cuts.

Despite the notable decline in interest rates, MXN’s profile remains attractive relative to EM peers on a volatility-adjusted basis. Moreover, real interest rates remain around 5%, which are high for an economy that is now running a balanced current account. While offshore traders have increased their bets on MXN recently, the size of positions is still below historically extreme levels.

Given Mexico’s strong reliance on trade flows and foreign investment, the CUSMA review is critical for currency stability. Mexico has geared up for a tough review process, addressing US concerns about its energy, agriculture, IP and customs policies. We would brace for headline risks in Q1, but once there is clarity on the issue, there could be more support for the peso. We expect USDMXN to end next year around 17.80.

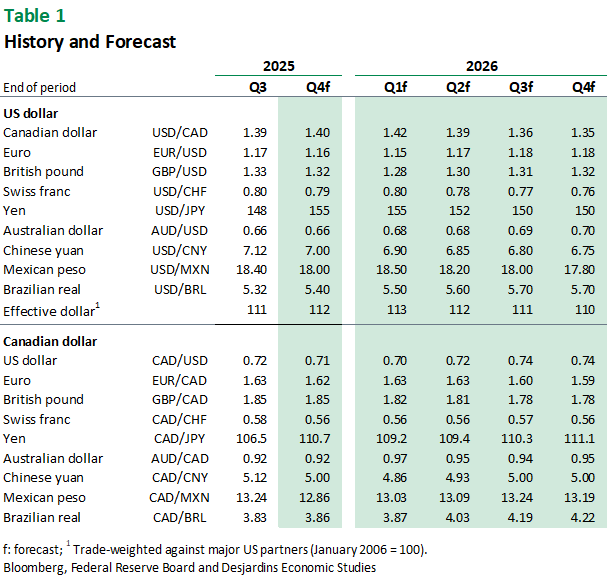

Forecast Table