- LJ Valencia

Economist

Economic News

Canada: Trade Deficit Widens As Gold Reverses Course

October 7, 2025

Highlights

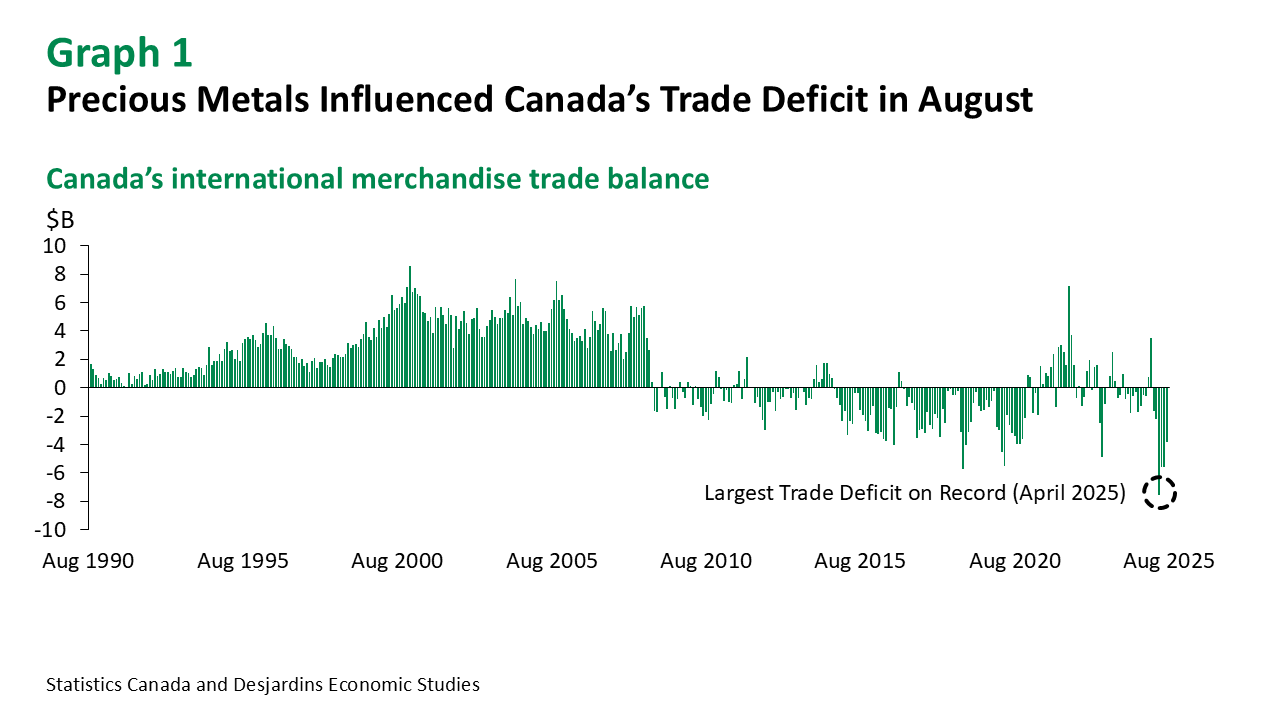

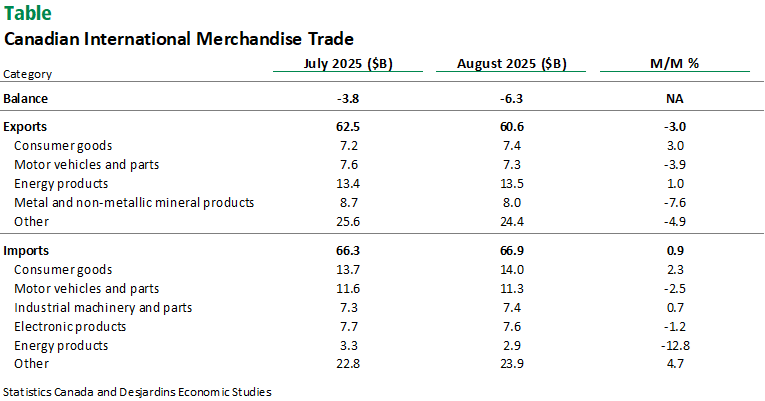

- Canada’s international merchandise trade deficit widened to $6.3B in August from a revised $3.8B in the prior month (graph 1). This was deeper into negative territory than the consensus expectation for a $5.6B deficit. See table for more details.

- Goods exports were down 3.0% m/m in August—a reversal from gains in the prior three months. Imports rose by 0.9%. In real terms, exports fell by 3.2% while imports increased by 0.2%.

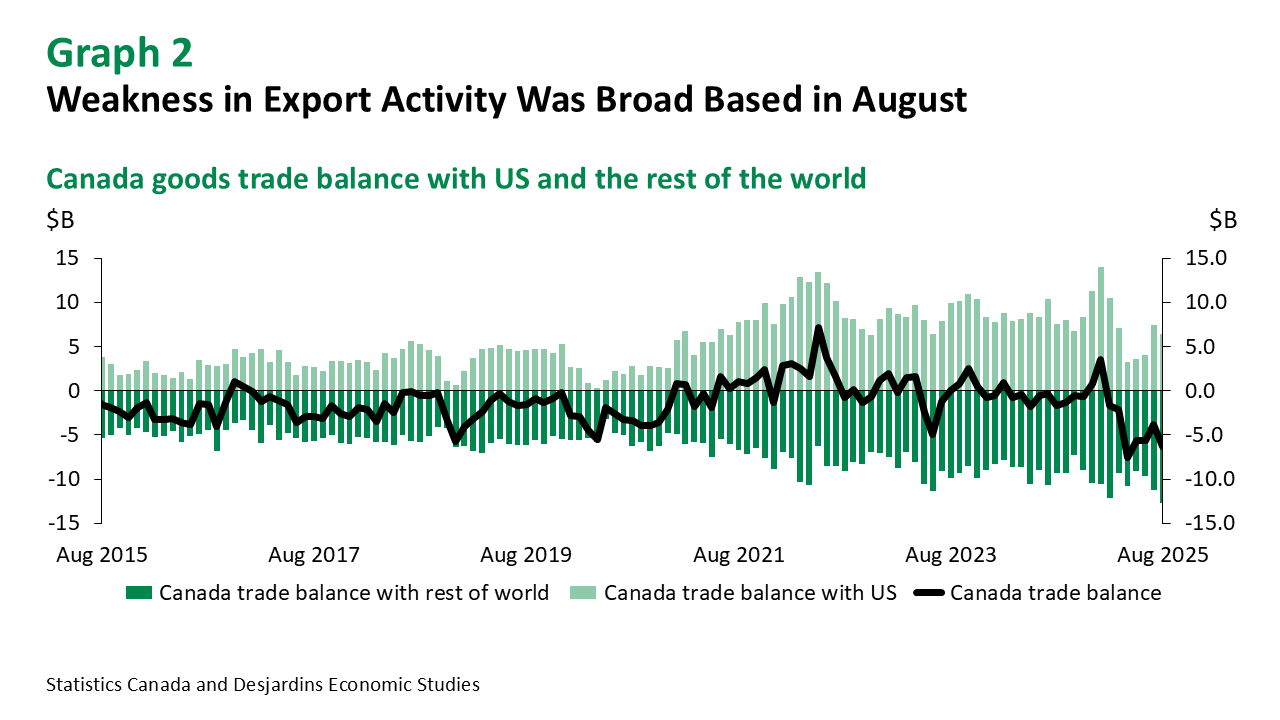

- Canada’s trade surplus with the US shrunk from $7.4B to $6.4B in August (graph 2). Meanwhile, the trade deficit with countries other than the United States widened from $11.2B to $12.8B in the month.

- Services trade in August posted a $340M surplus. Exports of services declined by 0.2% while services imports were unchanged.

Comments

Canada’s exports saw a setback in August, with eight out of 11 export categories experiencing a decrease in the month. Exports of metal and non‑metallic mineral products contributed most to the decline (-7.6% m/m), mainly on the back of lower gold exports to the US. Industrial machinery, equipment, and parts fell for the first time in four months (-9.5%), largely driven by lower exports of general‑purpose machinery and equipment to the US. Forestry products and building and packaging materials fell sharply (-10.1%), following US anti‑dumping and countervailing duties on Canadian softwood lumber. In contrast, energy products continue to be a bright spot for Canadian exports, posting a modest increase (1.0%).

On the flip side of the trade balance, metal and non‑metallic product imports saw a sharp rise of 24.2% in August, largely thanks to higher gold imports. Consumer products also saw gains (2.3%), partly due to higher prices and pharmaceutical shipments from Switzerland and Belgium. In contrast to these gains, six of 11 product categories posted declines. Energy product imports fell the most (12.8%), mainly due to lower crude oil imports from the US. Note that past import data may be revised significantly due to the CBSA Assessment and Revenue Management (CARM) initiative.

Implications

Today’s trade deficit is not welcome news. However, reflecting the recent trade data, net exports are still expected to contribute roughly +1.3 percentage points to Q3 output growth. We expect real GDP growth to be around 0.5% annualized in the quarter. This is just shy of the Bank of Canada's July Monetary Policy Report forecast of 1% annualized.

Looking ahead, trade disruptions and uncertainty will continue to impact Canadian economic activity and influence the decisions of central bankers. As such, our recent outlook External link. points to slow economic growth and weaker inflation in the coming quarters even if the economy manages to dodge a recession.