- LJ Valencia

Economic Analyst

Economic News

Canada: The Trade Surplus in December Provides Some Calm Before the Storm

February 5, 2025

Highlights

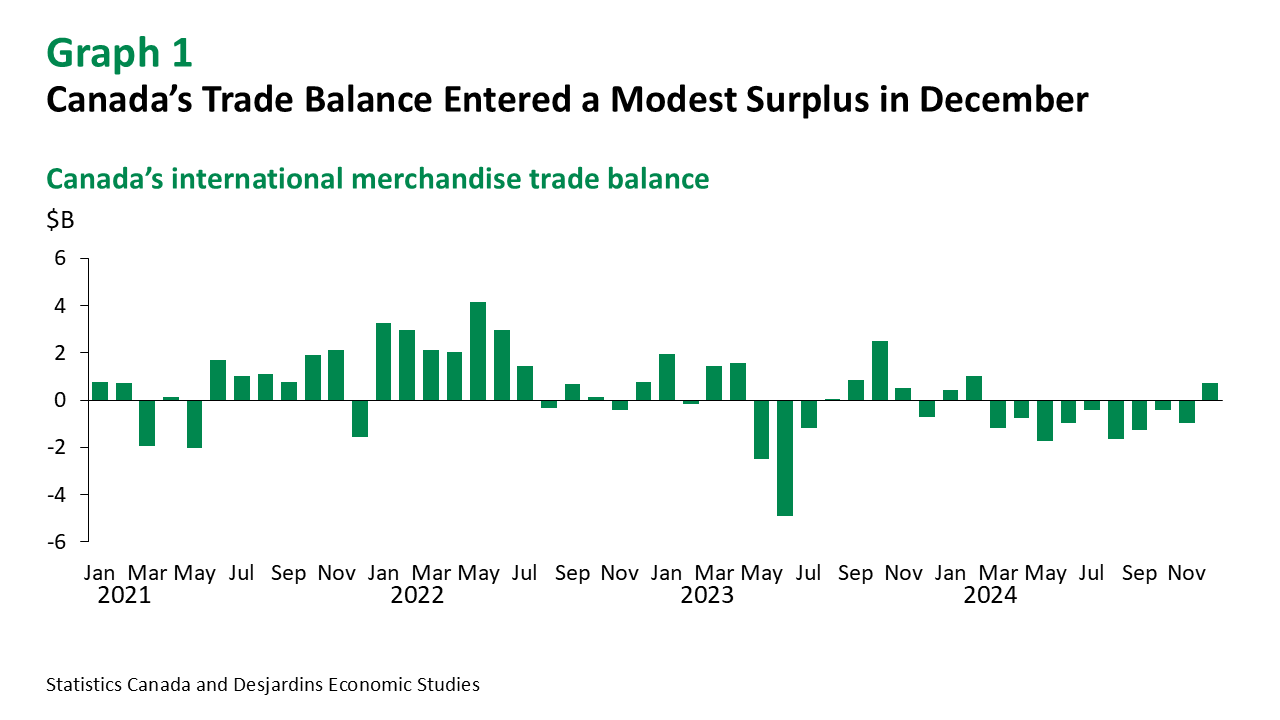

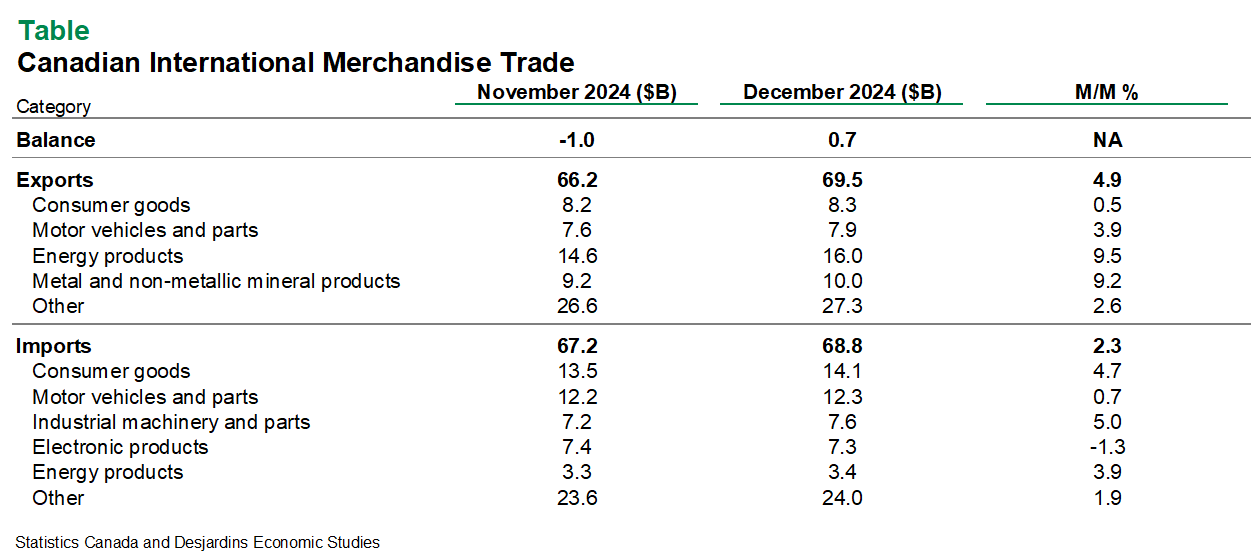

- Canada’s international merchandise trade balance went from a deficit of $986M in November to a surplus of $708M in December—the first surplus since February 2024 (graph 1). This was below the consensus expectation of $1B. See Table for more details.

- Goods exports were up for a third consecutive month, increasing by 4.9% m/m, while imports rose by 2.3%. In real terms, exports were up by 2.4% while imports grew by a more modest 0.6%.

- On a quarterly basis, nominal exports and imports rose by an annualized 18.2% q/q and 11.9%, respectively. The increase in exports was the largest quarterly increase since Q2 2022. After adjusting for prices, real exports and real imports rose by 11.3% and 8.5%, respectively.

- Canada’s trade deficit with countries other than the United States expanded from $9.2B to $10.6B. Meanwhile, the trade surplus with the US edged up from $8.2B to $11.3B, in part due to higher exports of energy products.

- The services trade balance entered a surplus of $641M in December, a reversal from a deficit of $1.4B in November. But on a quarterly basis, a decline in exports (-5.4% q/q ann.) and a small gain in imports (0.5% q/q ann.), caused the services trade balance to remain a deficit for Q4.

Comments

The depreciation of the Canadian dollar continued to boost nominal exports and imports for a third month in a row in December. Note that since most transactions are converted from USD to CAD, a weaker Canadian dollar leads to higher export volumes and import prices.

On the export side, eight out of the 11 categories experienced an increase in December. As expected, exports of energy products (9.5% m/m) and precious metals (9.2%) continued to be supported by higher prices. Demand for precious metals should continue to rise in the coming months, reflecting the anticipated decline of policy rates worldwide and increasing gold prices. Additional solid advances in exports were observed in categories like motor vehicles and parts (3.9%) and consumer goods (0.5%).

On the import side, Statistics Canada mentioned again that delays in data compilation due to the CBSA Assessment and Revenue Management (CARM) digital initiative may lead to significant revisions to import values from October to December. As such, import data should be taken with a grain of salt. That said, similar to November External link., the largest contributor to the December increase was the rise in imports of consumer goods (4.7%). Considering the federal tax break External link. on some products starting in December 2024, consumer goods imports could rise higher in January and February due to stronger demand.

Implications

The $708M trade surplus in December points to annualized real GDP growth in Q4 2024 of 2.0%, slightly above the Bank of Canada’s 1.8% from the January 2025 Monetary Policy Report. Net exports are expected to contribute a modest +0.3 percentage points to growth in our Q4 tracking, leaving strong domestic demand largely met by a draw down in inventories.

But today’s trade release is the calm before the gathering storm of potential US import tariffs in 2025 (see our recent analysis External link. on the implications for Canada). Looking ahead, we expect External link. the lingering threat of US tariffs to increase volatility in both exports and imports, likely weighing heavily on growth and the minds of Canadian central bankers.