- Florence Jean-Jacobs

Principal Economist

Economic News

Canadians’ Spending Cooled Off in September

November 21, 2025

Highlights

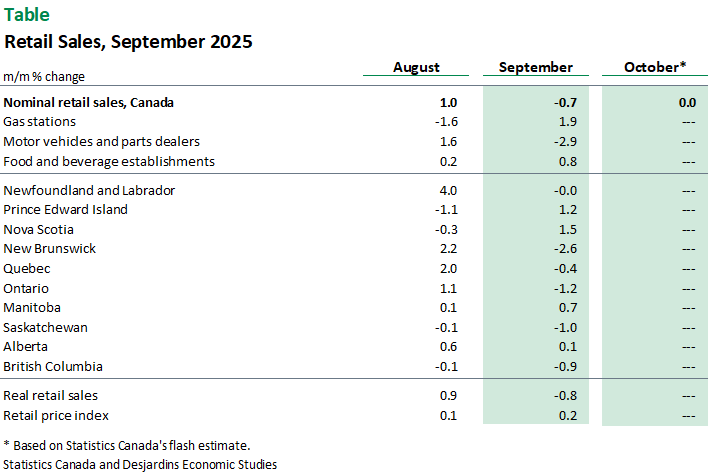

- Canadian retail sales fell by 0.7% m/m in September, in line with Statistics Canada’s flash estimate and the consensus of economic forecasters. (See table for details).

- The largest contributor to the decline was motor vehicle and parts dealerships, which registered a 2.9% drop in September—the first dip in three months.

- Nominal sales at gasoline stations increased by 1.9%, driven entirely by higher prices, as volumes declined.

- Core retail sales, which exclude autos and gasoline, were unchanged in September, with growth at food and beverage retailers being offset by lower sales at building material and garden equipment supplies dealers and general merchandise retailers.

- E-commerce sales were down 3.5% from August, and their 2.4% year-on-year decline in September is their sharpest drop since 2022.

- Retail sales dropped in six out of 10 provinces, with the largest decline in dollar terms registered in Ontario.

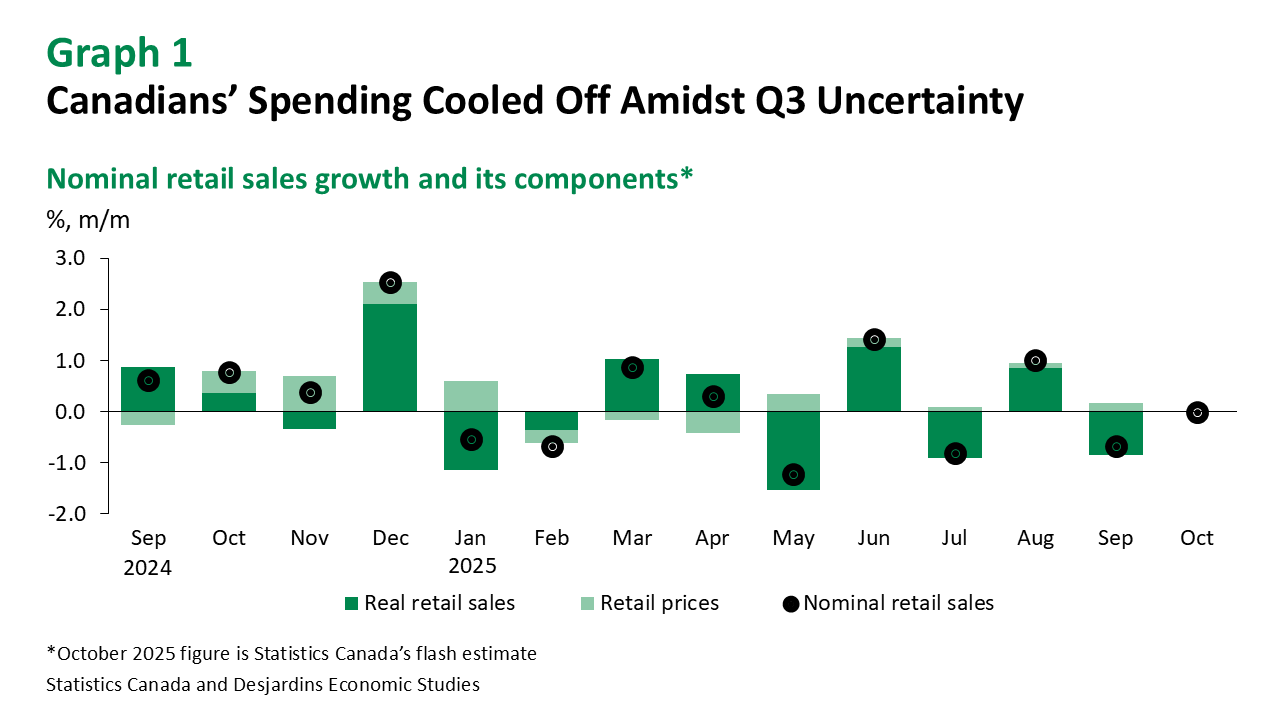

- In volume terms, retail sales decreased 0.8% in September, putting Q3 growth in negative territory (-1.2% q/q annualized).

- Softness appears to have persisted into October, with Statistics Canada’s advance indicator pointing to a flat print for retail sales to start the fourth quarter. But with seasonally adjusted goods prices down 0.2% in October, sales volumes probably inched up.

Implications

Perhaps unsurprisingly, real retail sales were down in Q3, amidst the uncertainty and trade tensions that continued to prevail in July through September. And as they entered the last quarter of the year, Canadian consumers appeared more cautious with their spending, both in store and online. The Bank of Canada’s recent monetary easing should give consumers and borrowers a helping hand, but we don’t expect further relief on that front in the near future.

While the cooldown in household spending is visible, inflation-adjusted retail sales have generally kept pace with population growth (graph 2), despite weak consumer sentiment. Looking to the months ahead, we expect slowing population growth to moderate overall retail sales.

After today’s release, our Q3 GDP tracking remains roughly in line with the Bank of Canada’s forecast of 0.5%. If labour market conditions continue to improve, as was the case in September and October, we anticipate retail sales should continue holding steady. That said, the outlook remains subject to downside risks linked to the uncertain outcome of trade negotiations with the US.