- Randall Bartlett

Senior Director of Canadian Economics

Economic News

Canada: Real GDP Starts 2024 with a Bang

March 28, 2024

Highlights

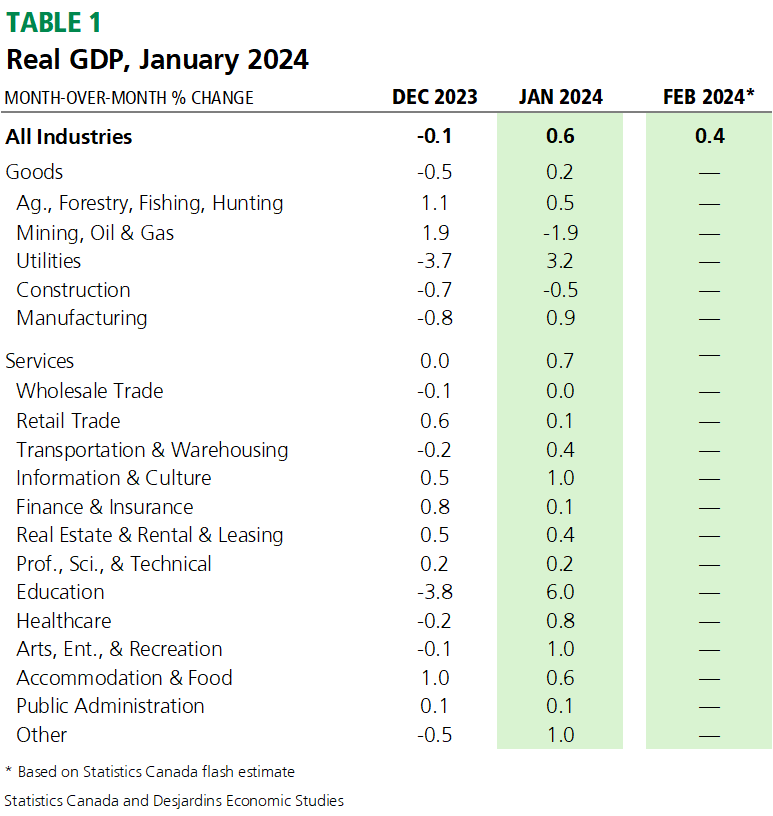

- Real GDP moved sharply higher in January, increasing by 0.6% in the month, for the strongest advance since January 2023. This beat both the consensus of economic forecasters and Statistics Canada’s flash estimate (0.4%). Services-producing sectors drove the gain, rising by 0.7% thanks to a rebound in educational services following the resolution of public service strikes in Quebec. Meanwhile, good-producing industries advanced by a still-respectable 0.2%. In all, 18 of 20 subsectors posted gains. See Table 1 for further details.

Implications

There was a lot to like in the January 2024 real GDP release beyond just the headline outperformance. While the rebound in education services (up 6%) was widely expected, the gains were much more broad-based than that. Indeed, every service-producing sector moved higher in the month. That includes industries like accommodation and food services, arts and entertainment, and retails sales, all of which reflect discretionary spending by households that are increasingly strained under the weight of high borrowing costs.

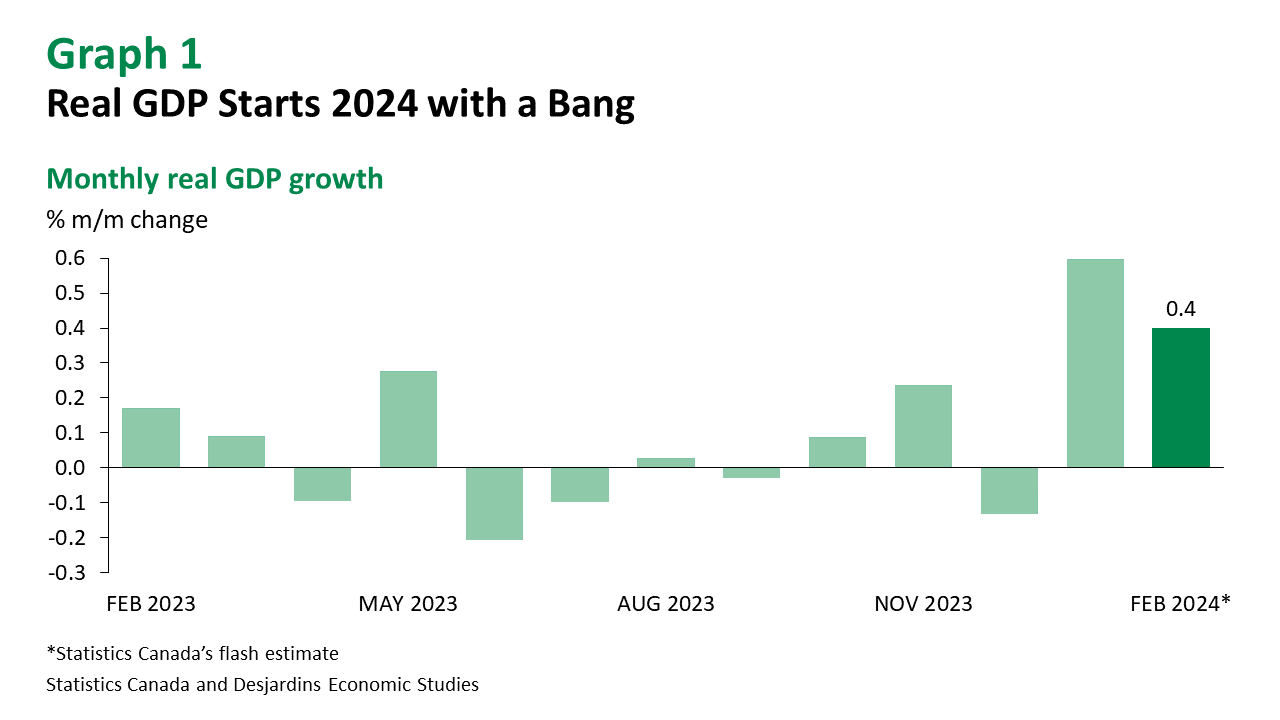

Looking ahead, Statistics Canada’s flash estimate for December is pointing to 0.4% growth in real GDP by industry (graph 1). Assuming it is correct and that there is no growth in March, real GDP by industry would advance by 3.5% annualized in Q1 2024. While our tracking is a little more cautious, we’re projecting an advance in real GDP by expenditure of at least 2% in Q1. This is way beyond the 0.5% forecast in the Bank of Canada’s January 2024 Monetary Policy Report.

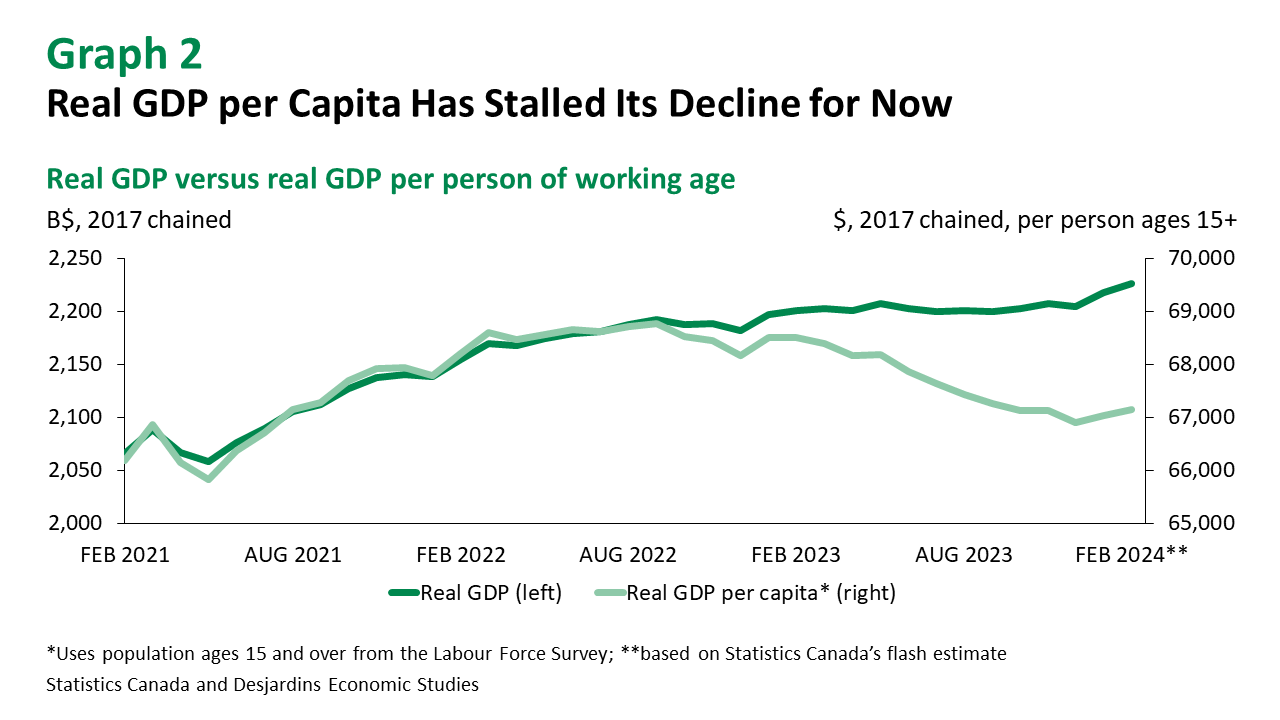

For the Bank of Canada, we think it will broadly look through the January real GDP print, in large part due to the outsized role played by education. At the same time, while real GDP per capita looks as though it may have stalled its decline, it remains well below levels reached in mid-2022 (graph 2). But maybe most importantly, inflation came in below expectations in both January and February External link. despite this outsized real GDP growth, and is tracking a slower pace than the Bank expected for Q1 (2.8% y/y versus 3.2%). In that context, the recent announcement of federal government plans to reduce non-permanent resident admissions should weaken this material tailwind to both growth and inflation going forward External link.. As such, we are of the view that the Bank remains on track to begin cutting interest rates at its upcoming June meeting.