- LJ Valencia

Economist

Economic News

Canada: Weak November Real GDP Tees Up a Possible Q4 Contraction

January 30, 2026

Highlights

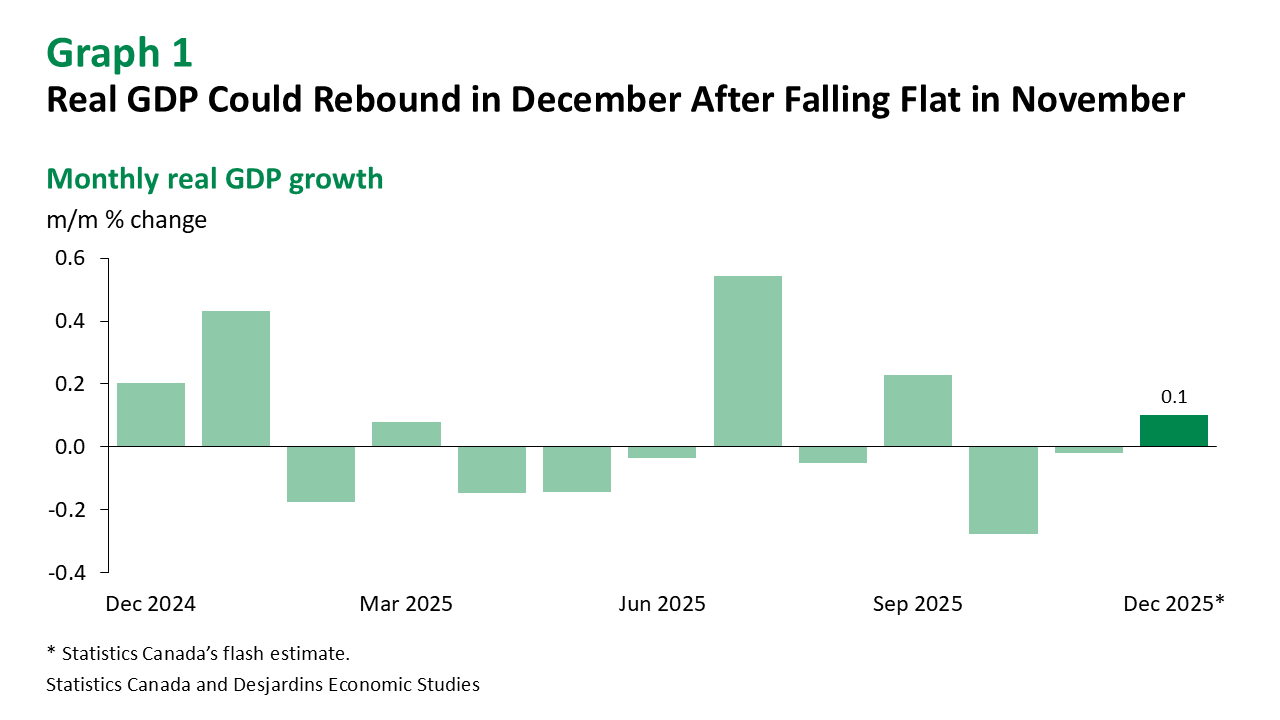

- Canadian real GDP was unchanged in November, following a decrease in the prior month. This was below the consensus of economic forecasters and Statistics Canada’s flash estimate (0.1% m/m). Gains in services-producing industries were offset by losses in goods-producing industries. See Table 1 for further details.

- Statistics Canada’s flash estimate points to a 0.1% increase in real GDP in December (graph 1), thanks to gains in manufacturing and wholesale trade offsetting weakness in resource extraction. That suggests a possible decline in real GDP by industry of 0.5% annualized in Q4 2025.

Comments

The muted real GDP growth print in November was primarily driven by weakness in goods-producing industries (-0.3% m/m). The manufacturing sector contracted (-1.3%), on the back of decreases in both durable and non-durable manufacturing. Durable goods output was weighed down by transportation equipment, machinery and fabricated metal products, pushing output in the subsector to its lowest level since mid‑2011 (excluding the pandemic period). Motor vehicle and parts manufacturing also fell as a global semiconductor shortage limited production. The agriculture, forestry, fishing and hunting sector decreased for a second straight month (-1.1%), likely due to US and China tariffs.

The services sector posted a modest 0.1% bump in November. Retail trade External link. rose (1.3%), with gains across all subsectors and more than offsetting the back-to-back monthly declines in the past two months. Educational services rebounded (1.0%), thanks largely to classes resuming in Alberta after the teachers’ strike ended in October. Transportation and warehousing also grew (0.9%), fully reversing the weakness recorded in the previous month. In contrast, wholesale trade saw its largest decline since April 2025 (-2.1%), on the back of lower activity in motor vehicle and parts, as well as building materials and supplies.

The lower-than-expected November print resulted in a decline in real GDP per capita, with no clear signs of improvement despite slower population growth External link. (graph 2).

Implications

Given the latest data, our tracking suggests real GDP by expenditure should grow at an annualized pace of about 0.25% in Q4, slightly above the Bank of Canada’s latest projection of a flat print. This stands in contrast to Statistics Canada’s estimate of a 0.5% contraction in real GDP by industry. The difference in our forecast with the official estimate can largely be explained by inventories, and is not out of line with recent differences in real GDP growth estimates (graph 3).

Our latest outlook External link. points to modest growth in 2026, but the path may be volatile. Effective tariff rates External link. remain low thanks higher compliance under the Canada–United States–Mexico Agreement (CUSMA), but uncertainty remains high and risks tilted to the downside as the CUSMA joint review approaches. With inflation External link. hovering around the Bank of Canada’s 2% target, the Bank held rates steady in its latest announcement External link. but indicated it stands ready to act if the outlook changes. All in all, today’s GDP data is unlikely to move the monetary policy needle.