- LJ Valencia

Economist

Economic News

Canada: Domestic Demand Showed Resilience in Q4 Despite Real GDP Contraction

February 27, 2026

Highlights

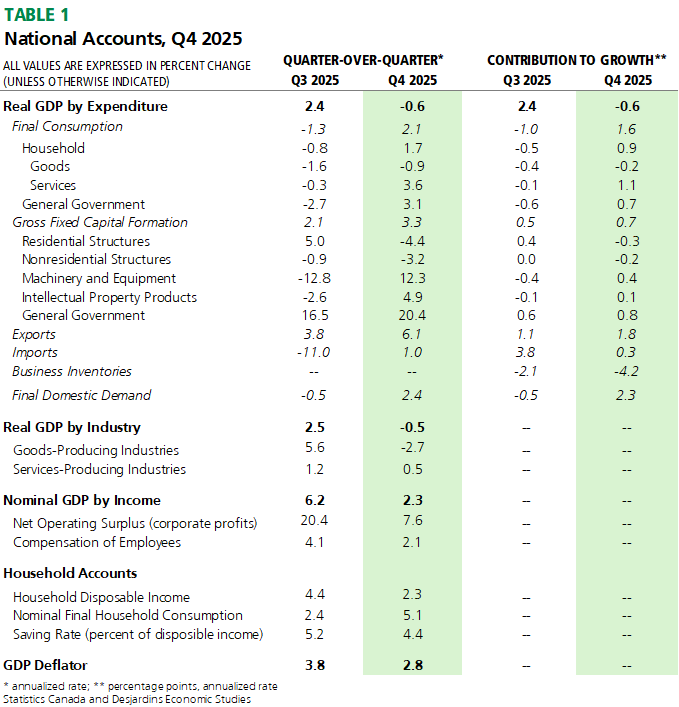

- Real GDP fell at an annualized pace of 0.6% q/q in Q4 2025. This was below the consensus of economic forecasters (-0.2%) and the Bank of Canada’s outlook of no change in real GDP. Table 1 provides more details on the release.

- At 1.7%, real GDP in 2025 grew to its slowest pace since the COVID‑19 pandemic, largely because of headwinds stemming from the trade war.

- Monthly real GDP rose in December (0.2% m/m), above consensus (0.1%). On a quarterly basis, real GDP by industry declined by 0.5% q/q annualized in Q4.

- Statistics Canada expects real GDP by industry to be broadly unchanged in January 2026, citing gains in oil and gas extraction and finance and insurance being partially offset by losses in manufacturing and real estate, rental and leasing.

Comments

The decline in real GDP during Q4 2025 was led by a significant drawdown of non-farm inventories, mainly in the manufacturing and wholesale sectors (graph 1).

Trade activity grew in the quarter, with exports advancing significantly (6.1%) on the back of higher gold and aluminum exports. That said, exports fell overall in 2025 (-1.7%) as shipments to the United States failed to recover after the new US tariffs came into full effect in Q1 2025. On the other hand, imports increased 1.0% in 2025, largely due to higher purchases of computers, clothing, footwear and metal ores.

Real investment accelerated in Q4 (3.3% q/q annualized) on the back of increased government capital spending (20.4%), as Canada continued to purchase weapons systems to meet its NATO targets. Moreover, the contribution from government investment to real GDP growth saw its strongest pace since Q3 2009 (0.8%). Investment in machinery and equipment also moved higher, as purchases of IT equipment and software showed the sort of increase seen throughout 2025 in the United States. In contrast, residential investment declined (-4.4%), as activity in the resale market, renovations and new construction fell.

Household spending rose in the quarter (1.7% q/q annualized) on the back of higher spending on rent and services. Overall, domestic demand bounced back with a healthy 2.4% gain. Domestic demand has been volatile, however. It was up just 1.4% year-over-year—a pace last seen in 2023 as the economy was contending with rate hikes. That said, slowing population growth also plays a role, and domestic demand is on a firmer footing on a per-capita basis. Indeed, per capita real GDP growth was flat in Q4 despite the decline in headline real GDP as Canada’s population shrunk (graph 2).

Compensation of employees slowed to 2.1% q/q annualized in Q4. The savings rate edged down to 4.4% on lower income and investment earnings. Lastly, corporate profits grew at a slower pace in Q4 (7.6%), largely because of gains in the mining sector being offset by weakness in the energy sector.

Implications

The economy showed resilience in Q4, despite the headline contraction. Our early tracking suggests that growth in real GDP by expenditure could be in the range of 1% to 1.5% annualized in Q1 2026. That’s below the Bank of Canada’s outlook for 1.8% growth published in its January 2026 Monetary Policy Report External link..

The path forward remains uncertain, however. As shown in our analysis External link., an unfavourable outcome from the CUSMA joint review could be a significant headwind for 2026. With our baseline assuming no major adverse disruption coming from the joint review, and with the resilient domestic demand evidenced in today’s report, we remain of the view that the Bank of Canada will be staying on the sidelines for a while.