- LJ Valencia

Economic Analyst

Economic News

Canada: Household Finances Started 2025 in Good Shape

June 12, 2025

Highlights

- Canadian households were more prosperous in Q1 2025 as net wealth increased by 0.8% q/q in the quarter (up $141.2B to $17.6T)—the sixth consecutive quarterly increase. This advance was due to gains in equities and real estate, more than offsetting increased borrowing.

- Household borrowing rose $34.5B in Q1, albeit at a slower pace than in recent quarters. Under the hood, the increase was driven primarily by mortgage loans ($30.7B) and to a much smaller extent by non-mortgage debt.

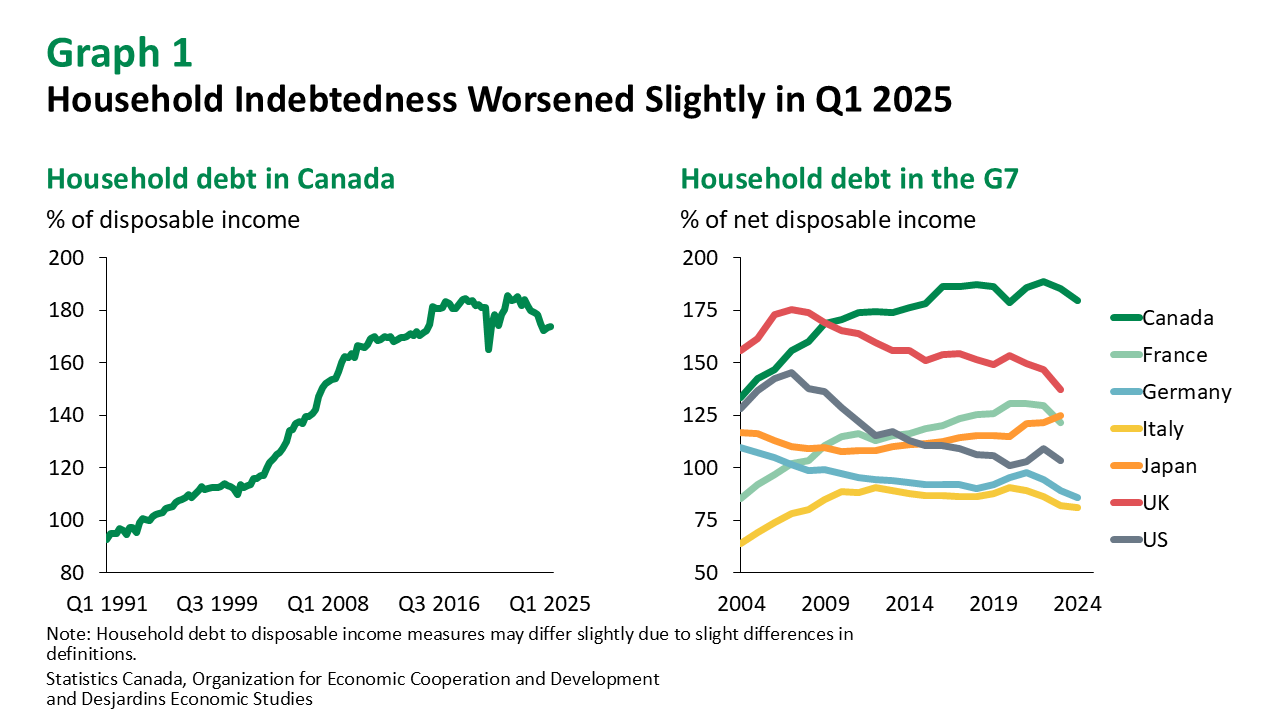

- Household credit market debt tallied $3.0T in Q1. As a proportion of household disposable income, it rose for a second straight quarter, reaching 173.9% from 173.5% in Q4 2024. Household indebtedness remained only slightly below the historic high of 185.7% reached in Q4 2021 (graph 1). Canadian households were the most indebted among G7 countries by a wide margin in 2024, and the Q1 2025 numbers don’t suggest that has changed.

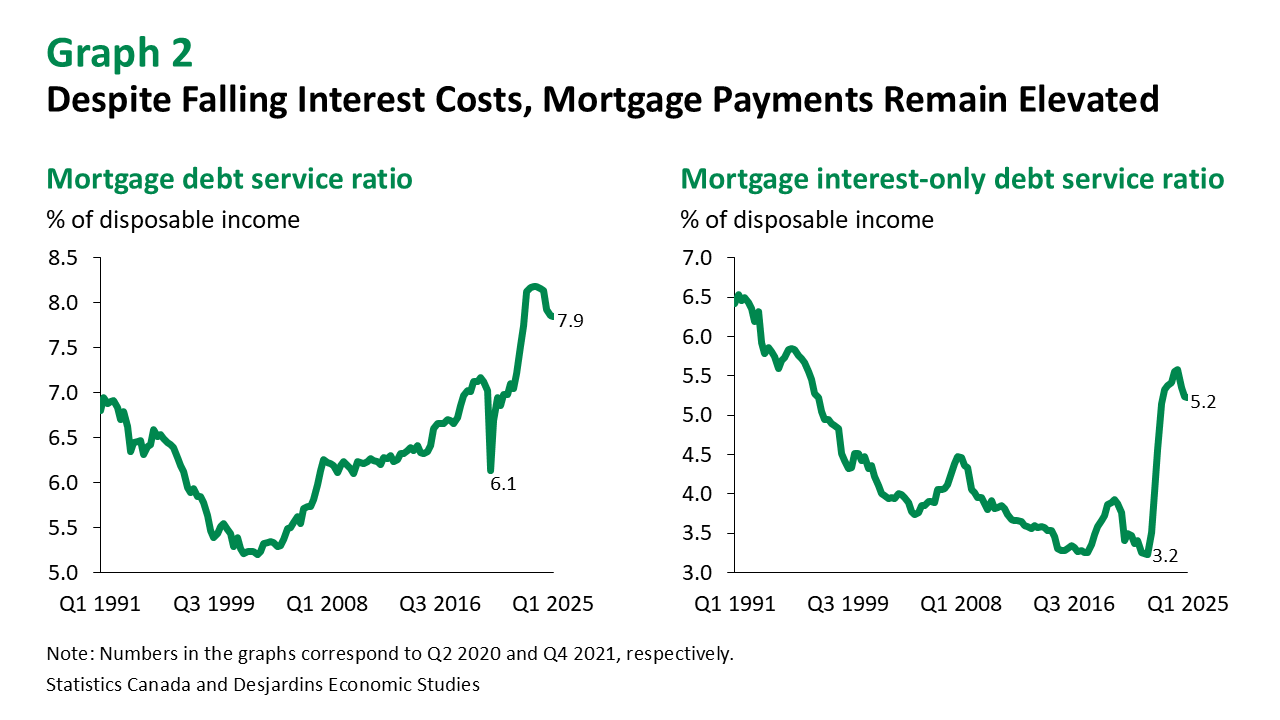

- The household debt service ratio—the share of disposable income directed toward debt payments—was unchanged at 14.4% in the first quarter. This isn’t far from the unprecedented peak of 15.1% reached in Q4 2023. Growth in disposable income helped to forestall a rise in the cost of debt servicing. The mortgage-only debt service ratio stood at 7.9% in the first quarter, slightly below the record high of 8.2% at the end of 2023 but still elevated (graph 2).

Implications

The Q1 2025 balance sheet data make clear that Canadian household finances started 2025 in good shape. However, the slower-than-usual pace of gains in net worth resulted in a slight fall in the savings rate in Q1 2025 External link.. This slowdown also coincided with higher consumer spending thanks, in part, to government supports such as the GST/HST holiday that ended in mid-February. Consumer spending remained solid with a boost to retail sales External link. in March, possibly reflecting the solid financial health of Canadians. It is likely also the result of a rush to get ahead of tariffs on imports from the United States and a renewed sense of patriotism driving a desire to buy local. The labour market is showing more resilience that we would have expected given the circumstances as well. All in all, Canadian household budgets were well-positioned for 2025.

While this is welcome news, the road ahead is less encouraging. The on-again, off-again tariff policies and trade uncertainty from our southern neighbour are a significant downside risk External link. to economic growth in 2025. The resulting slowdown could lead to employment losses while retaliatory tariffs are likely to add more fuel to the inflationary fire. The mortgage renewal wall is another concern as more households could face higher monthly mortgage payments. Looking ahead, the Bank of Canada will have a difficult balancing act as it weighs these conflicting forces.