- Kari Norman

Economist

Economic News

Canada: Once Again, Equity-Driven Wealth Gains Skewed Toward Affluent Households

December 11, 2025

Highlights

- Canadian households on average were more prosperous in Q3 2025 as net worth climbed by 2.6% q/q in the quarter (up $460.5B to $18.4T)—the eighth consecutive quarterly increase and the largest since Q1 2024. This advance was primarily due to gains in financial assets (+4.8% or $532.4B). This was slightly offset by an increase in household liabilities such as mortgage and non-mortgage debt (+1.3% or $40.8B) and a decline in residential real estate value (-0.6% or $53.4B).

- Household borrowing slowed to $33.5B in Q3. Under the hood, mortgage demand fell to $23.4B while non-mortgage debt—including consumer credit—edged up to $10.1B.

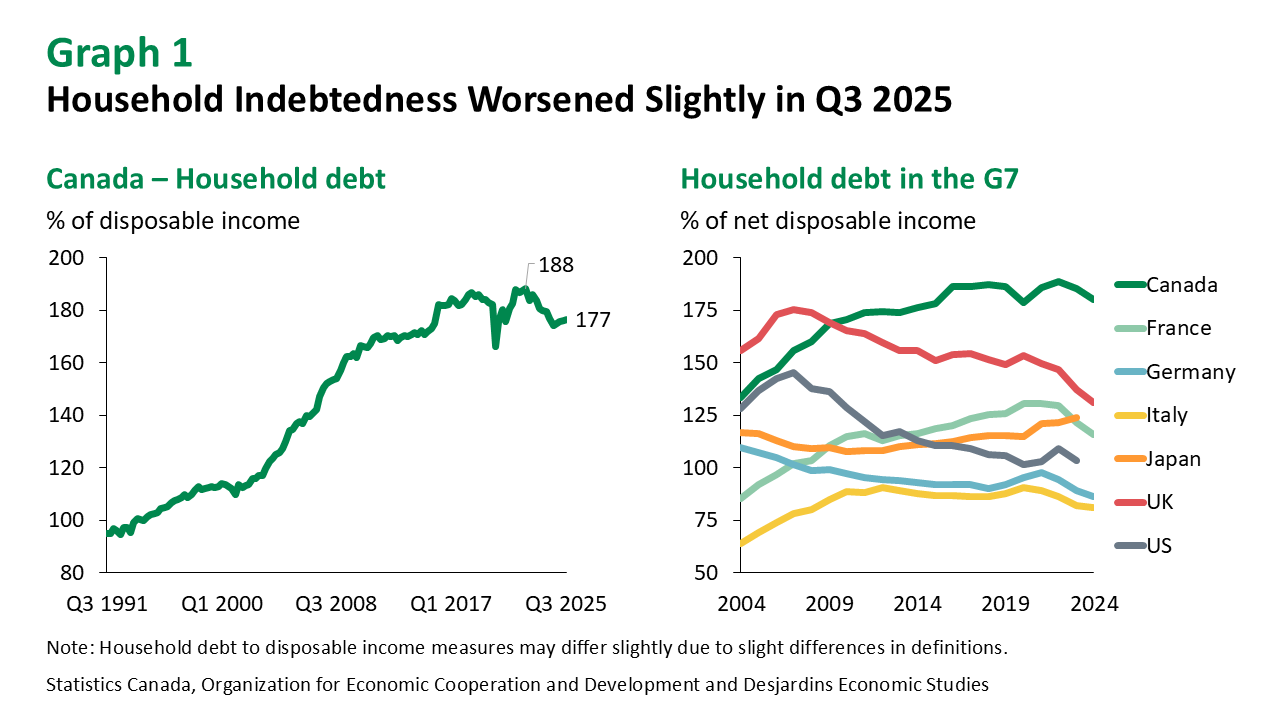

- Household credit market debt rose 1.0% to nearly $3.2T in Q3. As a proportion of household disposable income, it rose for a fourth straight quarter to 176.7%, but stayed below the historic high of 188.2% reached in Q3 2022 (graph 1). Canadian households remain the most indebted among G7 countries by a wide margin.

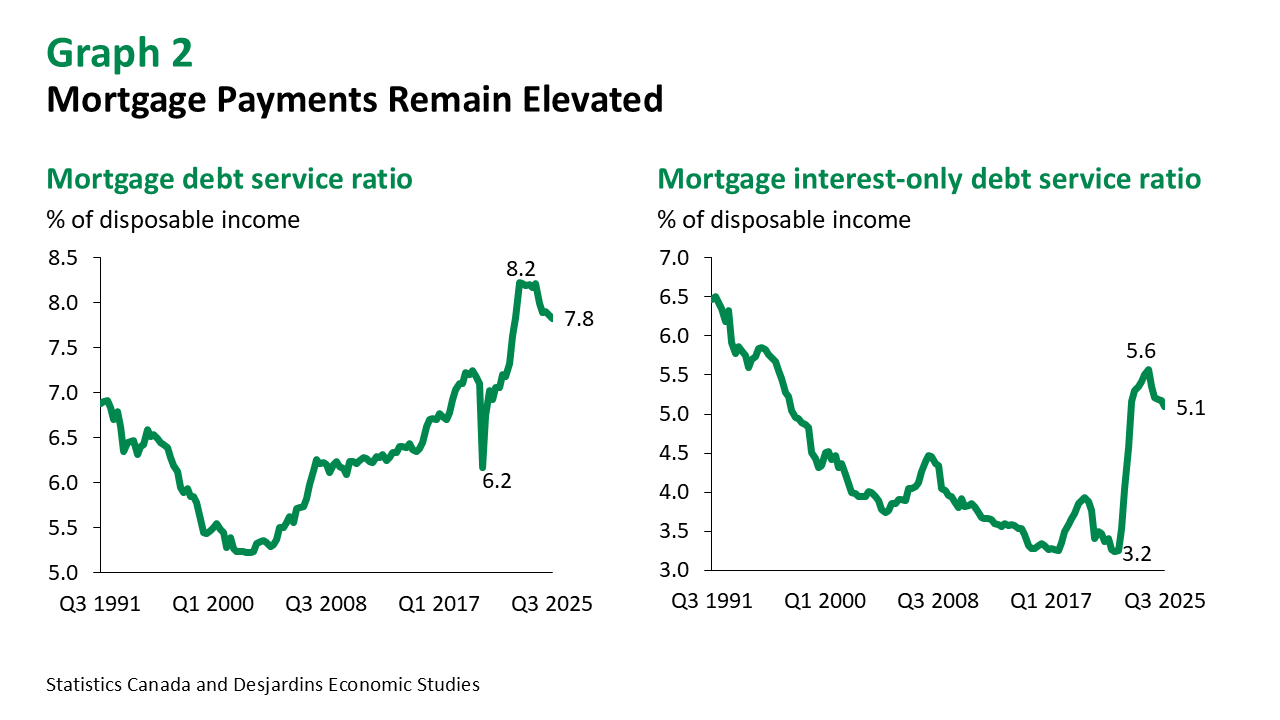

- The household debt service ratio—the share of disposable income directed toward debt payments—dipped slightly to 14.6% after its rise in Q2. This isn’t far from the unprecedented peak of 15.1% reached in Q1 2023. Mortgage principal payments rose 2.1% in Q3, while mortgage interest payments declined by 0.9%. The mortgage-only debt service ratio stood at 7.8% in the third quarter, slightly below the record high of 8.2% reached in Q1 2023 but still elevated (graph 2).

Comments

The Q3 2025 balance sheet release made clear that while Canadian household finances advanced in the quarter, gains were likely not evenly distributed. The wealthiest 20% of households held almost 70% of financial assets and were therefore most likely to benefit from the quarter’s stock market rallies—the S&P/TSX surged 11.8% and the S&P 500 climbed 7.8%. The savings rate External link. edged up a tick in the third quarter as household disposable income slightly outpaced nominal spending. Indeed, consumer spending External link. by Canadian households softened slightly in Q3 due in large part to lower spending on passenger vehicles.

Implications

Looking forward, higher monthly mortgage payments at renewal remain a key concern for many households, likely holding back consumer spending while encouraging savings in the near term. Our research External link. found that drag on employment attributable to the trade war this year is substantial. Nevertheless, the latest labour force data External link. show ongoing resilience so far in Q4. Wage gains are expected to slow further through the remainder of the year as labour demand weakens but should continue to outpace inflation. Canada continues to face trade uncertainty with volatility related to the CUSMA review expected in early 2026. Meanwhile, inflation concerns have receded and the Bank of Canada External link. has signalled that this rate cutting cycle is likely complete, barring any major shifts in the outlook.