- LJ Valencia

Economist

Economic News

Canada: The Trade Deficit Widened in June

August 5, 2025

Highlights

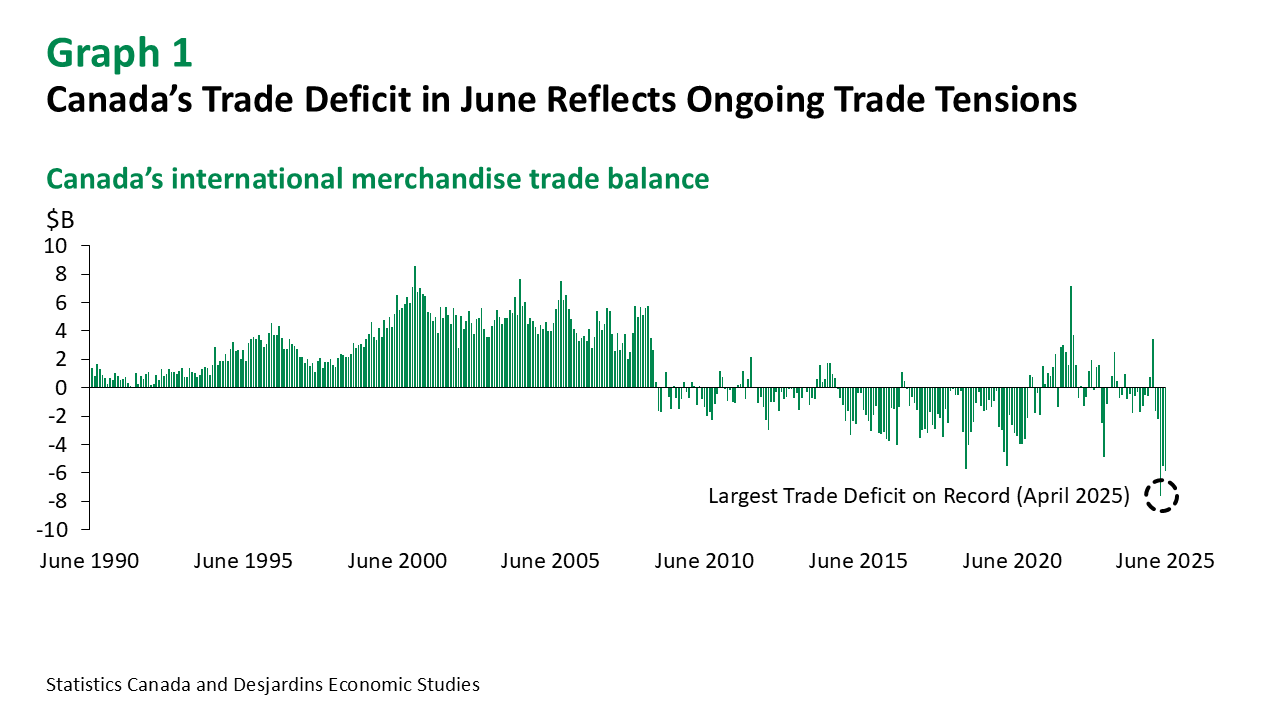

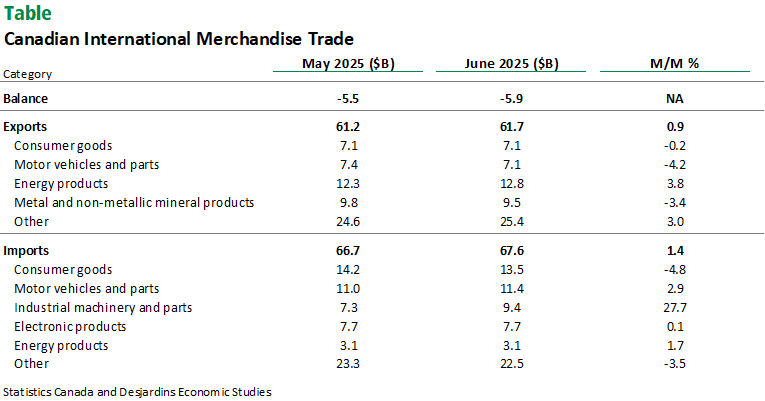

- Canada’s international merchandise trade deficit widened to $5.9B in June from $5.5B in the prior month (graph 1). This was slightly above the consensus expectation for a deficit of $6.3B. See table for more details.

- Goods exports rose by 0.9% m/m in June—a second consecutive increase. Imports rose by 1.4%—the first increase in four months. In real terms, exports were down 0.6% while imports increased by 2%.

- On a quarterly basis, nominal exports fell sharply by 12.8% q/q and imports decreased by 3.9%. After adjusting for prices, real exports and real imports fell by 9% and 1.5% in the quarter, respectively.

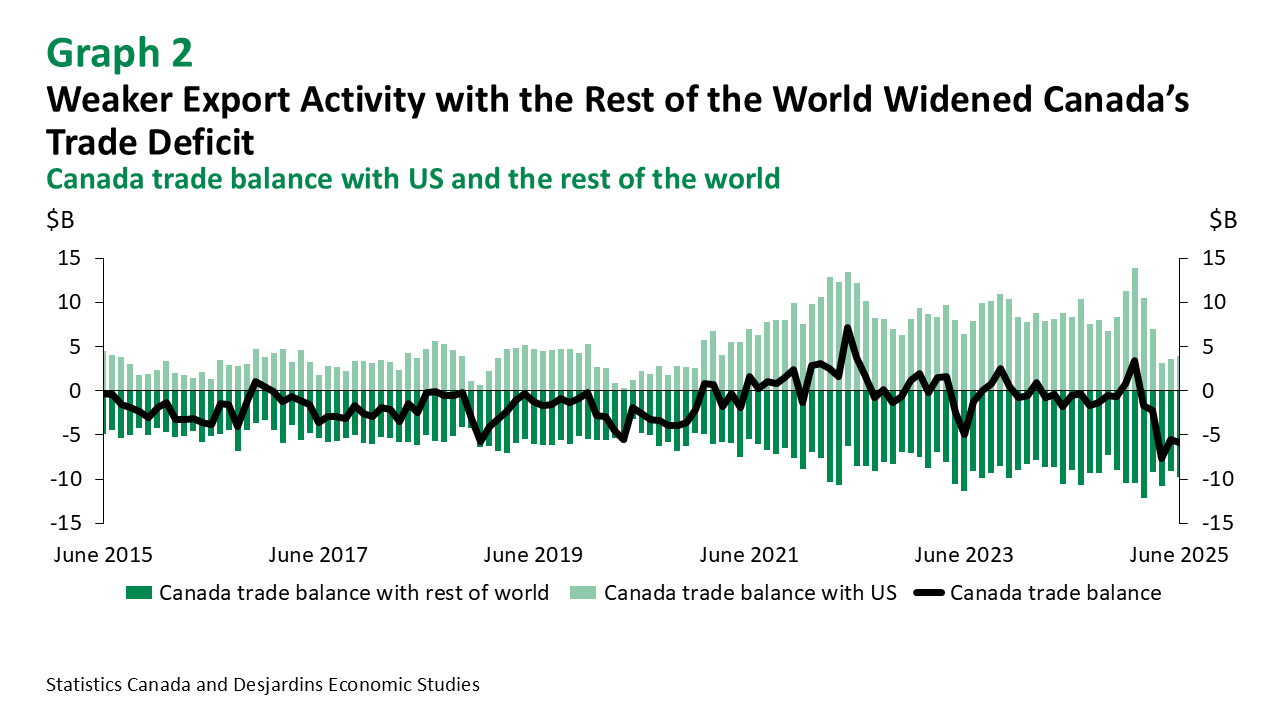

- Canada’s trade surplus with the US rose slightly from $3.6B to $3.9B in June (graph 2). Meanwhile, the trade deficit with countries other than the United States widened from $9.1B to $9.8B in the month.

- The services trade deficit narrowed in June to $659M. Service exports rose by 1% while service imports fell slightly by 0.2%.

Comments

Six out of 11 export categories experienced an increase in June, thanks to higher prices. Energy exports contributed the most to export growth in the month (3.8%), on the back of rising oil prices due to geopolitical tensions in the Middle East. Exports of farm, fishing and intermediate food products rose (6.7%) with broad gains across product subcategories, most notably live animals, canola and other crop products. In contrast, metal and non-metallic minerals fell (-3.4%), which can be primarily attributed to falling gold exports. In addition, aluminum, iron and steel product exports also decreased, coinciding with higher US tariffs on Canadian steel and aluminum.

On the import side, Statistics Canada again noted that the CBSA's Assessment and Revenue Management (CARM) initiative significantly revised import values from November 2024 to June 2025, so import data should be viewed cautiously. Five out of 11 categories posted increases. The largest moves were seen in the imports of industrial machinery, equipment and parts (27.7%) largely thanks to a high-value module import destined for an oil project off the coast of Newfoundland. Motor vehicles and parts posted a modest increase (2.9%), largely on higher imports of passenger cars and trucks from Mexico. This was enough to offset falling imports of motor vehicle engines and parts amid declining domestic motor vehicle production, likely due to ongoing trade tensions with our southern neighbour.

Implications

Today’s trade deficit points to Canada’s declining trade activity and ongoing tensions with its southern neighbour. As a result, net exports are expected to drag down Q2 growth by 7.1%. We expect GDP growth was about -0.5% to 0.0% in the quarter. This is above the Bank of Canada's July Monetary Policy Report forecast.

Looking ahead, ongoing trade tensions and volatility should heavily influence growth and the decisions of Canadian central bankers. Consequently, our recent analysis External link. on economic growth and projections External link. suggest a more subdued outlook for Canada’s economy in the coming quarters.