- Kari Norman

Economist

Economic News

Canada: October Housing Starts Chilled While Sales Warmed Up

November 18, 2025

Highlights

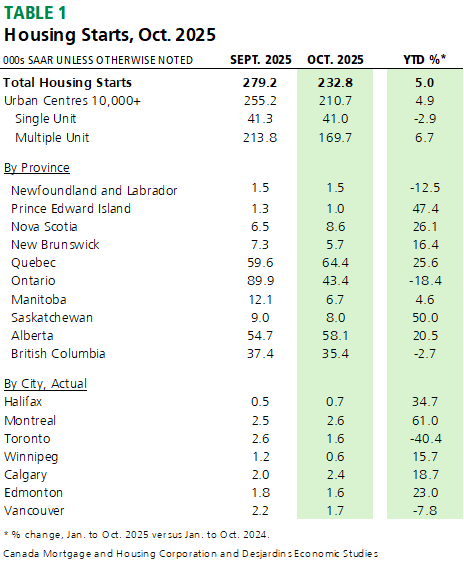

- The pace of housing starts in Canada slowed in October to 232.8k (saar) from 279k in September, pulling down the 6-month moving average to 269k. Table 1 summarizes key data points.

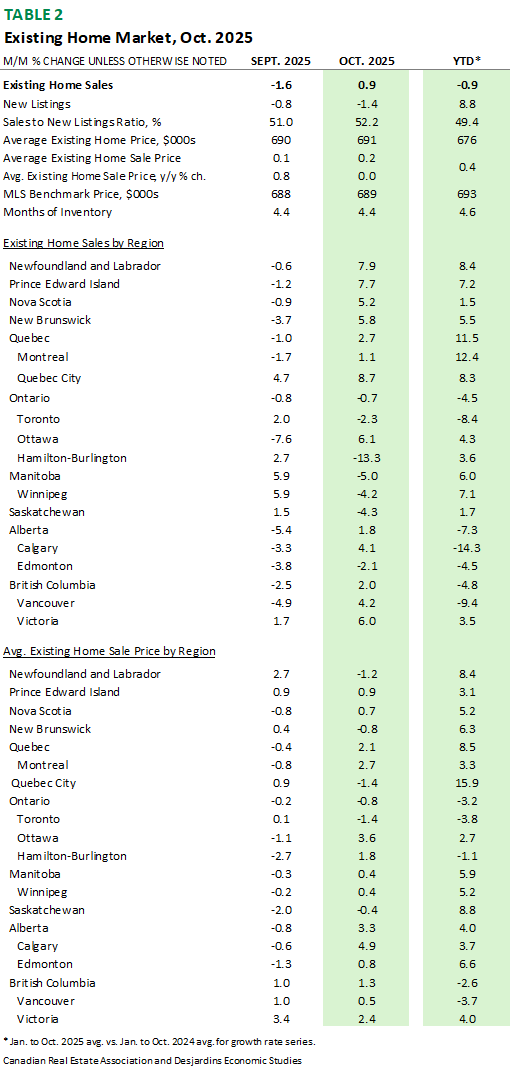

- Existing home sales in Canada edged up by 0.9% m/m in October. The average national sale price rose 0.2% m/m, while the benchmark price was essentially unchanged. Both remain well below their historic peaks reached in 2022. Table 2 summarizes key data points.

Comments

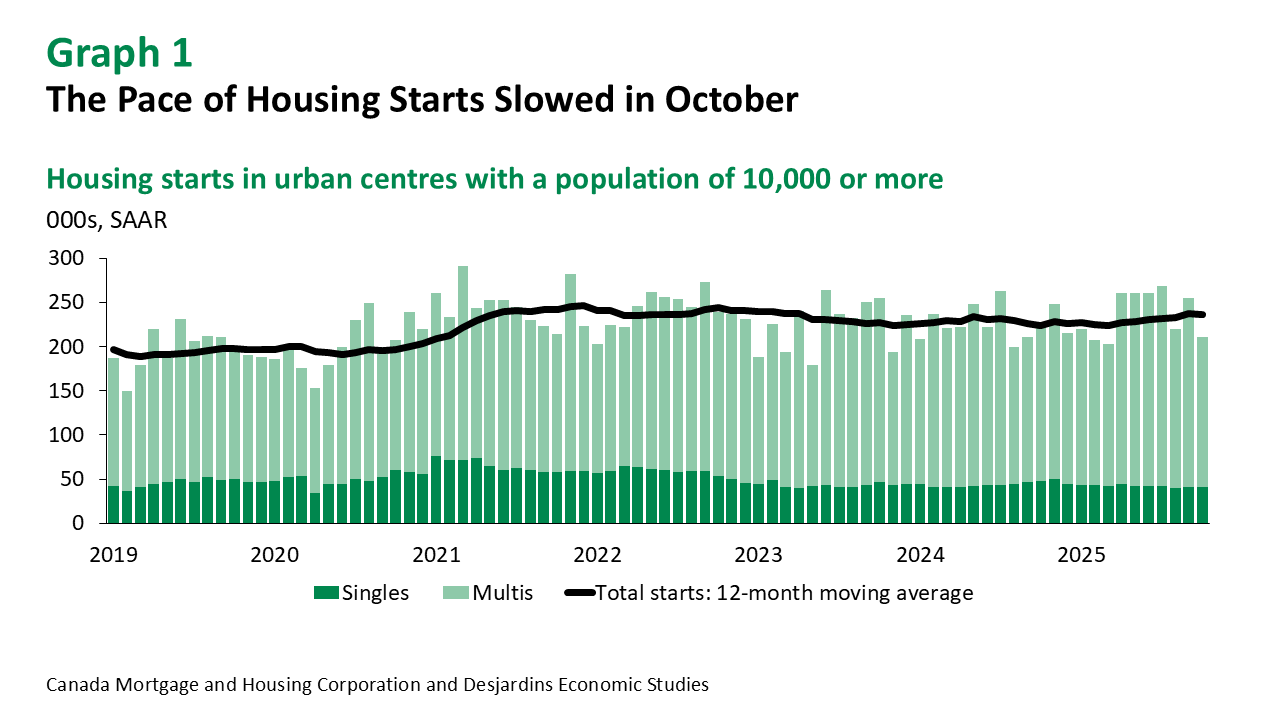

October’s seasonally adjusted housing starts slowed to 232.8k, well below the consensus of economic forecasters. As typically seen, the month-to-month variability was entirely within the multi-unit segment. Single family housing starts remained on par with the previous several months, albeit well below levels at the start of 2025 (graph 1).

The decline in homebuilding was driven by Ontario, with merely 43k starts last month, following 90k in September. One quiet month doesn’t make a trend; however, we will continue to watch this closely as reports of low condo presales in the province may signal further slowdowns in construction.

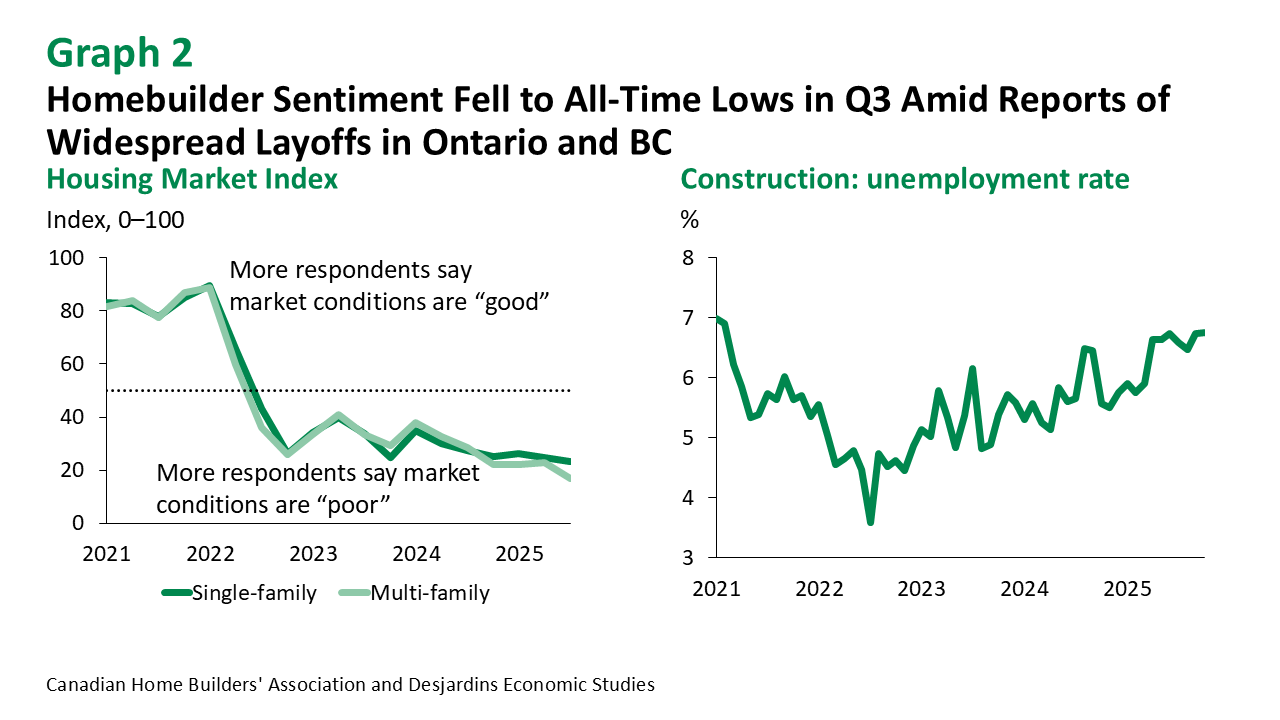

Despite robust housing starts in 2025 overall, homebuilder sentiment in Q3 plunged to record lows in both the single- and multi-unit sectors (graph 2). Declining confidence stemmed from ongoing trade uncertainty and hesitation among would-be first-time homebuyers waiting for the promised GST rebate to pass into law. Additionally, inflation in construction materials since 2020 has added an estimated $99,000 to the cost of building a 2,400-square-foot home. Mounting unemployment in the construction sector raises concerns about fewer projects breaking ground, reinforced by reports of unprecedented weakness in condo presales across key markets.

In the resale market, October home sales grew by 0.9% m/m. Sales remained within seasonal norms but came in well below October 2024 levels. This despite the lower mortgage rates, softer prices, ample listings in key cities and new government affordability measures External link. introduced at the end of last year such as 30-year amortizations for first-time homebuyers.

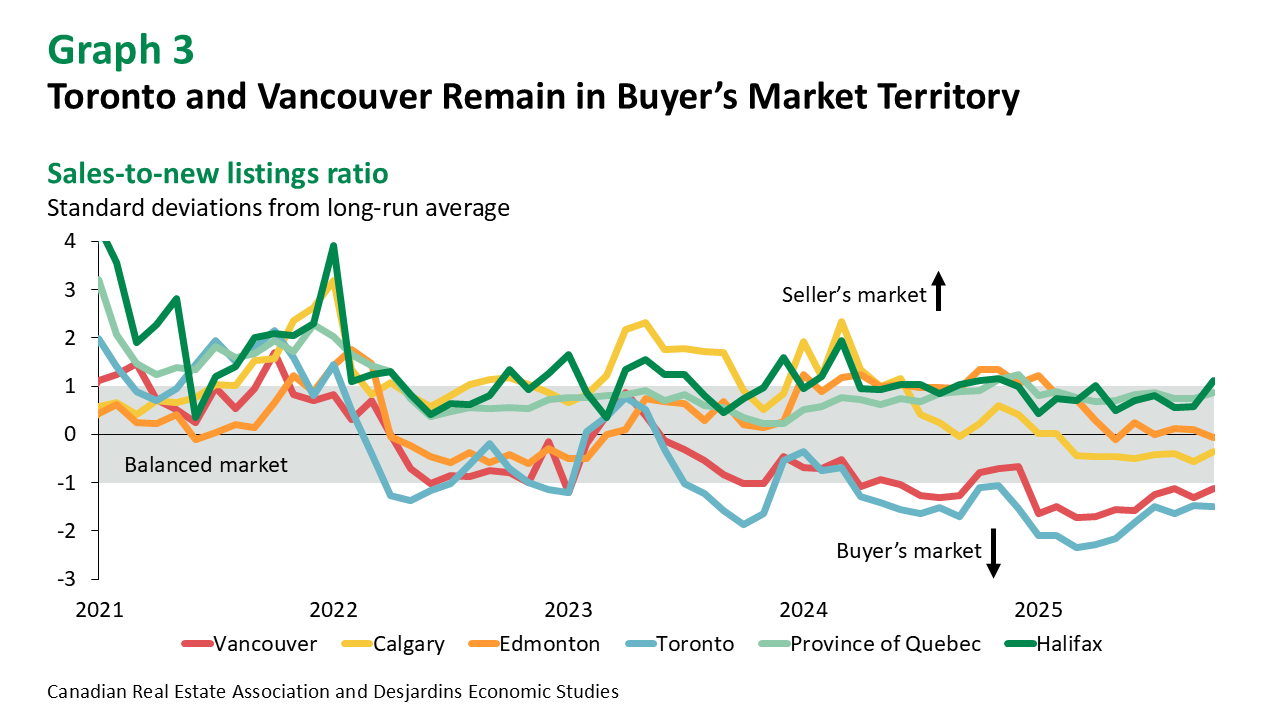

Nationally, new listings declined by 1.4% m/m and inventory held steady at 4.4 months in October—well above the post-2018 average of 3.7 months. The sales-to-new-listings ratio inched up from 51.0% to 52.2%, the highest level in 2025 albeit still balanced. Toronto and Vancouver continued in buyer’s market territory, while Halifax and the Province of Quebec edged towards a seller’s market (graph 3).

Implications

The Bank of Canada External link. (BoC) lowered the policy rate by 25-basis points to 2.25% in October, following a similar move in September External link.. Looking ahead, the BoC has signalled that further rate cuts are unlikely, limiting any additional savings to homebuyers and builders on financing costs. However, all levels of government seem to be increasingly rowing in the same direction on homebuilding, primarily in purpose-built rental and affordable units including co-op housing. Despite an uptick in rent CPI in October External link., our forecast for lower rental accommodation inflation External link. suggests renters will face less pressure to transition into homeownership.