- Kari Norman

Economist

Economic News

Canada: February Rebound in Housing Starts Hints at a Possible Early Spring Thaw

March 15, 2024

Highlights

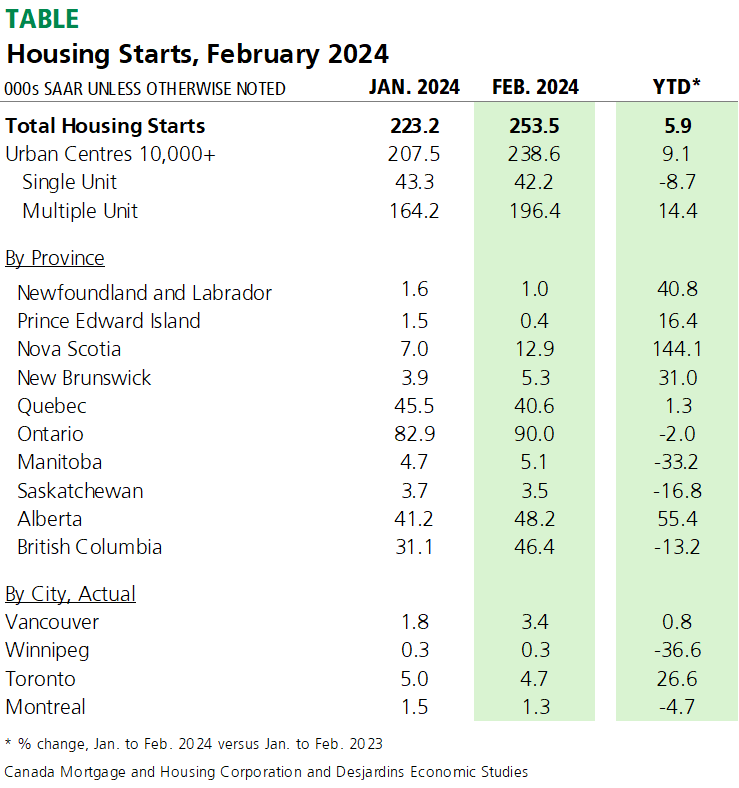

- Housing starts in Canada rebounded in February, to 253k (saar), with a significant upsurge in multi-unit housing leading the way. The table below summarizes key data points.

- Our tracking suggests real annualized GDP growth in the range of 1% to 1.5% annualized in the first quarter of 2024. That’s more than the Bank of Canada’s forecast of 0.5% published in January.

Implications

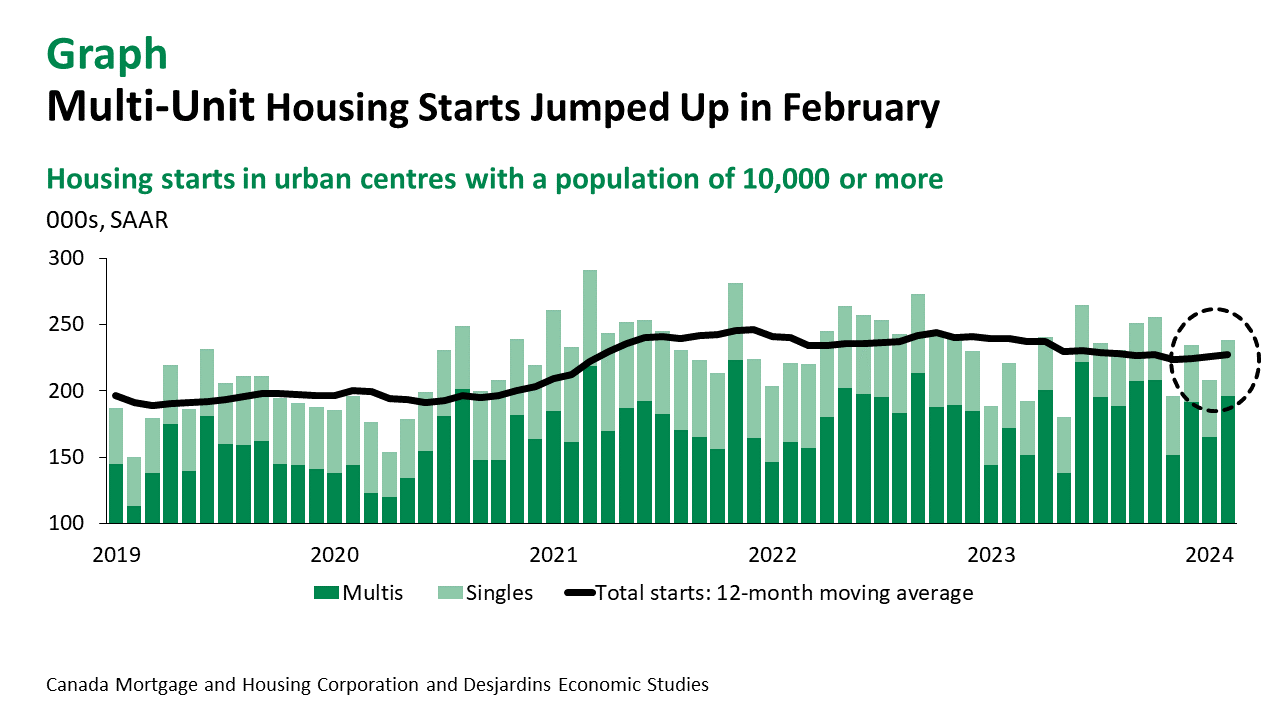

Despite the heavy influence of the prevailing high interest rate environment, the Canadian housing market continues to forge ahead (graph). Significant variation across regions highlights the nature of housing, where local conditions dictate market dynamics. The pace of construction picked up in Ontario, Alberta and BC, while pulling back slightly in Quebec.

Often volatile multi-unit residential construction continued to dominate housing starts, up almost 15% so far this year over the same period a year ago. Single-unit starts, on the other hand, are down nearly 9% year-to-date as compared to these same months last year. This may reflect a shift toward more economically viable housing solutions in an era of sustained elevated home prices paired with high interest rates. Moreover, it aligns with urban planning goals aimed at sustainable and efficient land use. The spring construction season will no doubt benefit from the unseasonably warm weather at the start of 2024 as well.

Historically new construction typically closely follows home purchases. Though that was not the case in 2022–23, home sales External link. strength mirrored a pickup in starts more recently. Next week’s expected housing sales data release will show whether this trend continues in February.

With inflation slowing External link., the Bank has begun to soften its tone External link.. Even with the February uptick in housing starts, we remain of the view that the Bank of Canada will begin to gradually unwind interest rate hikes starting in June. Nonetheless, we don’t anticipate a surge in construction activity in 2024 despite some relief in borrowing costs that less restrictive monetary policy would provide. The construction industry continues to suffer from labour shortages, weak homebuilder sentiment and inflation in building materials costs. Indeed, we expect External link. that housing starts won’t return to 2023 levels for the next several years.