- Kari Norman

Senior Economist

Economic News

A Weak December Caps a Stop‑Start Year for the Canadian Housing Market

January 15, 2026

Highlights

- Existing home sales in Canada fell by 2.7% m/m in December, on a seasonally adjusted basis. The average national sale price and benchmark price were essentially unchanged. Both price measures remain well below their historic peaks reached in 2022. Table 1 summarizes key market indicators.

Comments

Looking back at last year, home sales began 2025 poised for growth, with several interest rate cuts already in place, but trade war uncertainty sent many potential homebuyers back to the sidelines. A mid-year rally lent some optimism, though the year ended not with a bang but a whimper. Existing home sales in December remained within seasonal norms but came in well below December 2024 levels. This despite the lower mortgage rates, softer prices, a buyer’s market in key cities and federal affordability measures External link. introduced late in 2024, including 30‑year amortizations for first-time homebuyers.

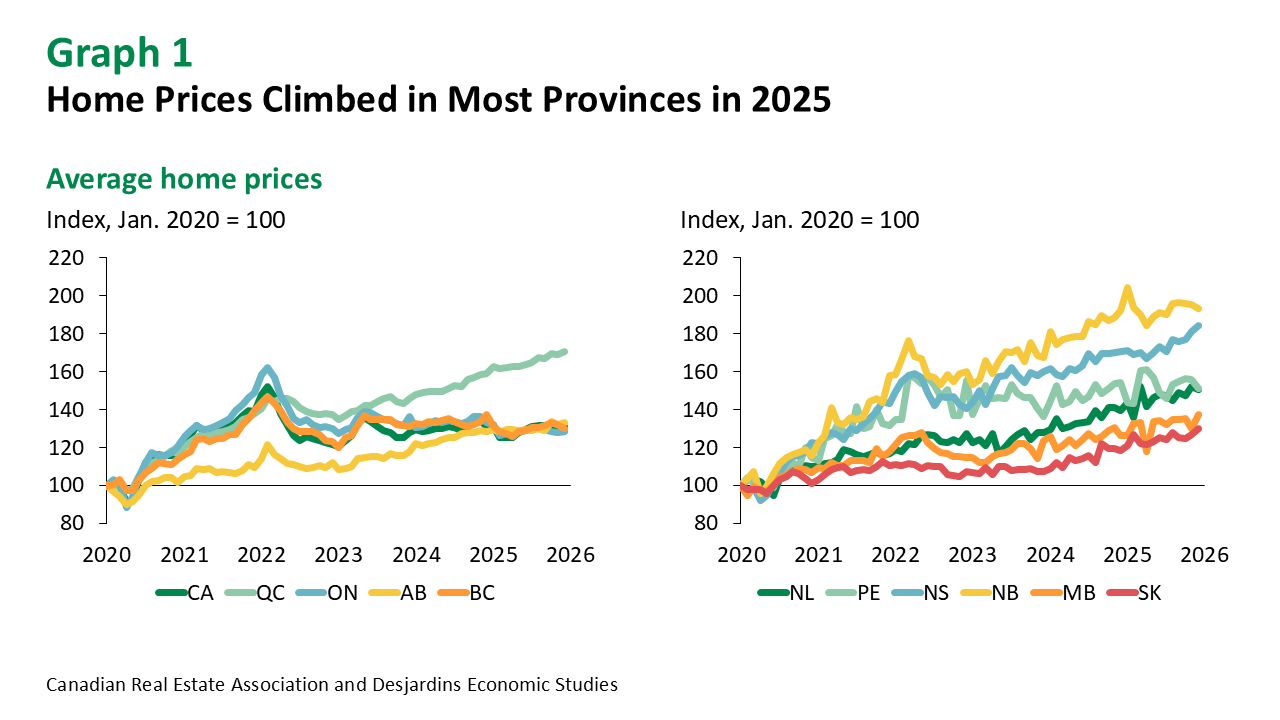

Regionally, December home sales were particularly weak in Alberta and Quebec. Sales declines in Ontario and BC were milder than the national average last month. Only the Maritime provinces had sales gains in December, albeit following November declines. Looking at the year as a whole, national averages continued to mask strong regional variations, as softer prices in Ontario and BC brought down the annual headline figure (graph 1). All the other provinces posted strong gains in selling prices last year, with Saskatchewan and Newfoundland and Labrador leading the way at about 8%.

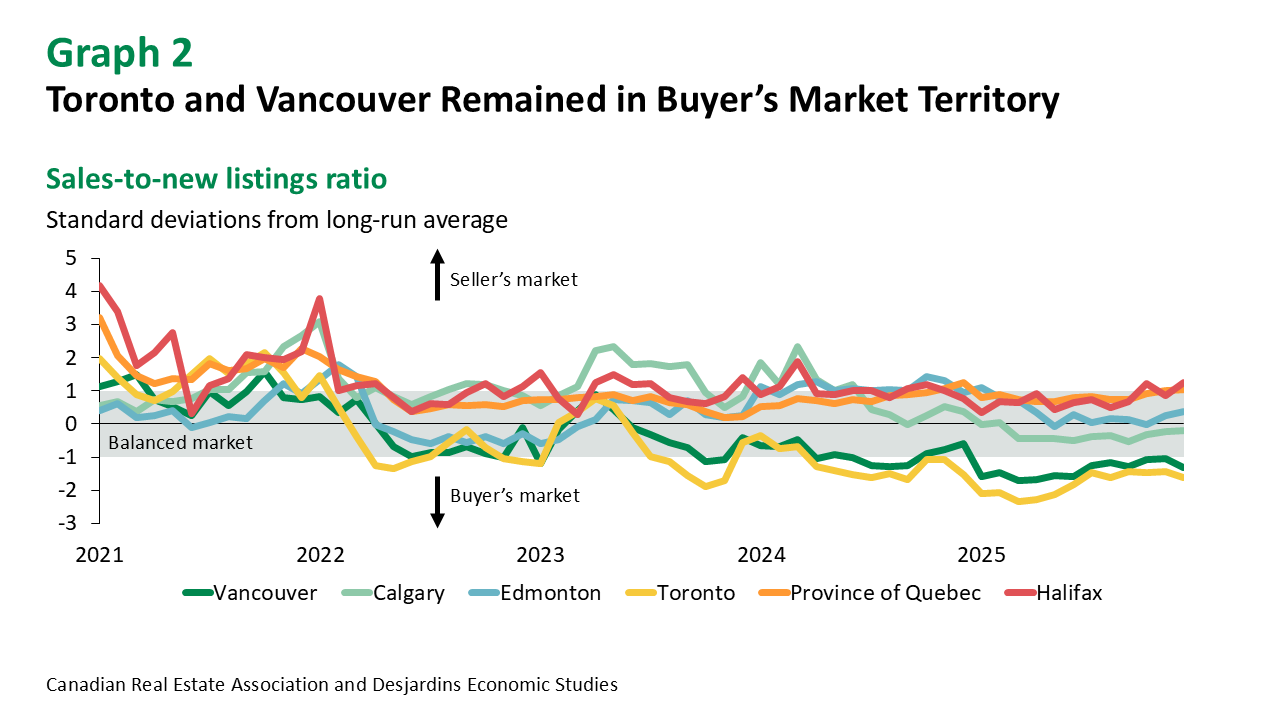

Nationally, new listings decreased by 2.0% m/m in December—the fourth consecutive monthly drop. The inventory level ticked up to 4.5 months—well above the post‑2018 average of 3.7 months. The sales-to-new-listings ratio eased slightly to 52.3%, remaining comfortably within balanced market conditions. Toronto and Vancouver continued in buyer’s market territory (graph 2). Both cities have experienced exceptionally subdued sales throughout last year, even as selling prices declined and interest rates eased.

Implications

We expect the Bank of Canada to leave policy rates unchanged at its January rate announcement and maintain this stance for the foreseeable future. Governing Council has indicated that the current policy rate level is appropriate to keep inflation close to the 2% target while supporting the economy through the ongoing trade disruptions. As a result, the potential for further reductions in monthly mortgage payments is limited.

Looking ahead, economic conditions External link. indicate that the spring housing market may be poised for a solid advance in sales. But with a higher level of inventory in Canada’s largest provinces than a year ago, prices may not rise as quickly. At the same time, our outlook for modest rental accommodation inflation External link. suggests renters may face less pressure to transition into homeownership. That said, local housing market conditions vary widely.