- LJ Valencia

Economist

Economic News

Canada: Canada’s Labour Market Remains Soft Despite Solid September Hiring

October 10, 2025

Highlights

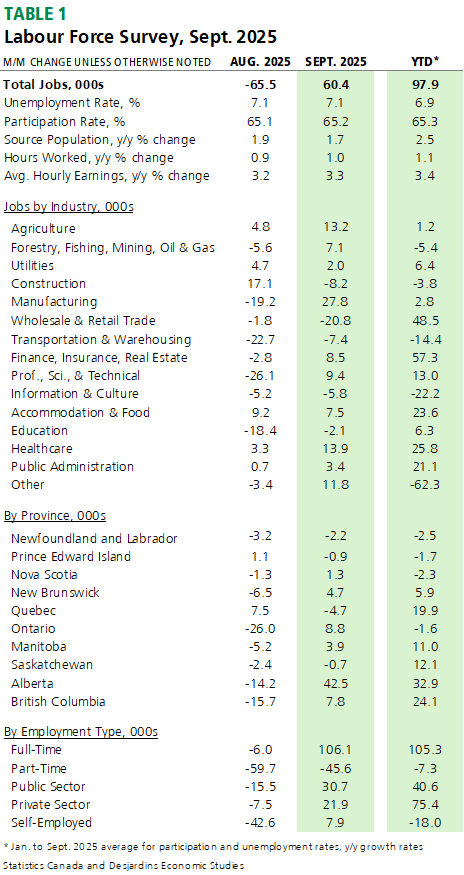

- Canadian employment increased in September 2025 by 60k jobs, nearly reversing August’s decline of around 65k jobs. Today’s print surprised economic forecasters who anticipated an advance of 5k. The unemployment rate was unchanged at 7.1%, also slightly better than expected. Average hourly wage growth increased 3.3% y/y in September, a slight uptick from August. Table 1 summarizes key data.

- Reflecting the recent employment data, our tracking suggests real GDP growth at around 0.5% annualized in the quarter, just shy of the Bank of Canada’s July Monetary Policy Report forecast of 1% annualized.

Comments

The Canadian labour market showed renewed signs of life in September, following two consecutive months of job losses. All of the job gains were in full-time employment as part-time employment fell. Employment in the manufacturing and agriculture sectors posted their first increase since January. Despite ongoing trade tensions, manufacturing jobs have risen by nearly 3k since the start of the year. Alberta recorded the largest employment gain in the month, more than offsetting losses in July and August. Ontario and BC saw some job gains as well.

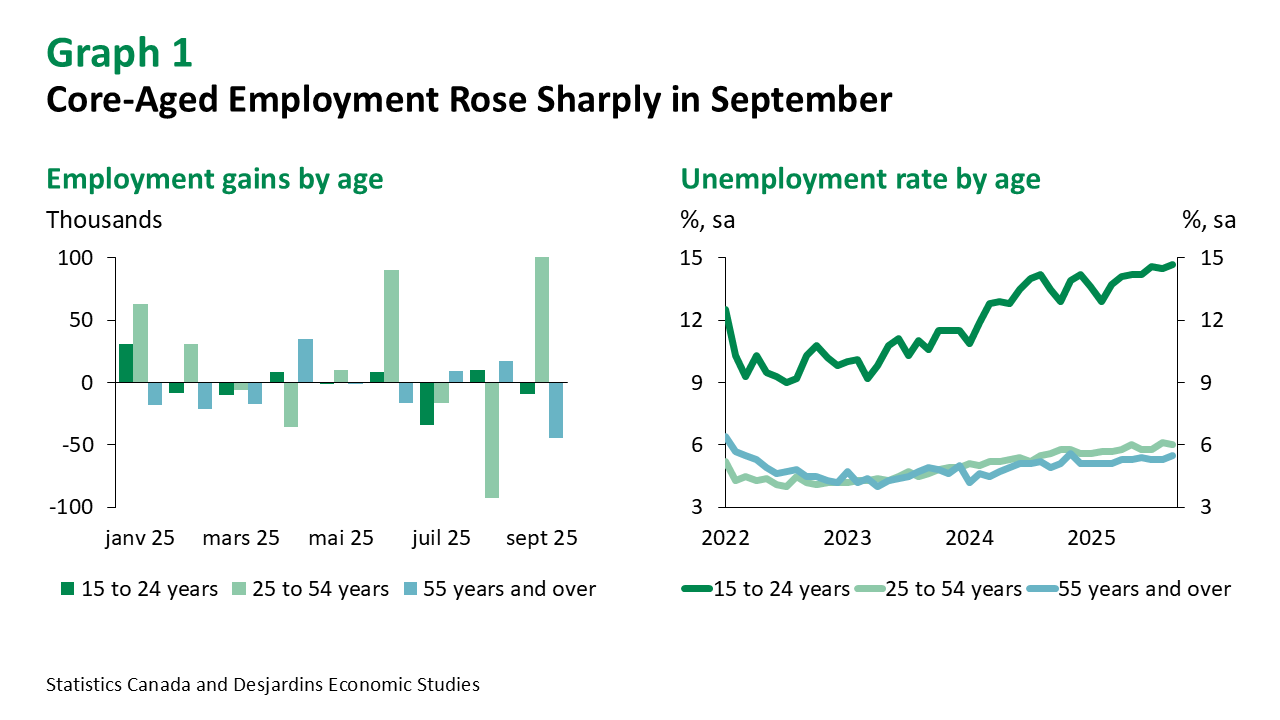

Despite the job gains, labour market conditions show a mixed picture as the unemployment rate did not move in the month. The unemployment rate for core-aged workers (ages 25 to 54 years) fell slightly to 6.0% in September from 6.1% (graph 1). This comes as employment gains were concentrated in core-aged workers at 109k jobs, surpassing losses of 93k in August. Following the end of the summer job market, youth (ages 15 to 24 years) lost about 9k positions, reversing some of the job gains in the prior month. The youth unemployment rate rose to 14.7%, the highest rate since September 2010, excluding the pandemic. Our recent report External link. looked at the drivers of high youth unemployment, some which are starting to fade.

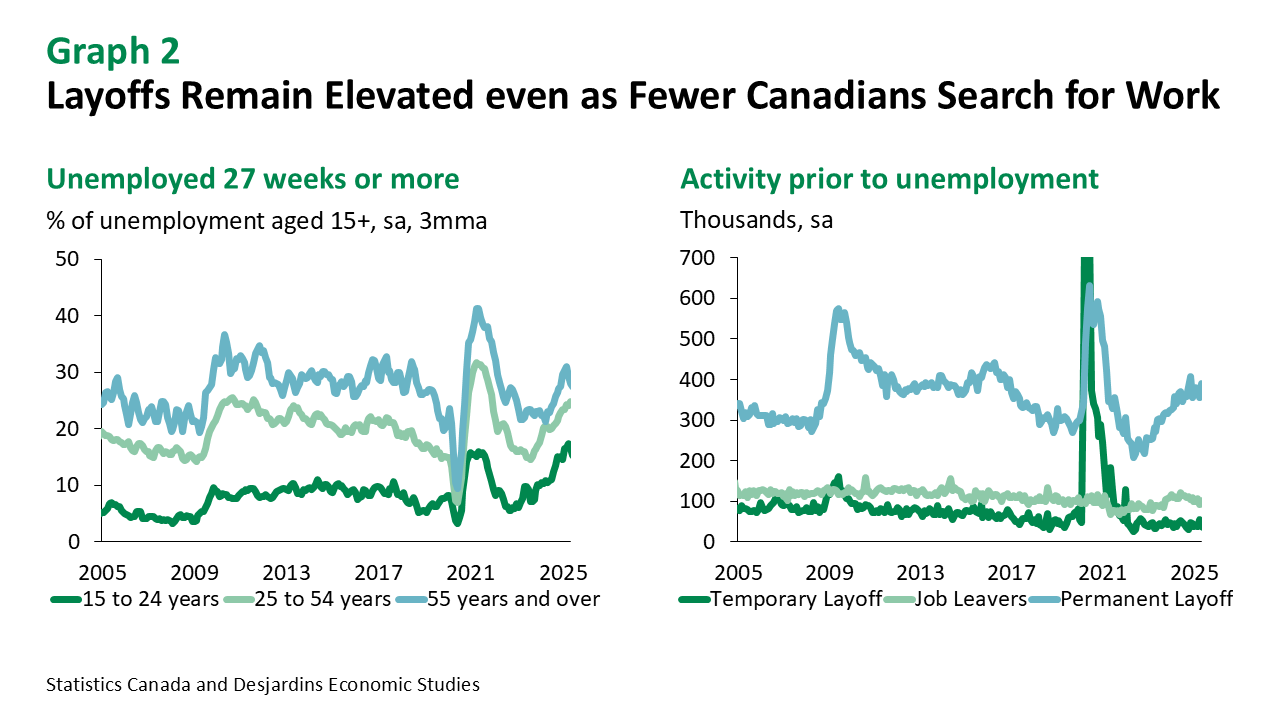

While the headline unemployment rate held steady in September, permanent layoffs continued to rise, albeit remaining below recessionary levels (graph 2). At the same time, the share of core-aged job searchers experiencing at least 6 months of unemployment fell slightly in the month.

Average wage growth edged higher in September to 3.3% year-over-year, though it remains well below the elevated post-pandemic levels of over 5%. Wage growth is expected to remain subdued throughout much of 2025, as labour demand weakens and economic activity slows down. That said, wage gains should continue to outpace inflation, supporting ongoing real earnings growth.

Implications

Looking ahead, as indicated in our recent outlook External link., domestic demand appears to be holding steady despite the economic drag caused by trade uncertainty. The trade environment continues to improve, especially as retaliatory tariffs are removed, likely keeping inflation close to the Bank of Canada’s 2% target. This provides the Bank with much-needed wiggle room for further easing. As such, we anticipate that the Bank will cut the policy rate again at its next meet in late October, to 2.25%.