- Randall Bartlett

Deputy Chief Economist

Weekly Commentary

How Much Is Defence Spending Really Boosting the Canadian Economy?

March 6, 2026

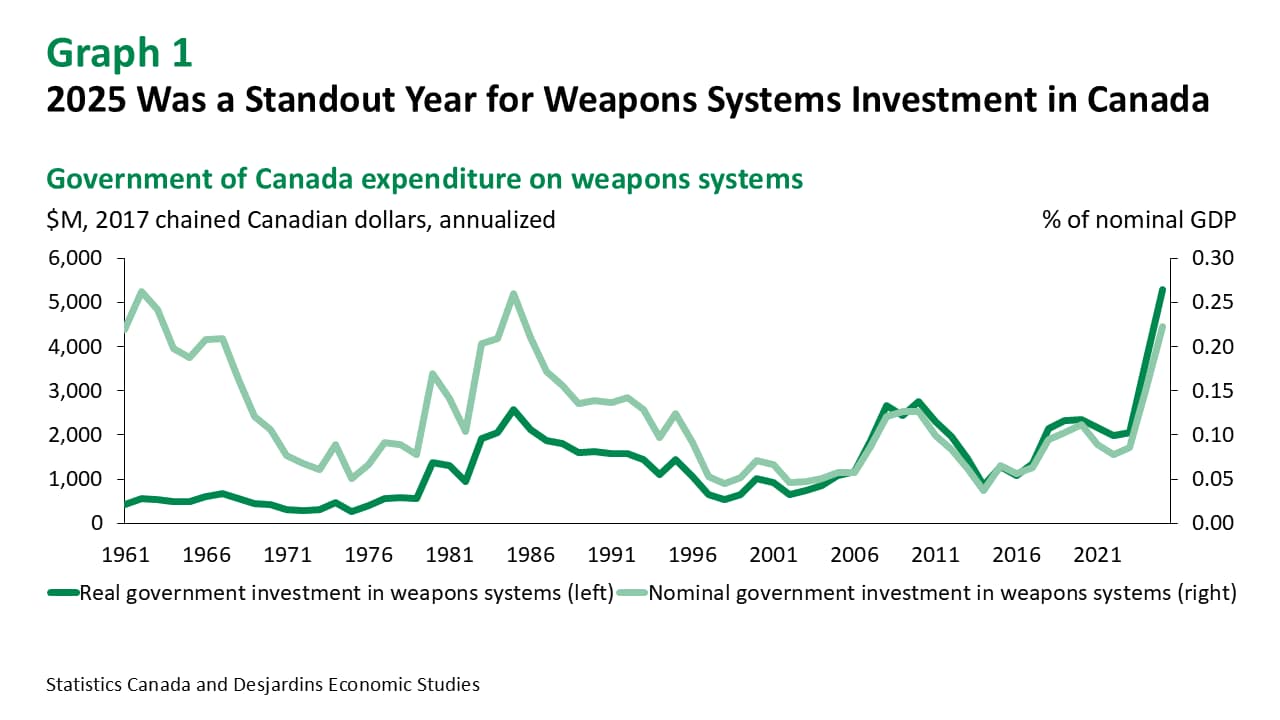

One of the most surprising contributions to the advance in domestic demand in Q4 2025 was the eyewatering increase in government investment in weapons systems. In inflation-adjusted terms, Canadian purchases of weapons jumped more than 800% q/q annualized at the end of the year relative to Q3. That follows a more than 1,300% advance the prior quarter. According to Statistics Canada, the level of real expenditure on weapons systems by Canada in 2025 was nearly double the historic peak reached in 2010 during the War in Afghanistan (graph 1) and was entirely concentrated in the second half of the year. Keep in mind that government investment in weapons systems still comprised only 0.2% of nominal GDP last year, falling short of the early post‑WWII period and mid‑1980s as a share of total output. But if spending on weapons systems in 2026 looks anything like it did in the second half of 2025, this year could see the largest share of output going to defence in at least the last 65 years.

Numbers of this magnitude beg the question: what is this money being spent on? The recent GDP data and Statistics Canada’s analysis that came with it don’t give much detail. According to the statistical agency External link., military weapons systems include “vehicles and other equipment such as warships, submarines, military aircrafts, tanks, missile carriers and launchers.” What they don’t include are single-use weapons (e.g., ammunition, missiles, rockets, bombs) and defence non-residential structures and engineering (e.g., military bases, military airports). Importantly, spending on weapons systems as it’s included in GDP is determined on a quarterly, seasonally adjusted basis. It’s also calculated using accrual-accounting principles External link., meaning the investment isn’t expensed all at once but rather spread over the useful life of the asset.

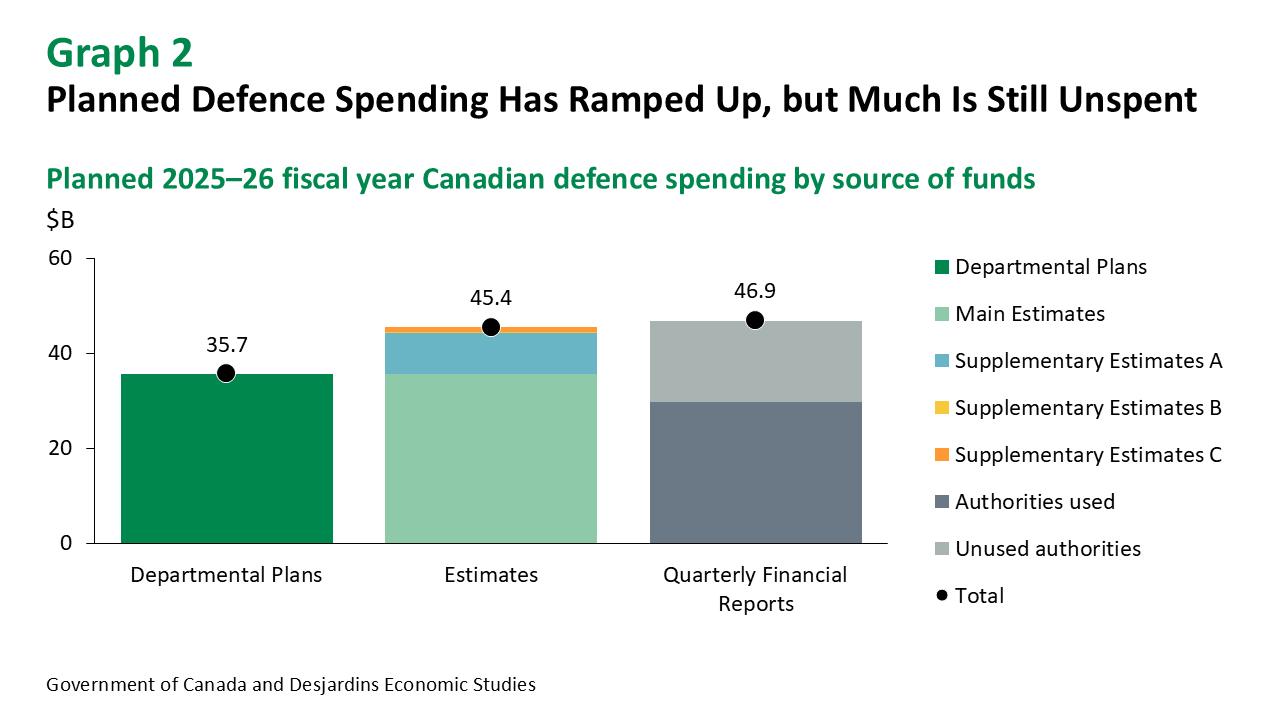

Data on weapons systems investment can come from several sources of defence spending information published by the Government of Canada (GoC). These include the budget External link.; Departmental Plan External link.—what the GoC says it plans to spend over the coming year; Main Estimates External link.—the initial ask for funding from Parliament for the coming fiscal year; and Supplementary Estimates (A External link., B External link. and C External link.)—subsequent asks to Parliament for additional funding for the current fiscal year beyond what was in the Main Estimates (graph 2). Notably, all this information is published on an annual, fiscal-year basis and uses expenditure or cash-accounting principles, meaning the money is accounted for when it’s spent as opposed to spread out over the useful life of the asset. This is also how NATO accounts for defence spending to evaluate how close countries are to reaching their commitments. These documents are to be read in conjunction with the Department of National Defence’s (DND’s) Quarterly Financial Report External link., the latest of which was published for Q4 2025 on the same day that GDP was released. This is also one of the key documents Statistics Canada has pointed to as the source of its data on investment in weapons systems. In contrast to these financial reports, information on federal government finances from the monthly Fiscal Monitor External link. is published on an accrual basis (subject to some caveats, including those outlined here External link.).

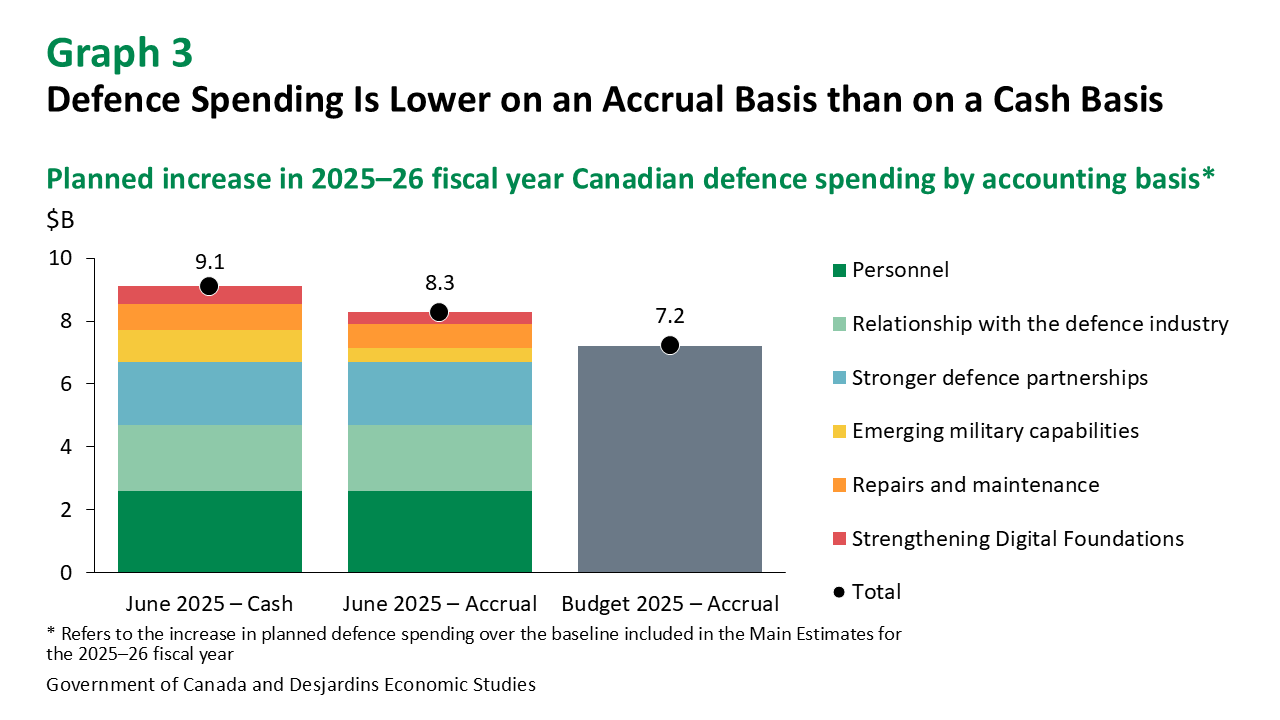

Putting these pieces together, we believe Statistics Canada may be overestimating the economic impact of the Government of Canada’s expenditure on weapons systems. First, it’s unclear what parts of the federal government’s current defence spending are included under weapons systems for the purposes of calculating GDP and when they were included. For example, news reports External link. suggest the latest GDP numbers could include Kingfisher search-and-rescue aircraft and Cyclone maritime helicopters. However, these may not constitute weapons systems as outlined in Statistics Canada’s own definition, or at least might not have met the definition before Q3 2025. Instead, these expenditures could reflect the ramp-up in “defence spending” associated with the transfer of the control and supervision of the Canadian Coast Guard from Fisheries and Oceans Canada to DND on September 2, 2025. (Note that Statistics Canada has privately challenged this assertion since the release of Q4 2025 GDP.) Second, it’s not clear how Statistics Canada is transforming a sharp increase in annual cash spending on defence into quarterly, seasonally adjusted investment on weapons systems on an accrual basis that conforms to the methodology for calculating GDP. Defence spending forecasts External link. published by the Government of Canada last June illustrate the importance of these accounting differences, with planned new capital spending on defence about a third lower this year on an accrual basis than on a cash basis (graph 3). Indeed, if these new capital assets had been properly accounted for in Q4 2025, one would expect to see corresponding transactions in the Fiscal Monitor, which doesn’t appear to be the case. As such, some of the recent spike in weapons systems investment may be the result of a methodological change as opposed to actual new spending, and this investment could be revised lower in the future.