- Randall Bartlett

Deputy Chief Economist

Economic News

Canada: The Bank Will Look Through September’s Inflation Surprise as the Economy Remains Weak

October 21, 2025

Highlights

- Headline CPI rose 2.4% y/y in September, up from 1.9% y/y in August and above the consensus expectation of economists (2.2%). Prices moved up 0.1% month‑over‑month and rose 0.4% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Comments

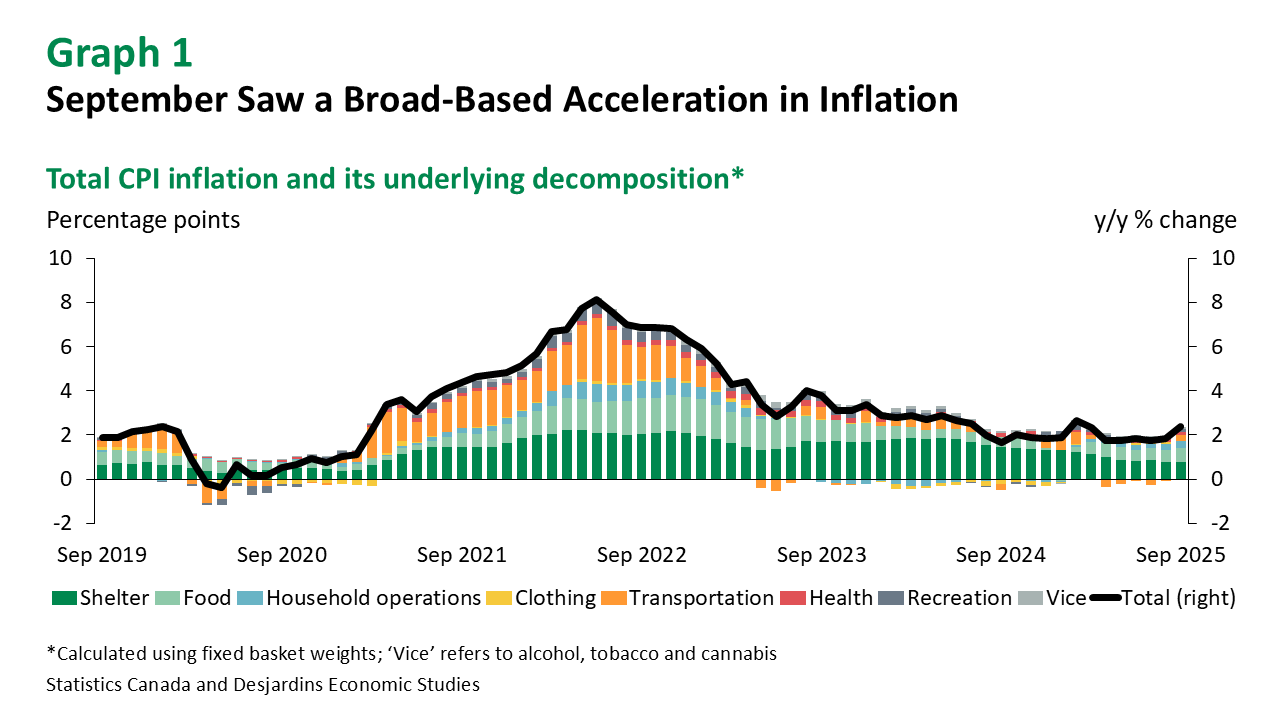

Headline inflation came in above the Bank of Canada’s (BoC’s) inflation target in September for the first time since March 2025. The increase was broad based, with most aggregate price categories seeing an acceleration over August (graph 1). This is in part due to base effects, which are the impact on year‑over‑year inflation of a sharp drop in month‑over‑month inflation a year ago. But on a month‑over‑month basis, higher costs for gasoline, travel tours, groceries and rents all helped to drive September’s price gain. This despite the federal government significantly reducing tariffs on imports from the US, which has yet to show up meaningfully in goods prices. (See our analysis External link. on the inflationary and economic impacts of reducing federal countertariffs.)

Gasoline prices increased 1.9% month‑over‑month in September because of refinery disruptions and maintenance in the United States and Canada. This meant the drag from energy prices on year‑over‑year headline inflation was more muted than it was in August. That said, headline inflation would have been about 0.6 percentage points higher in September, at 2.9% y/y, if it weren’t the elimination of the federal consumer carbon tax in April (graph 2). (See our analysis External link. on the inflationary impact of eliminating the federal price on pollution.)

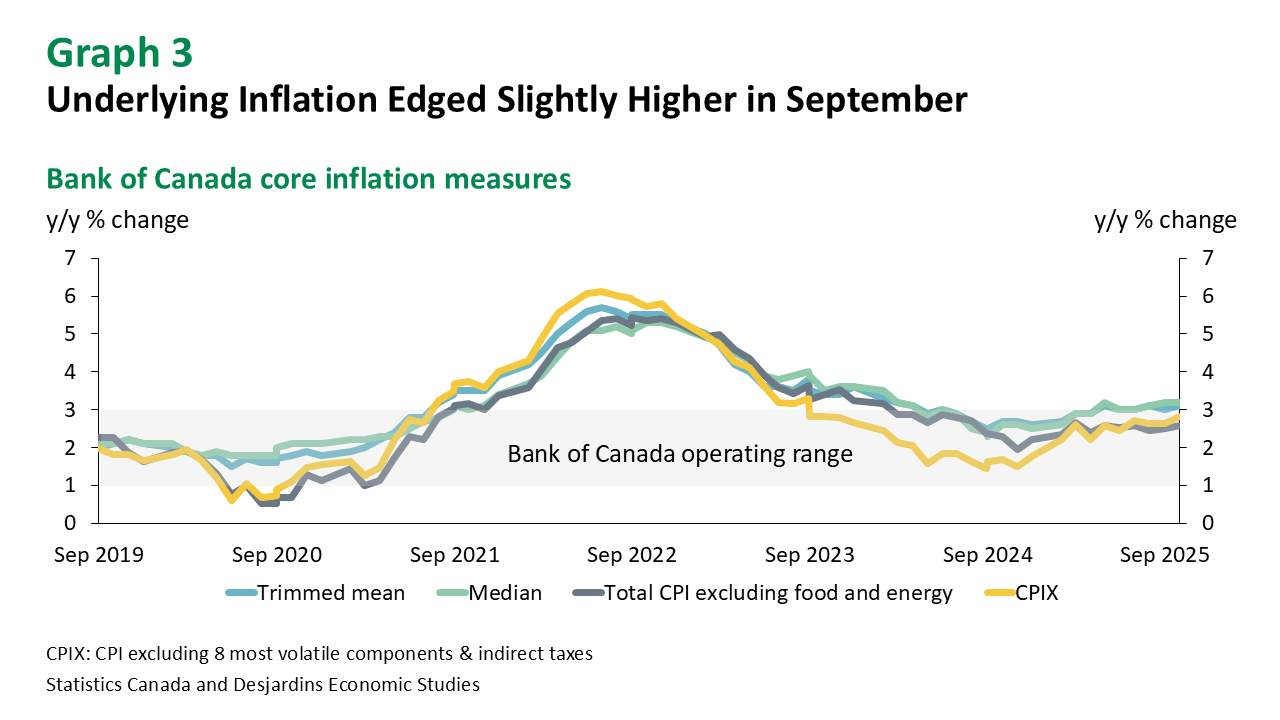

Turning to underlying CPI inflation, the news was somewhat better. The Bank of Canada’s (BoC’s) preferred measures of core inflation—CPI median and trimmed mean—accelerated modestly in September, to around 3.2% y/y (graph 3). Traditional measures of underlying inflation—total CPI inflation excluding food and energy and total CPI inflation excluding the eight more volatile components—were more muted but also edged higher to between 2.6% and 2.8% y/y. However, analysis by the Macro Strategy team suggests that the distribution of price growth actually shifted somewhat lower in September, with the share of categories experiencing annual growth above 3% declining slightly.

Implications

While the higher‑than‑expected pace of inflation in September may complicate the Bank of Canada’s messaging, a good part of the acceleration in the month can be explained by events a year ago as opposed to what is happening today. As such, we think that headline inflation could comfortably return to around 2% in the fourth quarter, supported by the recent reduction in retaliatory tariffs on goods imports from the US. When combined with the Bank’s downbeat business and consumer surveys, a still elevated unemployment rate and an economy that looks like it might barely manage to escape a recession in Q3, we remain of the view that the BoC will cut the policy rate by another 25 basis points at its upcoming meeting.