- LJ Valencia

Economist

Economic News

Canada: Stable Inflation in November Provides Some Measure of Holiday Cheer

December 15, 2025

Highlights

- Headline CPI rose 2.2% y/y in November, matching the October pace but slightly below the consensus expectation of economists (2.3%). Prices moved up 0.1% month-over-month and rose 0.2% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Comments

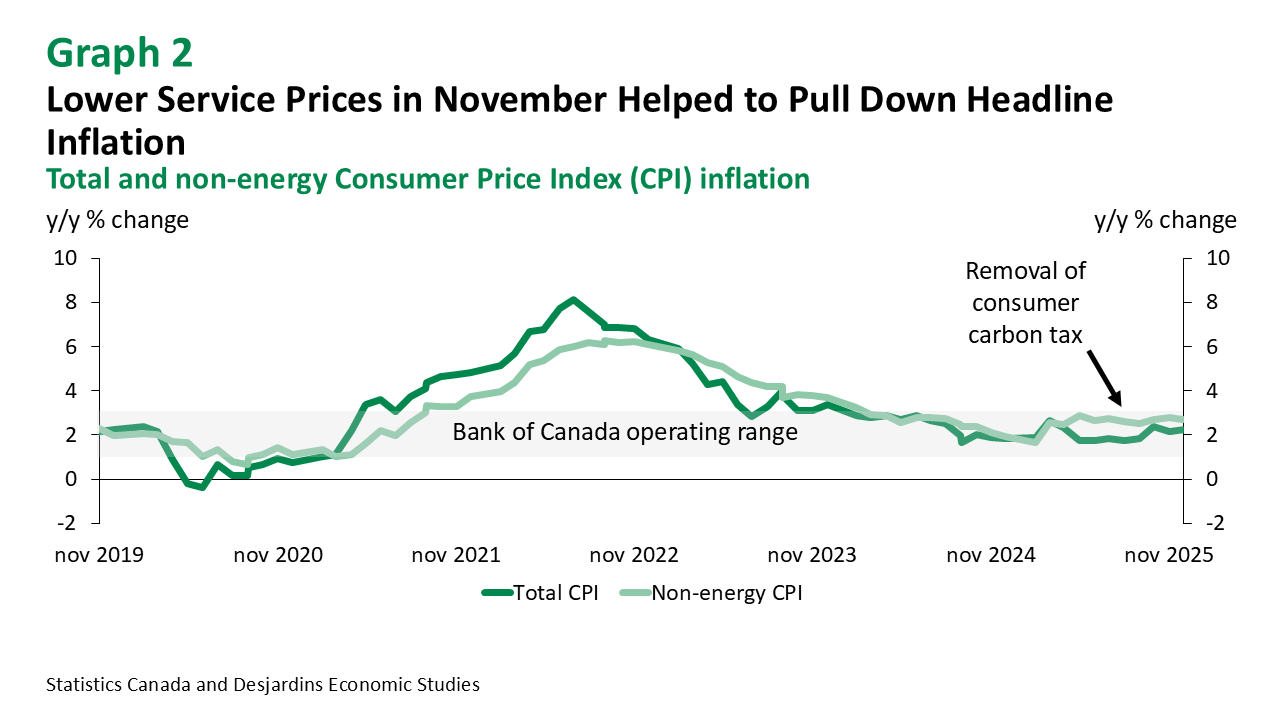

Headline CPI inflation remained close to the Bank of Canada’s (BoC’s) inflation target in November. Services prices played a big part, advancing by 2.8% y/y last month, down from 3.2% in October (graph 1). Travel tour prices fell drastically from a year earlier (-8.2%) due to lower demand for US destinations. Moreover, traveller accommodation prices slumped more sharply in November (-6.9%) than in October (-0.6%), largely due to a base-year effect from a surge in November 2024 linked to high-profile concerts in Toronto. Lastly, the pace of rent prices slowed during the month, as price growth eased across most regions. But it wasn’t all good news for services inflation, cellular services prices continued to accelerate, up 12.7% in November from 7.7% in the previous month.

In contrast to slowing services inflation in November, the cost of goods was on the rise. Prices of food purchased from stores accelerated to 4.7% y/y in November from 3.4% in October. This was the largest year-over-year advance since December 2023. The increase in grocery price inflation was largely attributed to higher prices of fresh fruit. Elevated beef and coffee prices continued to be significant contributors to grocery inflation on an annual basis. At the same time, gasoline prices fell at a slower pace (-7.8%) relative to October (-9.4%). Still, headline inflation would have been about 0.4 percentage points higher in November, at 2.6%, if it weren’t the elimination of the federal consumer carbon tax in April (graph 2).

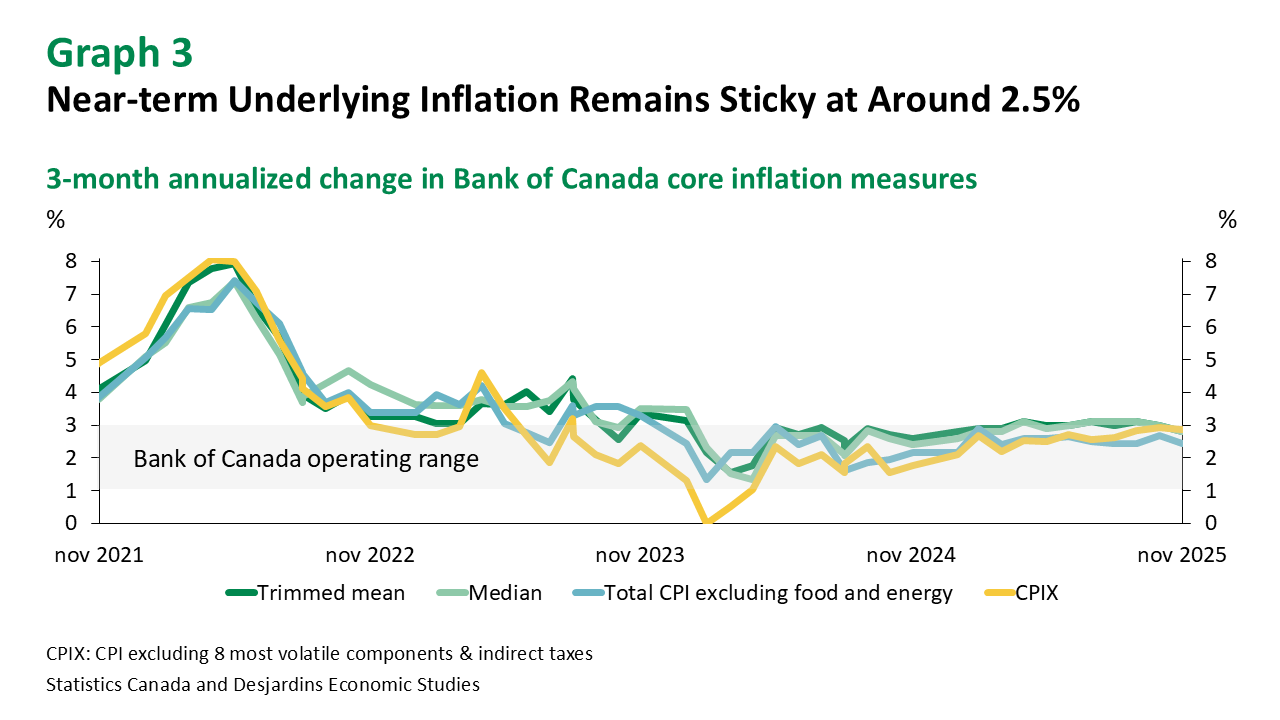

Turning to underlying CPI inflation, the BoC’s preferred measures of core inflation—CPI median and trimmed mean—slowed slightly in November, to around 2.8% y/y. Total CPI inflation excluding food and energy—edged down to 2.4% y/y while total CPI inflation excluding the eight more volatile components barely moved at 2.9% y/y. The average of seasonally adjusted 3-month moving average of these latter series slowed down from 2.8% in October to 2.7% in November (graph 3). Similarly, when this same calculation applied to the Bank’s preferred measures went from 2.6% to 2.3% last month. Looking to other price measures the BoC has favoured lately, there’s no reason to think underlying inflation has strayed much from the Bank’s recent estimate of 2.5%.

Implications

Though headline inflation appears to have normalized, a broad group of underlying inflation measures remain elevated in the 2% to 3% range. And while the economy continues to be in a precarious state, with the upcoming CUSMA review becoming a potentially critical turning point, the BoC is of the view that there is little monetary policy can do to address this uncertainty. As such, the Bank is expected to remain on the sidelines for the foreseeable future External link..