- LJ Valencia

Economist

Economic News

Canada: Uptick in December Inflation as Last Year’s GST/HST Holiday Pushed Up Food Price Growth

January 19, 2026

Highlights

- Headline CPI rose 2.4% y/y in December, slightly above the November pace and the consensus expectation of economists (2.2%). Prices moved down 0.2% month-over-month but rose 0.3% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Comments

While headline inflation surprised by moving higher in December, base effects stemming from the GST/HST holiday a year ago played a big role in pushing up year-over-year prices that month. Services prices accelerated to 3.3% y/y as a result, up from 2.8% in November (graph 1). Under the hood, restaurant prices were the largest driver of CPI growth, rising sharply to 8.5%, far above 3.3% in November. In addition, notable price increases were observed in alcoholic beverages purchased from licensed establishments (6.5%) and from stores (5.6%). Other goods such as toys, games and hobby supplies, and children’s clothing also received an honourable mention in Statistics Canada’s writeup. In contrast, air transportation prices saw a more modest decline (-0.8%) compared to November (-5.9%), likely due to increased holiday travel. Notably, the month-over-month increase in December (34.5%) was larger than prior increases for that month.

In contrast to rising services inflation in December, the cost of goods fell in the month. Gasoline prices fell at a faster pace (-13.8% y/y) relative to November (-7.8% y/y) as crude oil prices fell to their lowest point in over four years. That said, headline inflation would have been about 0.4 percentage points higher in December, at 2.8%, if it weren’t for the elimination of the consumer carbon tax (graph 2). While gasoline prices declined, grocery prices increased again in December (+5.0%), due in part to elevated coffee (30.8%) and frozen beef prices (16.8%).

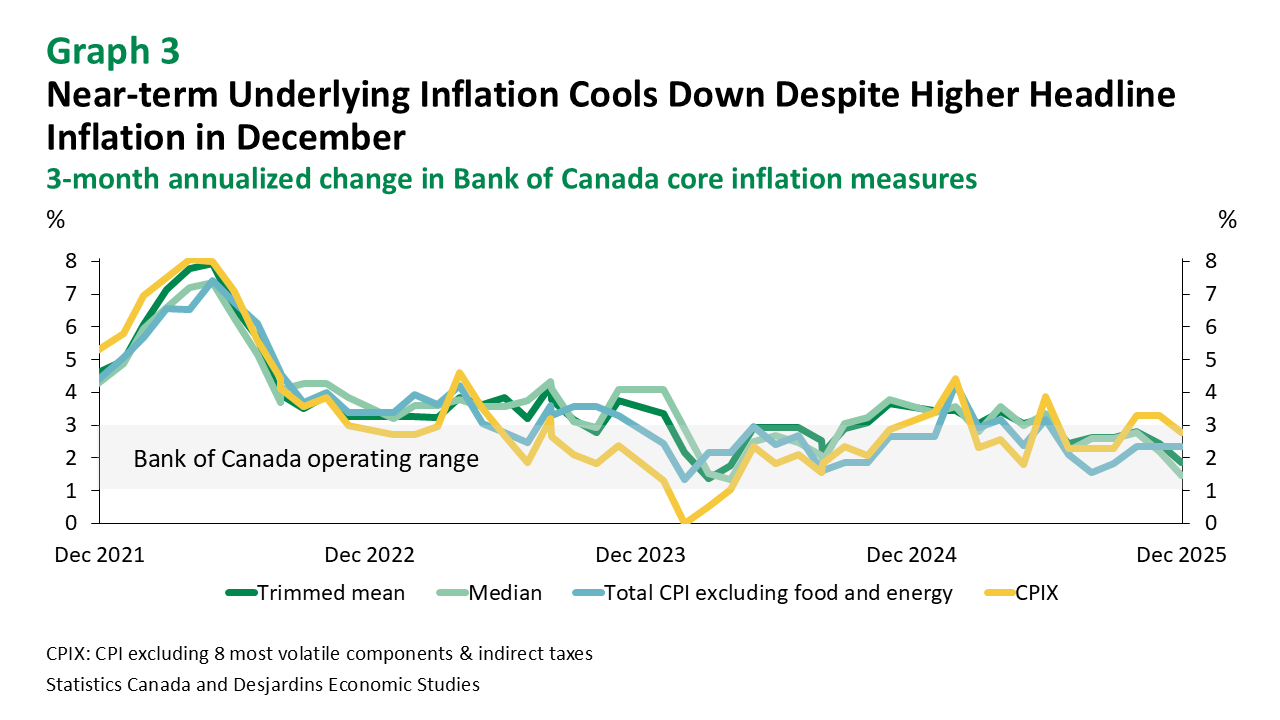

Turning to underlying CPI inflation, the average of BoC’s preferred measures of core inflation—CPI median and trimmed mean—slowed in December to around 2.6% y/y. Total CPI inflation excluding food and energy—shifted up slightly to 2.5% y/y (from 2.4%) while total CPI inflation excluding the eight more volatile components barely moved at 2.8%. Meanwhile, the annualized seasonally adjusted 3‑month moving average of these latter series slowed down from 2.8% in November to 2.6% in December (graph 3). Similarly, this same calculation applied to the Bank’s preferred measures went from 2.3% to 1.7% last month.

Implications

While inflation provided some mixed messages in December, most measures broadly remained in the 2% to 3% range. At the same time, the economy continues to be in a precarious position, with the upcoming CUSMA review becoming a potentially critical turning point. In addition, our analysis External link. on the recent regime shift in Venezuela signals increased uncertainty for oil prices and the Canadian economy. The Bank stated in its previous decision External link. that interest rates are at a level sufficient to guide the economy through this period of trade uncertainty, and the latest CPI data suggests that the Bank is likely to remain on the sidelines.