- Randall Bartlett

Deputy Chief Economist

Economic News

Canada: Lower Inflation in July Reinforces Our Call for a September Rate Cut

August 19, 2025

Highlights

- Headline CPI rose 1.7% y/y in July, down from 1.9% in June and slightly below the consensus expectation of economists (1.8%). Prices moved up 0.3% month-over-month and rose 0.1% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Comments

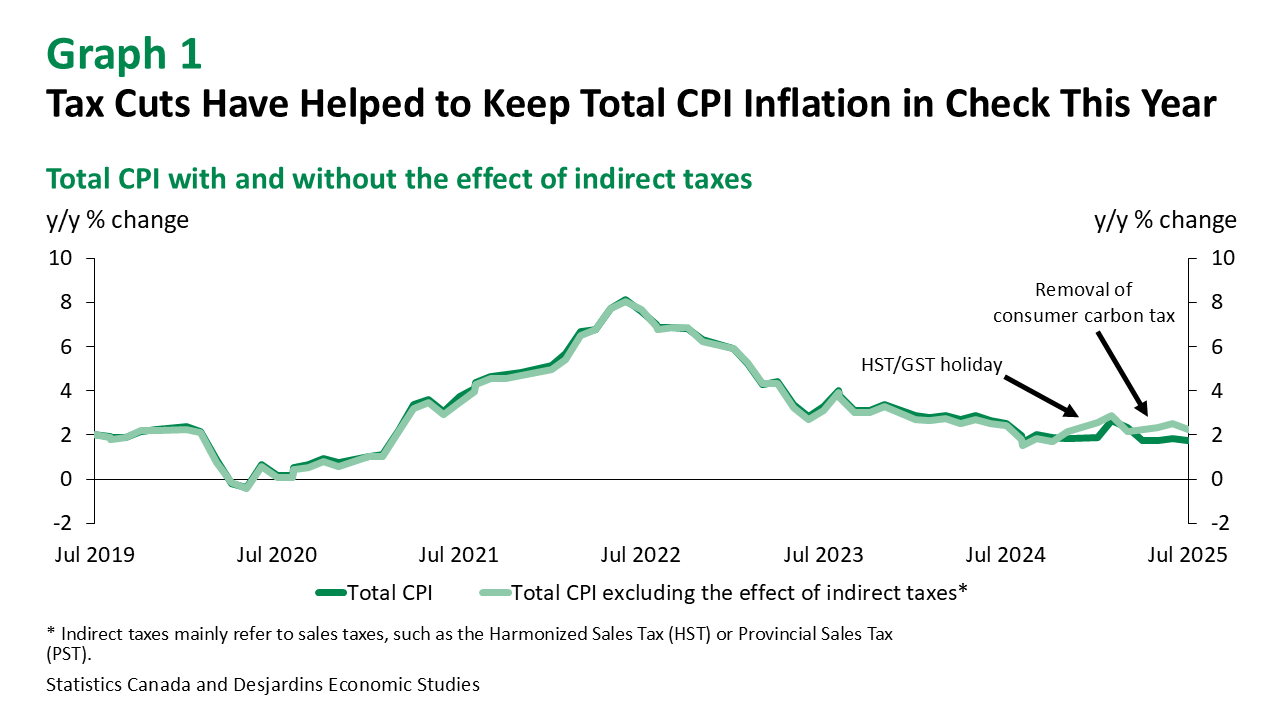

Headline inflation came in below the Bank of Canada’s (BoC) 2% target for the fourth consecutive month in July. This was again in part because of lower energy prices than a year ago thanks to the elimination of the federal consumer carbon tax in April. Without this tax cut, total CPI inflation would have been closer to 2.2% y/y in July, albeit also down from 2.5% in June (graph 1). (See our analysis External link. on the inflationary impact of eliminating the federal price on pollution.) At the same time, gasoline prices fell 0.7% m/m relative to June due to lower crude oil prices on higher OPEC supply and easing tensions between Israel and Iran in the month.

While lower energy prices continued to have a disinflationary impact on price gains in July, changes in other cost categories were more mixed. Grocery prices tacked higher in the month, albeit seemingly due to weather related factors as opposed to policy measures, such as any newly applied import tariffs. And while tariffs continued to play a role in keeping inflation more elevated than it would be otherwise (see our analysis This link will open in a new window.), their contribution to rising core non-shelter inflation may have peaked (graph 2). In contrast, shelter inflation edged up in July as rising rents and utility costs more than offset the sustained slowing in homeownership costs.

What BoC watchers were really keeping an eye out for in July was core CPI inflation. The BoC’s preferred measures of core inflation—CPI median and trimmed mean—edged up slightly in July, averaging 3.1% y/y from 3.0% in June. But the annualized 3‑month moving average of these core seasonally adjusted series slowed sharply to an average of 2.4% from 3.4% in June (graph 3)—an abrupt turn but a welcome one. While just one month of data, this returns near-term underlying inflation to a pace not observed in nearly a year and could signal a slowing in the year-over-year advance in underlying inflation in the months ahead.

Implications

Reading between the lines of the BoC’s most recent interest rate announcement This link will open in a new window., it seemed clear that policymakers would be open to cutting rates to support the weakening economy and labour market if underlying inflation was to start moving in the right direction. With this in mind, the easing of underlying price pressures in the July inflation report may have been just what the doctor ordered. As such, it reinforces our view that the BoC is more likely than not to cut the policy rate at its upcoming meeting in September—an outcome that markets have not yet fully priced in.