- Randall Bartlett

Deputy Chief Economist

Economic News

Canada: October Inflation Supports the BoC Staying on the Sidelines

November 17, 2025

Highlights

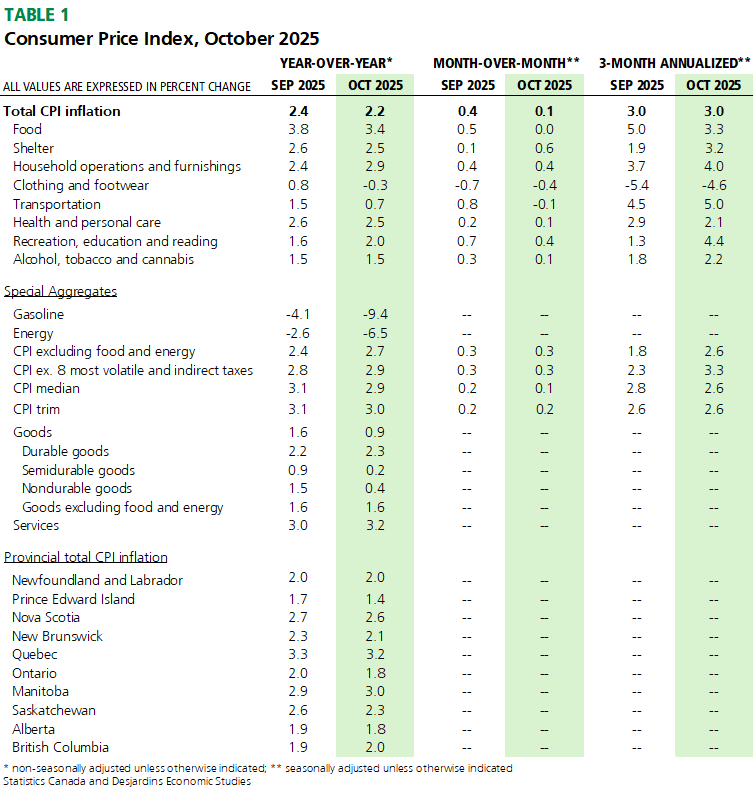

- Headline CPI rose 2.2% in October, down from 2.4% y/y in September and slightly above the consensus expectation of economists (2.1%). Prices moved up 0.2% month-over-month and rose 0.1% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Comments

As expected, headline CPI inflation dropped back toward the Bank of Canada’s (BoC) inflation target in October. Changes in gasoline prices played a big part, down 9.4% y/y from a year ago and 4.8% m/m from September. Lower prices for natural gas in Ontario also contributed to weaker energy prices in the month. That said, headline inflation would have been about 0.6 percentage points higher in October, at 2.8% y/y, if it weren’t the elimination of the federal consumer carbon tax in April (graph 1).

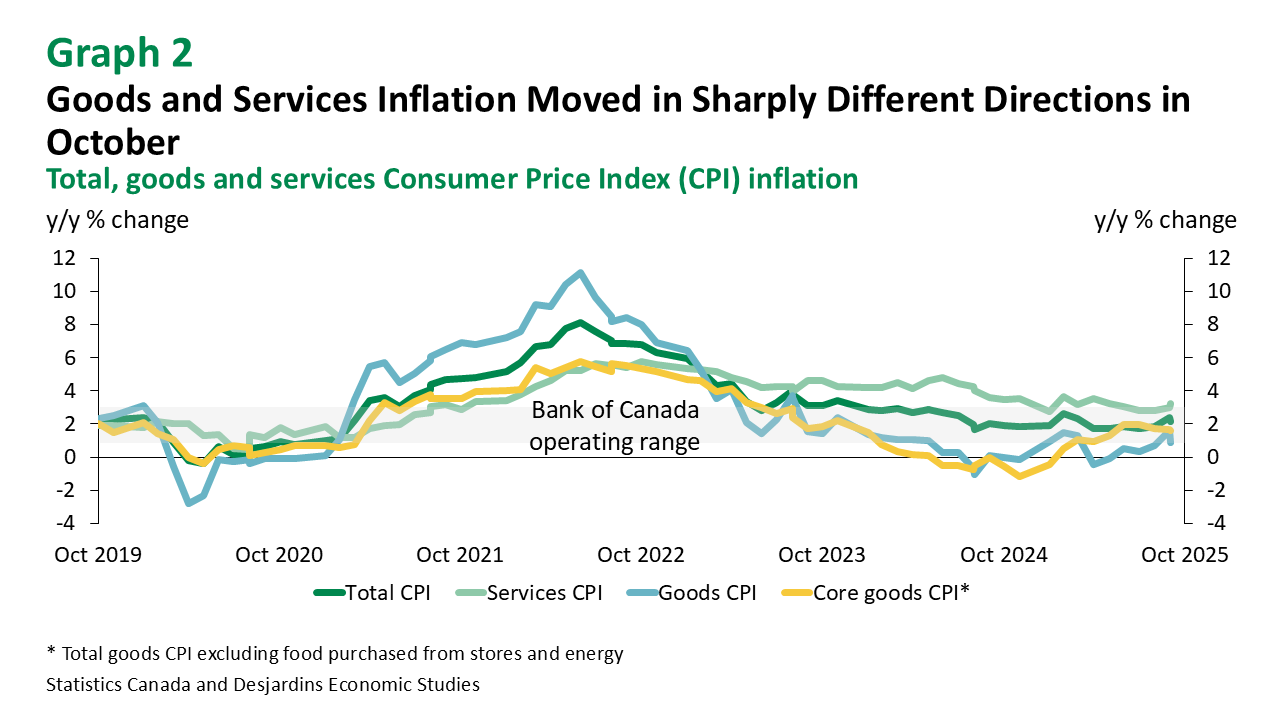

In addition to energy, some other price categories saw notable changes in the month. Helping to pull inflation lower were prices of food purchased from stores, which slowed to 3.4% y/y in October from 4.0% in September. Some of this may reflect the federal government significantly reducing tariffs on imports from the US, which is expected to weigh on inflation going forward as the impact of lower import duties feed through to consumer prices. But it wasn’t all good news in the release. Services inflation grew by couple of ticks to 3.2% y/y (graph 2), due to notable increases in prices for home and auto insurances as well as the first increase in the cost of cellular services since April 2023. Property taxes also rose 5.6% from a year ago, on the back of a 6.0% increase posted in October 2024, while rent inflation posted a notable reacceleration in October (from 4.8% to 5.2%).

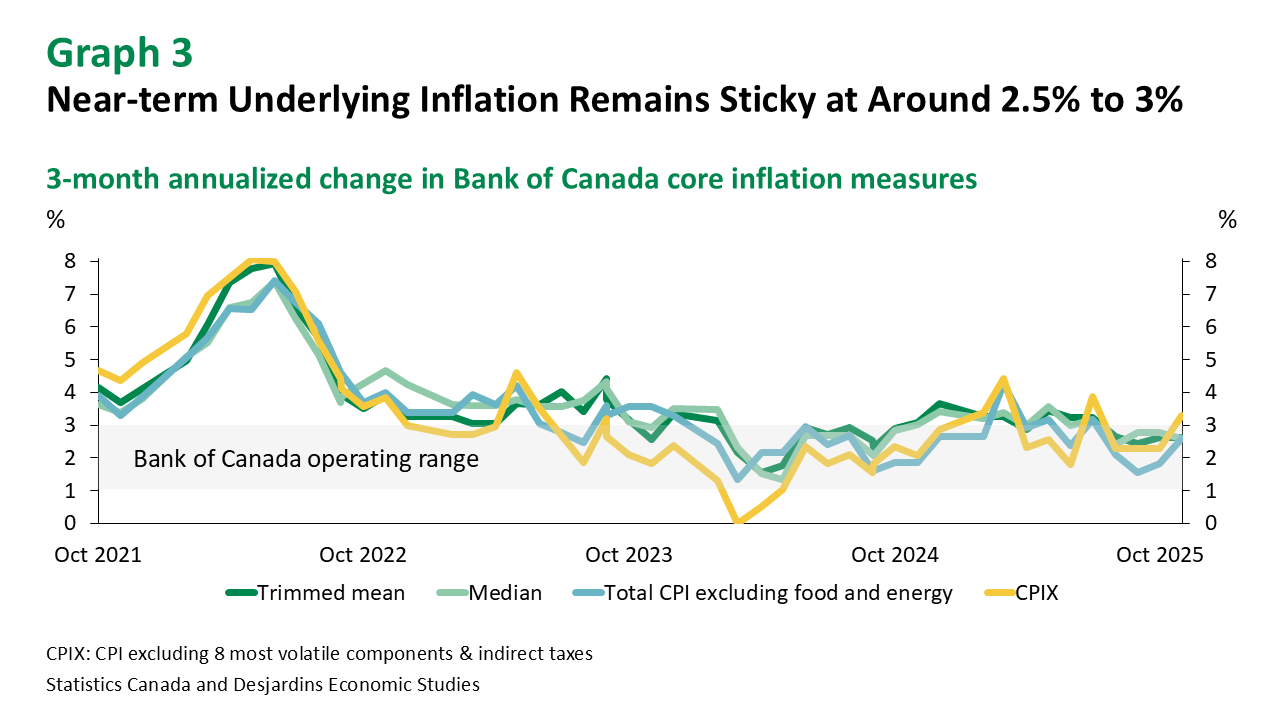

Turning to underlying CPI inflation, the BoC’s preferred measures of core inflation—CPI median and trimmed mean—slowed slightly in October, to around 3.0% y/y. In contrast, more traditional measures of underlying inflation—total CPI inflation excluding food and energy and total CPI inflation excluding the eight more volatile components—moved marginally higher to between 2.7% and 2.9% y/y. More worrying is the seasonally adjusted 3‑month moving average of these latter series, the average of which accelerated markedly from 2.1% in September to 3.0% in October (graph 3). However, this same calculation applied to the Bank’s preferred measures went from 2.7% to 2.6% last month. Looking to other price measures the BoC has favoured lately, there’s no reason to think underlying inflation has strayed much from the Bank’s recent estimate of 2.5%.

Implications

With a broad group of inflation measures remaining in the top half the Bank of Canada’s 1% to 3% operating range and the economy still expected to just escape falling into recession in Q3 2025, there is little pressure on the BoC to continue cutting rates at this time. We maintain our view that the Bank of Canada will be on hold for the next year.