- Randall Bartlett, Deputy Chief Economist • LJ Valencia, Economist

Essentials of Monetary Policy

The Bank Holds the Line as Uncertainty Remains High

January 28, 2026

According to the Bank of Canada (BoC)

- As expected, the Bank of Canada left its policy rate unchanged in January at 2.25%. The overnight rate remains at the lower bound of the Bank’s estimated range for the neutral rate.

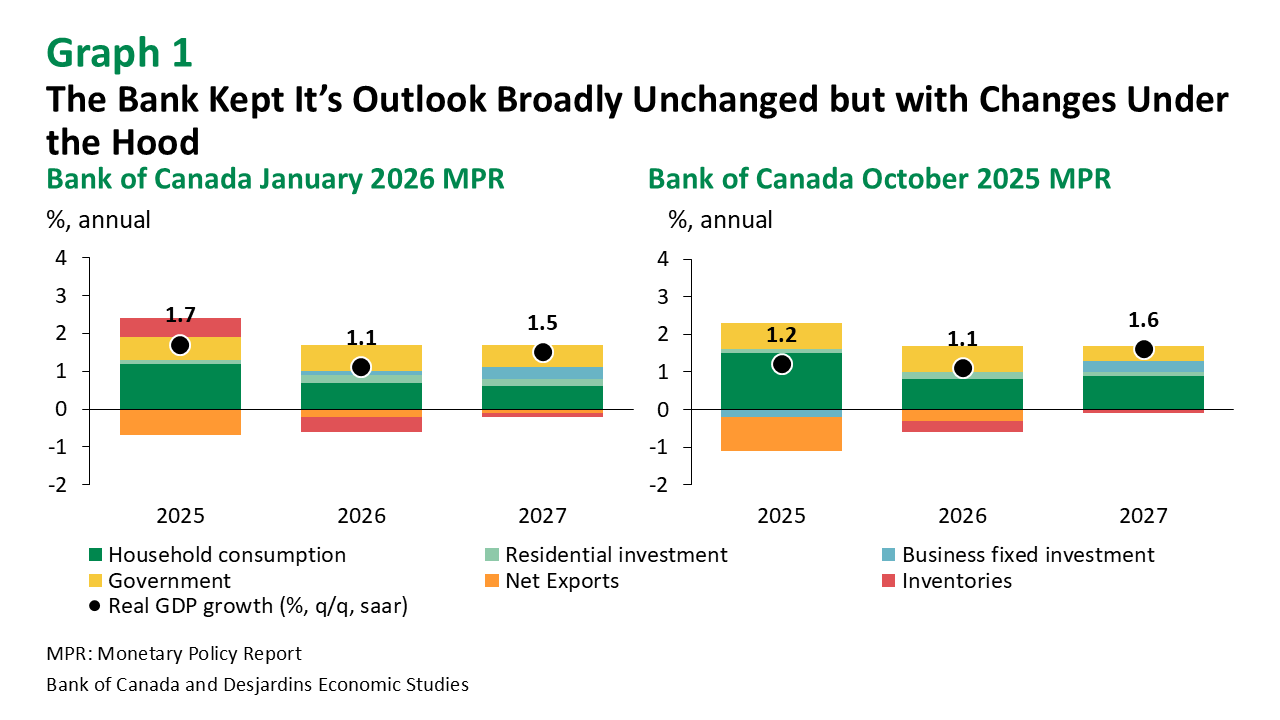

- Overall, the Bank’s outlook for the Canadian and global economies hasn’t changed much since the October 2025 Monetary Policy Report (MPR) External link.. After a strong Q3 2025, Canadian real GDP is expected to stall in Q4 before edging higher early in 2026. Looking further ahead, real GDP is projected to advance by 1.1% this year and 1.5% next year—broadly in line with the Bank’s prior projections (graph 1). And while headline growth remained largely unchanged, stronger government spending and a modest pickup in business investment are expected to be primarily offset by weaker consumption growth.

- In line with the Bank’s growth forecast, the inflation outlook also didn’t change much (graph 2). The central bank expects CPI inflation to remain close to its 2% target, as excess supply offsets trade-related cost pressures. That said, some near-term acceleration in inflation is expected, as the drop in some prices last year due to the short-lived GST/HST holiday External link. gets picked up in the year-over-year numbers. At the same time, the Bank’s preferred measures of underlying inflation eased from 3% in October to 2.5% in December.

- Finally, given the lack of change in the outlook, it came as no surprise that the Governing Council reiterated its view that “the current policy rate remains appropriate, conditional on the economy evolving broadly in line with the outlook we published today.” However, Governing Council highlighted that uncertainty remains high and they are prepared to respond if the outlook changes.

Implications

While economists and markets were fully prepared for the Bank of Canada to hold the line on interest rates today, there were things the Bank avoided spending much time discussing.

The first is the federal Budget 2025 External link., which was scarcely mentioned in the MPR. The upward adjustment to the government category of real GDP was marginal despite sizeable planned deficits. This likely reflects measures skewed more toward investment than consumption. It could also be because the budget has yet to pass in Parliament.

Second, the Bank left the output gap essentially unchanged from the October MPR, at -1.5% to -0.5%. This contrasts with our estimates and those of many others which show a narrower gap after substantial historical revisions to real GDP, implying less slack in the Canadian economy (graph 3).

All told, the Bank looks to have done its best to change as little as possible to support the case for keeping interest rates on hold. And barring any unforeseen changes to the economic outlook, we expect the Bank to remain on the sidelines for the foreseeable future.

2026 Schedule of Central Bank Meetings