- Randall Bartlett, Deputy Chief Economist • LJ Valencia, Economist

Essentials of Monetary Policy

Bank of Canada Leaves Policy Rate Unchanged but Overlooks Some Recent Developments

December 10, 2025

According to the Bank of Canada (BoC)

- As expected, the Bank of Canada left its policy rate unchanged at 2.25% in December. The overnight rate remains at the lower bound of the Bank’s estimated range for the neutral rate.

- In his Press Conference Opening Statement, Bank of Canada Governor Tiff Macklem had several main messages:

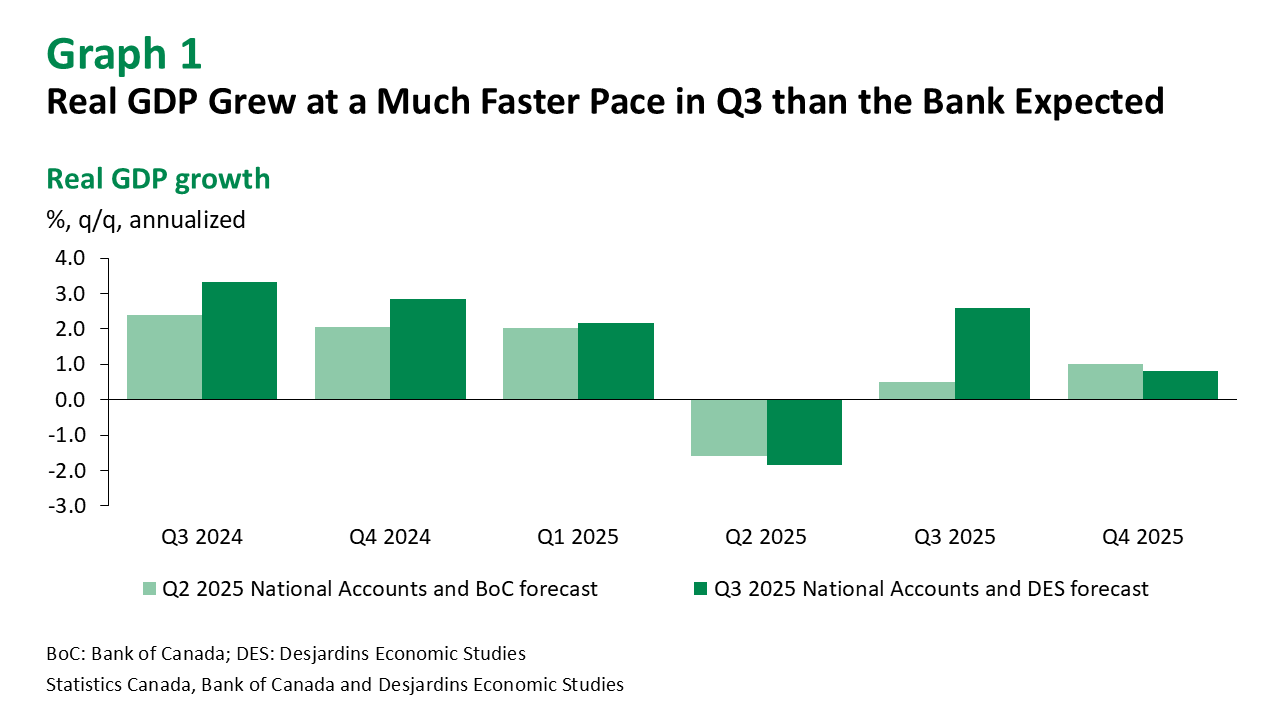

- First, despite high sector-specific tariffs and US trade policy uncertainty weighing on business investment, Canada’s economy is proving resilient, growing by a surprise 2.6% in Q3 2025 External link.. Meanwhile, the unemployment rate fell to 6.5% in November External link., though trade-sensitive sectors continue to be weak and overall hiring remains subdued. The Bank expects Q4 real GDP growth to slow, as trade should be a drag on growth while final domestic demand will probably advance (graph 1). In 2026, the BoC sees growth picking up, although uncertainty persists and high trade volatility may cause sharp quarterly swings.

- Second, despite trade-related cost pressures, inflation continues to be contained. The BoC still views underlying inflation as being around 2.5%. However, total CPI inflation has hovered around 2% for over a year. The Bank expects it to remain around 2% going forward despite some likely higher prints in the next few months reflecting last year’s GST/HST holiday. According to the Bank, ongoing economic slack should roughly offset cost pressures associated with the reconfiguration of trade, keeping CPI inflation close to the 2% target.

- Third, Governing Council reiterated that it “sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment.”

Implications

It was no surprise that the Bank of Canada didn’t feel the need to adjust its overnight policy rate in December. However, what stood out was what the Bank failed to mention in the accompanying documents.

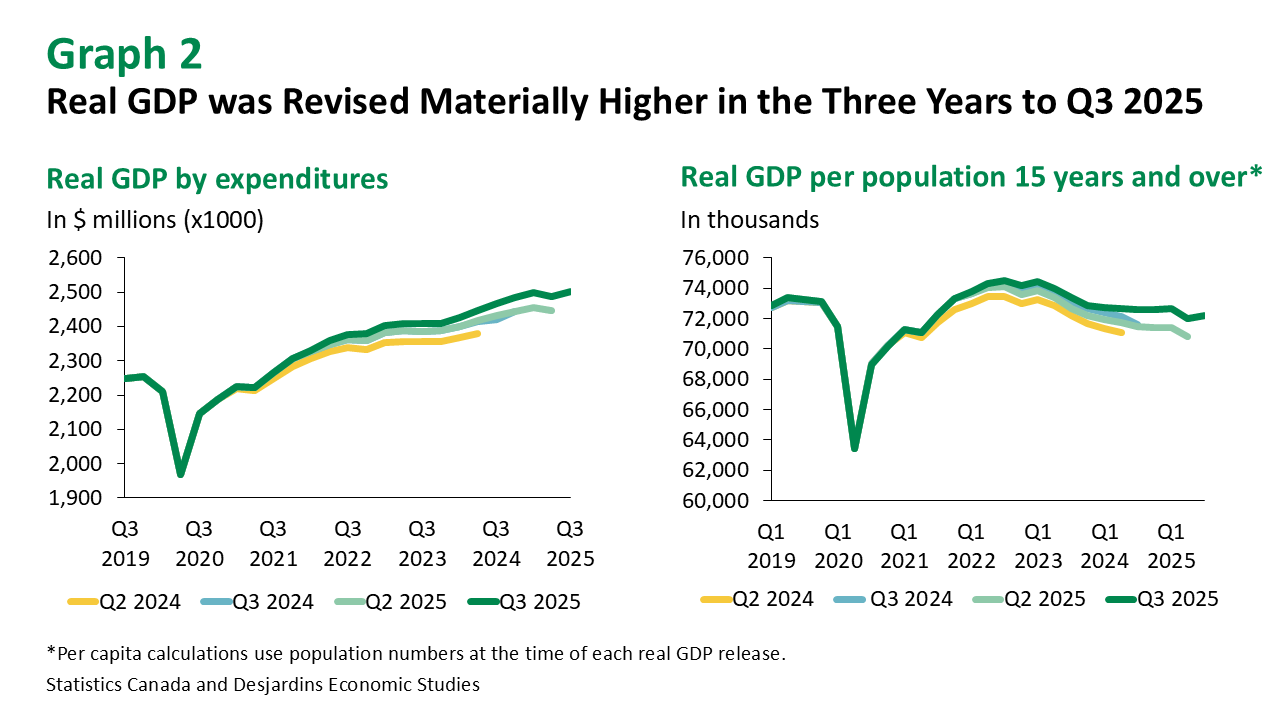

First, real GDP has been revised substantially higher over the three years through to Q3 2025 (graph 2). As such, our output gap estimates were revised, reducing estimated slack and narrowing the output gap relative to that at the time of the October 2025 Monetary Policy Report External link. (graph 3). As a result, there should be less downward pressure to offset trade-related costs. On net, this should provide an inflationary tailwind to the Bank’s already elevated outlook for total CPI inflation.

Second, while Governor Macklem mentioned the recent federal budget External link. in his Opening Statement, its impacts won’t be reflected in the Bank’s economic projections until January. And even then, the Bank expects it to take some time for the measures to be fully realized, gradually supporting both supply and demand.

All told, today’s announcement reinforces our view that the Bank of Canada will likely stay on the sidelines for the foreseeable future. That said, markets have priced in a full hike by the end of next year. We eagerly await the Bank’s updated projections in January.

2025 Schedule of Central Bank Meetings

2026 Schedule of Central Bank Meetings