Contributions to your Registered Retirement Savings Plan (RRSP) made in the first 60 days of the year can be used to reduce your previous year’s taxable income. While popular, this RRSP tax benefit is by no means the only one! Angela Iermieri, a financial planner with Desjardins, presents six ways to take advantage of the sometimes overlooked benefits of RRSPs.

1. Your RRSP contributions may entitle you to certain credits and social programs

Eligibility at both the federal and provincial levels for many tax credits and social programs depends on your situation and net family income. These include the Canada Child Benefit, Family Allowance, tax credit for child-care expenses, and the GST/HST credit.

“Deducting your RRSP contributions reduces your net income, which may make you again eligible for certain credits or social programs or increase the amount of your benefits.”

2. You can contribute to your RRSP now, but defer the tax deduction

You may have experienced a temporary drop in income as a result of being unemployed for a few months or by going on parental leave. If you still have some cash and unused RRSP contribution room, you can contribute to your RRSP this year to generate an immediate tax-sheltered return without necessarily reducing your taxable income right away.

“If you expect your marginal tax rate to be higher next year, deferring the tax deduction will generate greater tax savings.”

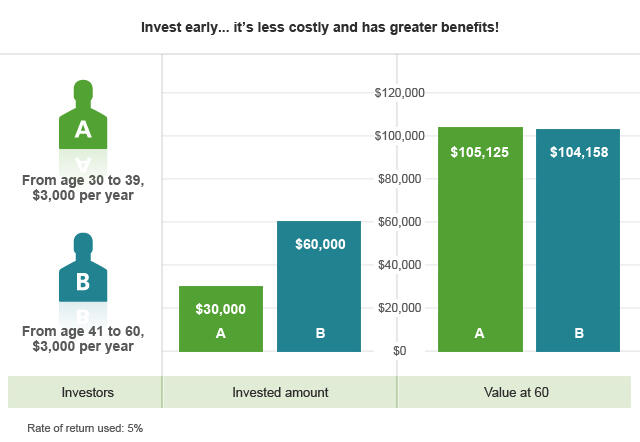

3. RRSPs speed up the effect of compound interest

The earlier you contribute, the longer your investments will benefit from a compounding effect. Over time and with investment diversification in keeping with your profile, your RRSPs could generate a return where the gains can be reinvested: this is the effect of the compound return. This will enable your savings and returns to grow tax-free as long as they remain in the RRSP. This speeds up the “return on the return.”

“Since the returns generated on the investments in your RRSP portfolio are tax-sheltered, all of the money can be reinvested and the total amount could accumulate even faster.”

Time is on your side! For example, with similar returns, an investor who contributes $3,000 per year from age 30 to 39 (or $30,000 over 10 years) will normally accumulate a higher amount than another investor who contributes the same amount each year from age 41 to 60 (or $60,000 over 20 years).

4. You can invest the tax savings from your RRSP contributions

When you file your tax returns, deducting your RRSP contributions will give you tax savings, which may result in a tax refund. In such a case, consider using this extra money to help you achieve your financial goals.

“By using your tax refund to contribute to your children’s Registered Education Savings Plan (RESP), you increase the amount and take advantage of government grants. If you have enough contribution room, you can also use your tax refund to top up your Tax-Free Savings Account (TFSA) or get a head start on next year’s RRSP contributions!”

5. Your RRSP can be used to finance your return to school

If you or your spouse return to school full-time, the The Lifelong Learning Plan (LLP) enables you to use your RRSP to finance your studies, under certain conditions. You will then have up to 10 years to repay the amount withdrawn from your RRSP.

“Each person can withdraw up to $20,000 over up to four consecutive years, but not more than $10,000 in a single year. A couple can withdraw up to $40,000 to jointly finance the return to school of one of the spouses.”

6. Use your RRSP to start over if you separate

The Home Buyers’ Plan (HBP) is not just for first-time home buyers or for persons who have not owned a home for four years prior to the purchase. With the HBP, your RRSP could also be used in the event of a separation, for instance.

“Under certain conditions, a person who is divorced or ending their conjugal relationship may withdraw up to $60,000 from their RRSP to buy back their share of the home from their former spouse or purchase a new home.”

See Complete list of HBP requirements the Government of Canada’s website.

An RRSP can be a financial tool for preparing for retirement and financing certain life plans starting today. Don’t hesitate to talk to your advisor if you need help.