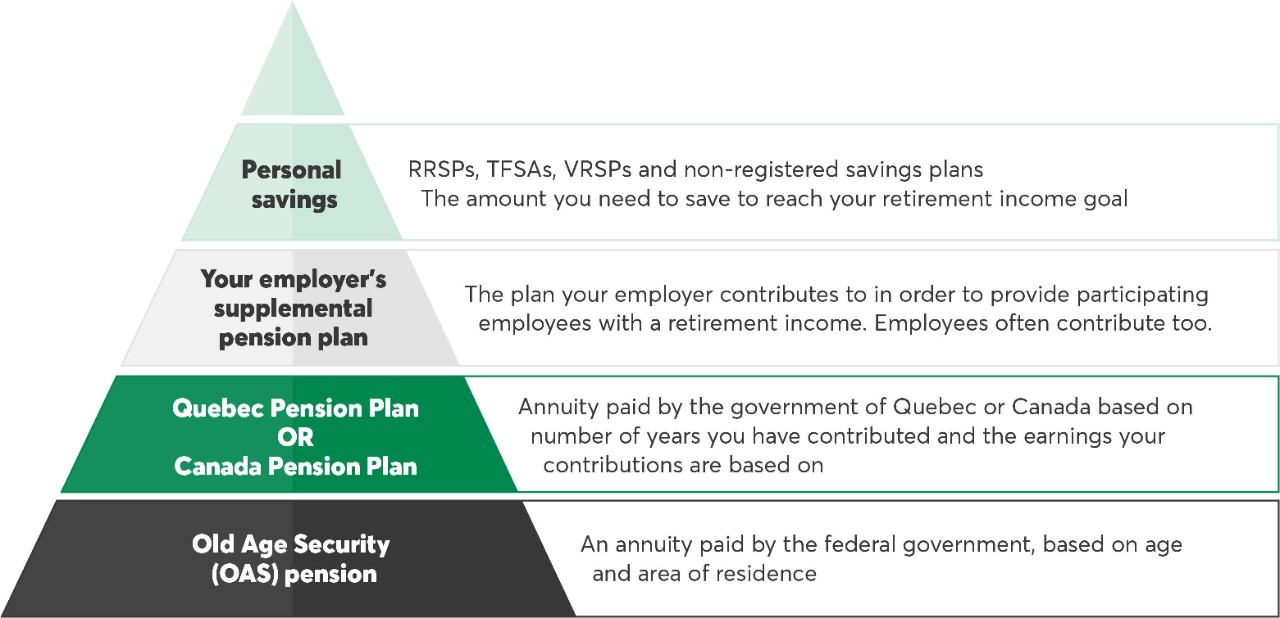

Where will your income come from when you retire?

Are you thinking about retirement and wondering where your income will come from when you leave the job market? To give you a better sense of what's available, here's an overview of the 4 most common sources of income in retirement.1

1- Old age security pension

You can start collecting this pension every month after you turn 65, even if you're still working.

A pension for everyone

The old age security pension (OAS) is paid out by the Government of Canada. This taxable benefit is reviewed every 3 months to ensure that it reflects increases in the cost of living as measured by the Consumer Price Index (CPI).

OAS benefits can be postponed until age 70. Waiting will give you higher payments, but it's something you need to consider carefully, taking into account your health, financial situation and other sources of income.

To be eligible for OAS, you must:

Be at least 65 years old.

Be a citizen or legal resident of Canada.

Have lived in Canada for at least 10 years since you turned 18. If you currently live outside Canada, you must have resided in Canada for at least 20 years since turning 18.

You can request OAS benefits even if you have never worked.

What resources exist for people with a low income?

If you have a modest income and live in Canada, you can apply for the Guaranteed Income Supplement (GIS). The amount you receive depends on your annual income and your family situation. The supplement, which is adjusted to the cost of living every 3 months, is not taxable.

If you are between the ages of 60 and 64, you can also receive the supplement if your spouse receives OAS benefits and is eligible for the GIS. If your spouse dies, you may be eligible for the Allowance for the Survivor benefit.

To learn more about pension plans and benefits, visit the website of the Government of Canada.

2- Canada Pension Plan or Québec Pension Plan benefits

Québec Pension Plan benefits

All workers in Quebec automatically contribute to this plan. The benefit you receive will depend on the number of years you contributed to the QPP and how much you earned during those years.

When should you start collecting QPP benefits?

It's up to you to review the available options for starting QPP benefits and decide what timing is best for you.

Did you know that you can start collecting benefits at age 60, even if you're still working? But the amount you receive depends on your age when you apply.

Between 60 and 65: Your pension will generally be reduced by 0.6% each month from the date you apply until you turn 65.

At age 65: Your pension will neither be reduced nor increased because age 65 is considered the "normal" retirement age.

After age 65: Your pension will increase by 0.7% each month from your 65th birthday until you apply, up to age 72.

How does the Québec Pension Plan work?

Workers and their employers split QPP contributions equally, but anyone who is self-employed has to pay the entire amount. If a self-employed worker declares a low income and therefore only makes a small contribution, this will impact how much they get in retirement, as their QPP benefits will be determined accordingly.

The QPP is indexed to the cost of living every January and is taxable. Very few people receive the maximum amount.

To determine what's best for you, take a look at your QPP statement.

To learn more about the QPP, visit the website of the Government of Quebec.

Canada Pension Plan benefits

Except for Quebec residents, all workers in Canada automatically contribute to this plan. The benefit you receive will depend on the number of years you contributed to the CPP and how much you earned during those years.

When should you start collecting CPP benefits?

It's up to you to review your options for starting CPP benefits and decide what timing is best for you.

Did you know that you can start collecting benefits at age 60, even if you're still working? But the amount you receive depends on your age when you apply.

Between 60 and 65: Your pension will generally be reduced by 0.6% each month from the date you apply until you turn 65.

At age 65: Your pension will neither be reduced nor increased because age 65 is considered the "normal" retirement age.

After age 65: Your pension will increase by 0.7% each month from your 65th birthday until you apply, up to age 70.

How does the Canada Pension Plan work?

Workers and their employers split CPP contributions equally, but anyone who is self-employed has to pay the entire amount. If a self-employed worker declares a low income and therefore only makes a small contribution, this will impact how much they get in retirement, as their CPP benefits will be determined accordingly.

The CPP is indexed to the cost of living every January and is taxable. Very few people receive the maximum amount.

To determine what's best for you, take a look at your CPP statement.

To learn more about the CPP, visit the website of the Government of Canada.

3- Supplemental pension plan

Workers who are part of a private pension plan save throughout their career—practically without realizing it.

What is it?

The terms "private pension plan," "registered pension plan" and "pension fund" all refer to the same thing: a supplemental pension plan (SPP).

It’s the plan your employer contributes to in order to provide participating employees with a retirement income. The benefits you accumulate are usually "locked-in" until you retire. This means you can't access the money before then, subject to the plan's terms and conditions. Your contributions are deducted from your income, and the income you receive once you retire will be taxable.

What type of plan do you have?

There are 2 main types of plans:

Defined benefit plan: With this type of plan, the amount is determined in advance and is generally a percentage of your salary multiplied by the number of years of service recognized by the plan. Contributions are regularly re-evaluated to fund the benefits that have been promised to plan members. While most plans include provisions for benefits to be indexed, full indexation is rare.

Defined contribution plan: This type of plan sets the employee and employer contributions in advance, but the amount of the pension is not known ahead of time. The amount you'll receive depends on your contributions, your employer’s contributions and the pension fund's investment performance. Rather than being based on your salary, the pension amount is based on how much you have saved in your accounts, the value of your investments at the time you decide to withdraw them, and the withdrawal approach you choose.

To estimate your future retirement income, review the statement of benefits provided by your employer each year.

4- Personal savings

Investing your savings in an RRSP or TFSA can be an effective way to supplement public pensions and your pension fund, if you have one. By using these vehicles to build a nest egg, you can prepare for the retirement of your dreams.

How much should you save for retirement?

To determine how much you need to save to maintain your standard of living, you need to consider things like inflation, what kind of retirement you want, when you plan to stop working and how long your retirement will be. Don't forget that life expectancy is increasing!

Aim to save 10% of your net income. As your goals become clearer, you can adjust the amount you save. Keep track of your budget so you can pinpoint any unnecessary expenses that could help grow your nest egg over time.

Saving requires discipline, but it's also about being consistent. Get into the habit of setting money aside as soon as you get your paycheque. To make it even easier, you can set up automatic payments to your RRSP or TFSA. Just make sure you check how much contribution room you have.

How do you grow your investments?

It all depends on your situation. Your advisor can help you determine your investor profile and choose suitable investments.

The 2 main registered investments are the registered retirement savings plan (RRSP) and the tax-free savings account (TFSA). Both of these tools can help you grow your savings for the future.

By contributing to an RRSP, you accumulate tax-sheltered savings for retirement while reducing your taxable income. Remember that any withdrawals you make are taxable. An RRSP is a good idea if you think your tax rate will be lower when you retire than it currently is.

When you turn 71, you'll need to convert your RRSP into a registered retirement income fund (RRIF) or an annuity. Your savings will continue to grow, but you’ll no longer be able to contribute to your RRSP, and you’ll have to withdraw some of the money you’ve accumulated each year.

Note that you can contribute to your spouse’s RRSP before the end of the year in which they turn 71, as long as you still have contribution room.

When you contribute to a TFSA, your earnings are tax-sheltered, regardless of whether you use them for retirement or another needs.

If you expect your retirement income to be modest, a TFSA is a good option for you. Unlike RRSP withdrawals, withdrawals from a TFSA aren't taxable. This means they won't jeopardize your access to income-based tax credits and social programs when you retire.

The future may be unpredictable, but you can still plan for it!

Talk to an advisor about your retirement goals. They’ll help you see the big picture. You’ll work together to determine the best way to approach this new stage of life and build the right retirement plan for you.

1. This information is provided for information purposes only and may be subject to legislative changes. Full details are available on the official government websites.