Understanding your credit card statement

You just got your credit card statement. Whether it's your first statement or your 90th, the amount of information it contains can be overwhelming. But don't worry! In this helpful guide, we'll go into detail about how to read the basic information you'll find in your monthly statement..

Before we start, make sure to have your credit card statement handy.

It'll help you follow along so you can remember where to look for things later.

Here are your statement's main sections:

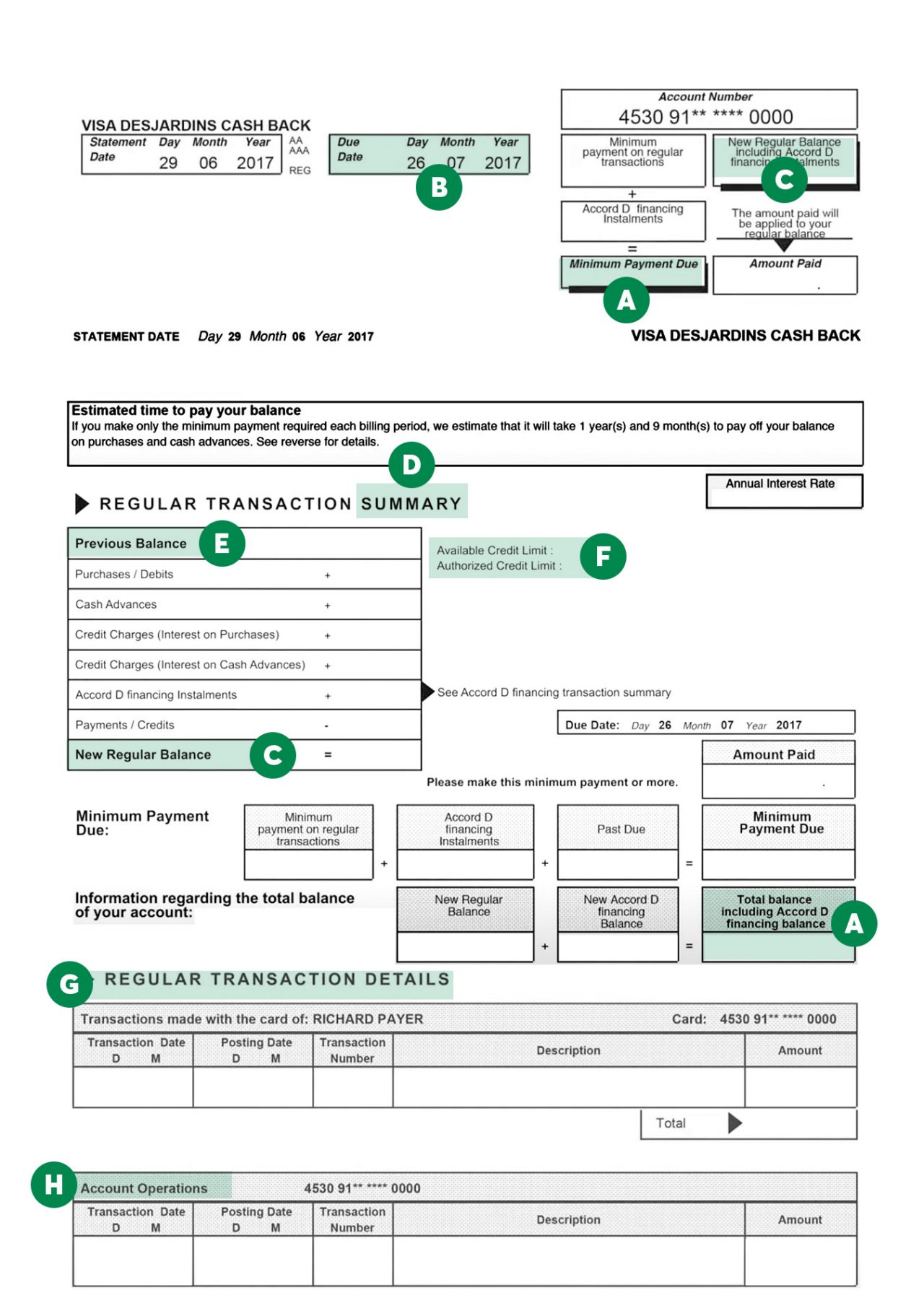

A) Minimum Payment Due

This is the minimum amount you need to pay before the payment due date to ensure your payment is considered on time. If you forget to make this payment or if it's received late, it will show up on your credit report. Since your minimum payment due is just a fraction of your current balance (usually 5%), you should always try to pay more to avoid taking on too much debt.

B) Statement Date and Payment Due Date

Your statement date tells you when the document was issued. Your payment due date is the date by which your payment needs to be received.

C) New Regular Balance

This is the total of all transactions posted to your account since your last statement. It includes any monthly payments on installment plans and Accord D financing, as well as cash advances and remaining balances from previous months (if applicable). You can avoid paying interest if you pay your balance in full by your payment due date. If you don't pay your balance in full before the payment due date, interest charges will be added to your balance.

D) Regular Transaction Summary

This table let's you see your account transactions at a glance. They're organized by category, including purchases, debits, cash advances, monthly installment payments, Accord D financing installments, interest on purchases and cash advances, as well as any payments made. Your new regular balance is based on the sum total of these transactions.

E) Previous Balance

This is the amount that was due as of your last credit card statement.

F) Authorized Credit Limit and Available Credit

Your available credit tells you the maximum value of any new transactions you can make. It's your authorized credit limit minus your current balance. Your authorized credit limit is the maximum amount you can borrow using all of the cards on your account as of your statement date.

Paying your credit card statement in full every month is the best way to maintain a good credit score. Among other things, having good credit will play in your favour if you ever want to take out a mortgage or a car loan.

G) Regular Transaction Details

This section contains details about the transactions posted to your account. If your account has multiple cardholders, these transactions will be organized by card. If your card features cash back or BONUSDOLLARS®1, you'll also see the percentage earned for each transaction depending on the purchase category.

H) Account Transactions

This section shows you a breakdown of payments made and charges incurred since your last statement, along with the transaction date.

You should make it a habit to check your credit card statement and transactions. It will help you:

- Get a clear idea of what you spent that month to help you stick to your budget

- Identify any fraudulent transactions

- Make sure any charges or refunds to your account are accurate so you can identify potential merchant errors

I) BONUSDOLLARS® or cash back earned since your last statement

If your credit card comes with BONUSDOLLARS® or cash back rewards, this section will let you know how much you earned this month.

The transactions posted to your credit card account during the current billing cycle will appear on your next statement. After the statement is issued, you'll be given a grace period (usually 21 days) to pay your current balance—preferably in full.

Annual interest rate

This rate is applied to your total balance once the payment due date has passed, and to all cash advances as of the transaction date.

Your credit card's annual interest rate is probably higher than your other loans (like your student loan, car loan or mortgage). If you're trying to figure out which debts to pay off first, it's usually a good idea to start with those with higher interest rates.

Regular purchases

If you always pay your balance in full by the due date, you won't have to pay any interest on your regular purchases. If you only make a partial payment, the annual interest rate will be applied to your total balance and interest charges will be added to your next statement.

Making more than the minimum payment due will limit your interest charges and prevent you from incurring more debt.

Cash advances

You can also use your credit card to get a cash advance from an ATM or via AccèsD. But watch out—in addition to any ATM withdrawal fees you incur, interest on cash advances starts immediately and is added daily. There's no grace period for cash advances, so you should always try to pay them back as soon as possible.

Cash advances may be an easy way to borrow money, but they can get expensive if you don't pay them back quickly. It's better to think of them as a temporary, short-term solution.

AccèsD makes managing your credit card easy

To make sure you never miss a payment, you can sign up for pre-authorized payments on AccèsD when you log in using a web browser. You'll be asked to select a payment option (in other words, whether you'd like to pay your balance in part or in full) and the amount will be directly withdrawn from your everyday account every month. That way, you don't have to worry about forgetting to pay your bill.

You can also choose to get a notification whenever your minimum monthly payment hasn't been received a few days before your payment due date. Another easy way to help you manage your money!

Lost, stolen or damaged card?

You can swiftly lock or replace a lost, stolen or damaged card whenever you need to by selecting Manage card on AccèsD.

More useful features

- Want to change your credit limit? You can request an increase or decrease in the Manage card section of AccèsD.

- Want to limit how much you can spend and get a notification when your available credit dips below a certain amount? Activate the Credit limit approaching alert and choose when you'd like to be notified by entering an amount.

- Have questions about your credit card's features? Check out the Features and benefits section under the Information tab for your credit card.

Want to learn more? Check out our walkthrough of your credit card statement.

The features and benefits of each credit card can vary a lot. Find out which one is right for your needs and lifestyle!

1 BONUSDOLLARS® is a registered trademark of the Fédération des caisses Desjardins du Québec.