- Francis Généreux

Principal Economist

Essentials of Monetary Policy

Federal Reserve: Still Not Ready to Give a Clear Signal on Rate Cuts

March 20, 2024

According to the Federal Reserve (Fed)

- The Committee decided to maintain the target for the federal funds rate in a range of 5.25% to 5.50%.

- Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated.

- The Committee judges that the risks to achieving its employment and inflation goals are moving into better balance.

- In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2%.

Comments

The policy statement published by the Federal Open Market Committee wasn’t much of a surprise. In fact, it wasn’t very different from the January statement (aside from removing a reference to slower job creation). The decision to hold rates was no surprise either. Recent statements by Fed officials, including Jerome Powell’s testimony before Congress, had already made that clear, and the consensus on this was unanimous.

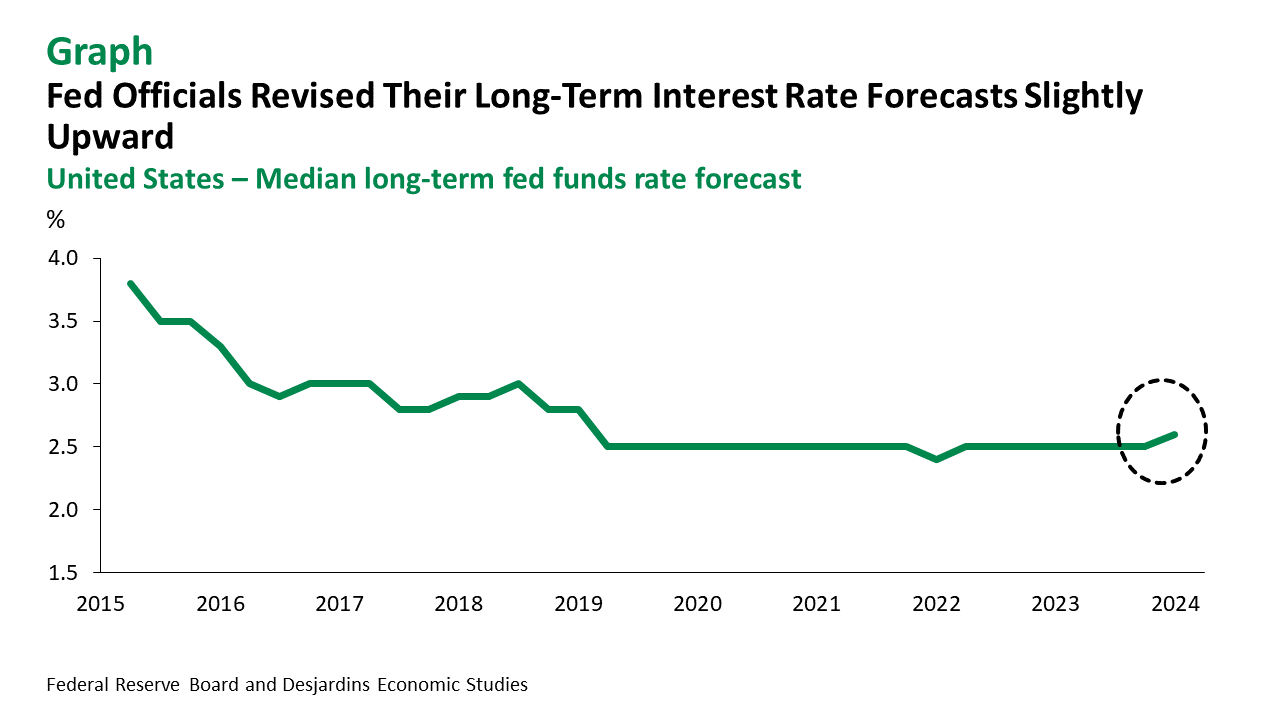

Updated forecasts by Fed officials shed a little more light on future decisions. As was the case last December, the median forecast is still for three 25‑point rate cuts by the end of this year. That said, if just one official changes their mind, it could bring the median down to just two. As for 2025, the median forecast is now for three cuts, down from four in December. It’s worth pointing out that the median for the medium-term rate, often called the nominal neutral rate, rose from 2.5% to 2.6%. It had been sitting at 2.5% since March 2019 (and was 2.8% in December 2018). In addition, the number of Fed officials who see the neutral rate at or above 3% jumped from 4 to 7. It seems that the Fed is starting to think that the “normal” rate could move higher over this cycle. Although this kind of change is unusual, it also isn’t that surprising. A number of factors point to a higher equilibrium rate: the US economy’s resilience in the face of tighter monetary policy, inflation that could be less sensitive to various downward pressures than it has been over the past two decades, higher levels of government debt and the ever-expanding need for public and private investment.

The Fed’s updated forecasts also revised the figure for real GDP growth at the end of 2024 upward from 1.4% to 2.1%. That’s higher than our own forecasts. The projections for real GDP growth in 2025 and 2026, as well as for unemployment and inflation, haven’t changed much.

Given the US economy’s continuing and expected strength, and the fact that the median forecast sees headline and core inflation staying slightly above the Fed’s 2% target, why should we expect the Fed to start cutting rates? During the press conference, Jerome Powell said he remains confident that “inflation [is] moving down gradually on a sometimes bumpy road toward 2%”. Since key rates are well above the neutral rate (even now that it’s been revised upwards), there’s still room for cuts.

Implications

Unsurprisingly, the Fed decided to hold steady on rates once more. Although inflation remains stubbornly high and its downward trajectory slowed in early 2024, the Fed seems confident that it will converge toward the target for the long term. Fed officials still expect three rate cuts this year. And if more progress is made in bringing inflation under control over the coming months, a June rate cut could still be on the table.

2024 Schedule of Central Bank Meetings