- Randall Bartlett

Senior Director of Canadian Economics

Economic News

Canada: The Canadian Economy Ended 2023 with a Skip in Its Step

January 31, 2024

Highlights

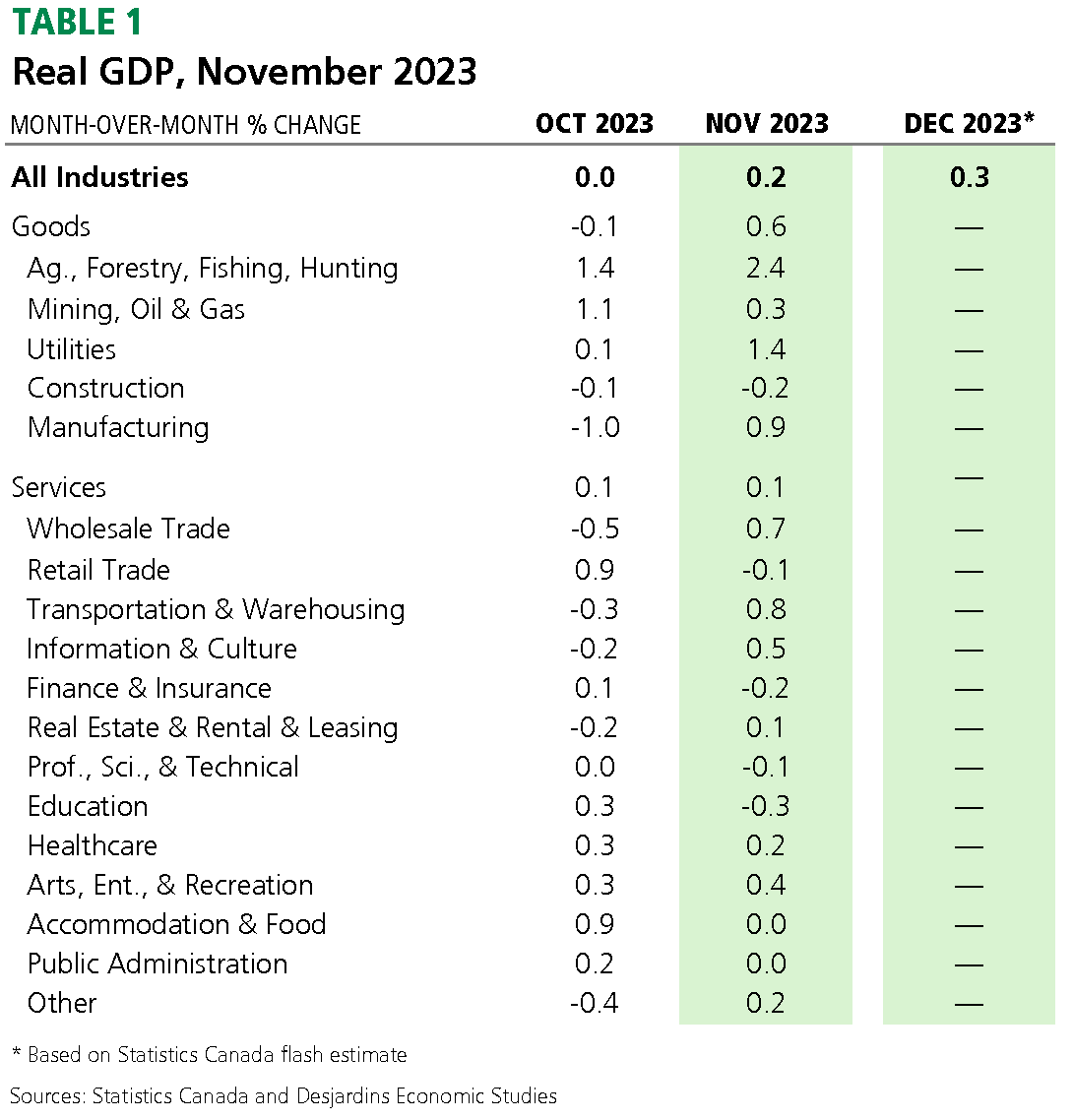

- Real GDP moved 0.2% higher in November, beating the consensus expectation of economists and Statistics Canada’s flash estimate (both +0.1%). Goods-producing sectors jumped 0.6%—the strongest growth since January 2023—while output in services-producing sectors edged up a more modest 0.1%. In all, 13 of 20 subsectors posted gains. See Table 1 for further details.

Implications

There was a lot of good news to report in the November real GDP release. The relatively broad-based gains were led by an outstanding performance in goods-producing sectors, with agriculture, utilities and manufacturing all shedding their recent weakness. Statistics Canada’s forward-looking information suggests some of these sectors showed further strengthen in December. Construction, however, may not be so lucky. Services were more of a mixed bag, with weak sectors in October rebounding in November and vice versa. That said, weakness in the education sector due to the strike in Quebec should be relatively short lived.

Looking ahead, Statistics Canada’s flash estimate for December is pointing to 0.3% growth in real GDP by industry. That would be the strongest pace of monthly GDP growth since May of last year (graph 1). Assuming it is correct, real GDP by industry would advance by 1.2% annualized in Q4 2023. Meanwhile, we’re tracking growth in real GDP by expenditure closer to 1.0% in the fourth quarter, well above the Bank of Canada’s recent forecast of 0.0% published in its January 2024 Monetary Policy Report. But we’ve seen massively outsized revisions to monthly real GDP in the past two quarters, so one would be wise not to assume that this data won’t be substantially revised a month from now. Indeed, we think the risks to our current tracking are to the downside.

For the Bank of Canada, this data gives them the opportunity to keep rates unchanged for now. Renewed economic strength in the final quarter of 2023 and a strong handoff to the start of 2024 could mean sustained economic strength and higher-than-hoped-for inflation this year. However, we anticipate more economic weakness on the horizon, as ongoing mortgage renewals at higher rates and slowing population growth weigh on the Canadian economy.