- Randall Bartlett

Senior Director of Canadian Economics

Economic News

Canada: Inflation Agrees to be the BoC’s Valentine in February

March 19, 2024

Highlights

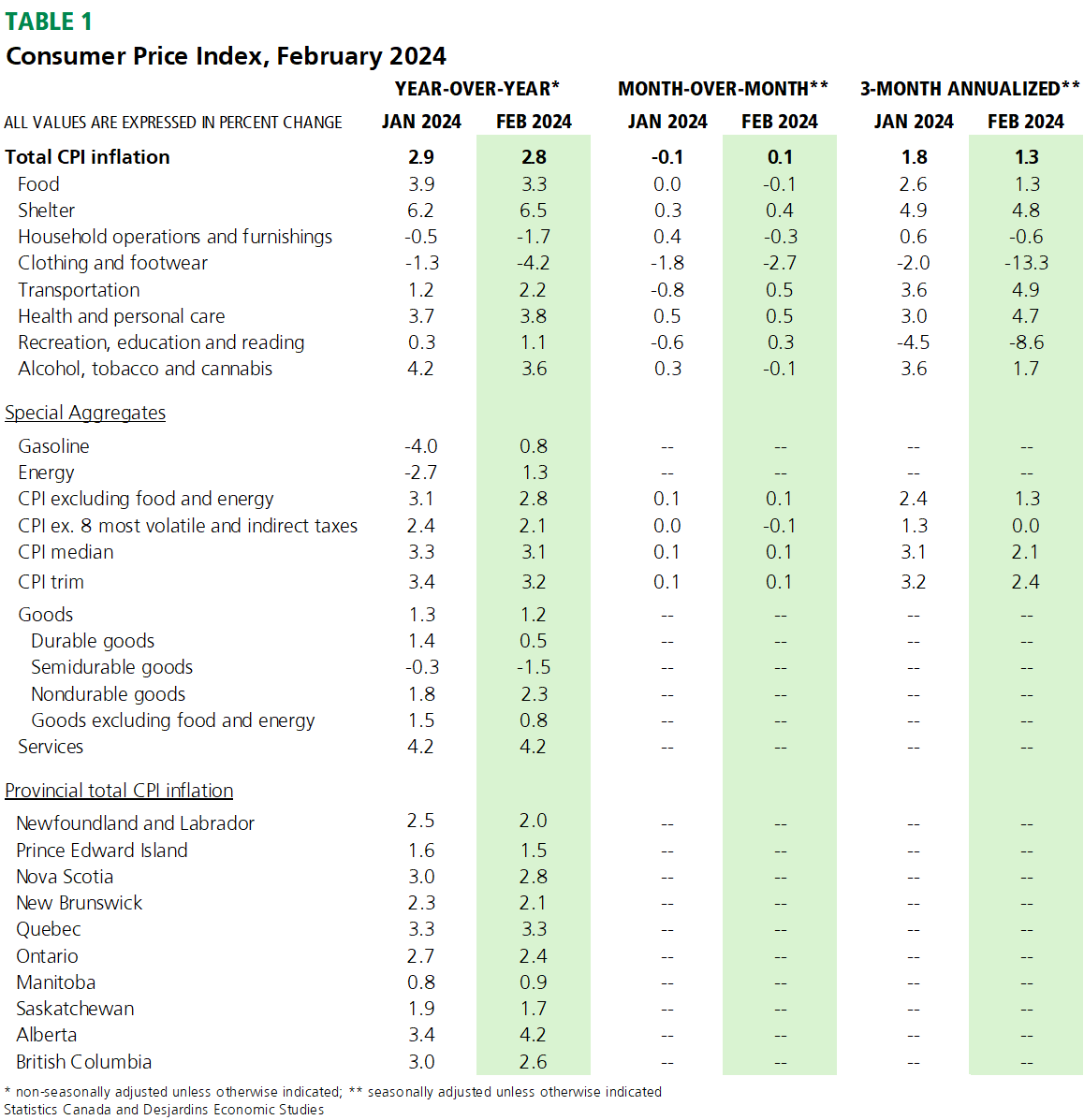

- Headline CPI rose 2.8% y/y over February of last year, coming in well below the consensus forecast of economists (3.1%) for the second consecutive month. Meanwhile, monthly prices rose 0.1% m/m on a seasonally-adjusted basis, reversing January’s drop. Table 1 summarizes the key data points.

Implications

2024 just keeps coming up Canada on the inflation front, with February posting the second consecutive downside surprise. At 2.8% y/y, inflation seems to be settling comfortably into the Bank of Canada’s 1% to 3% target range for inflation.

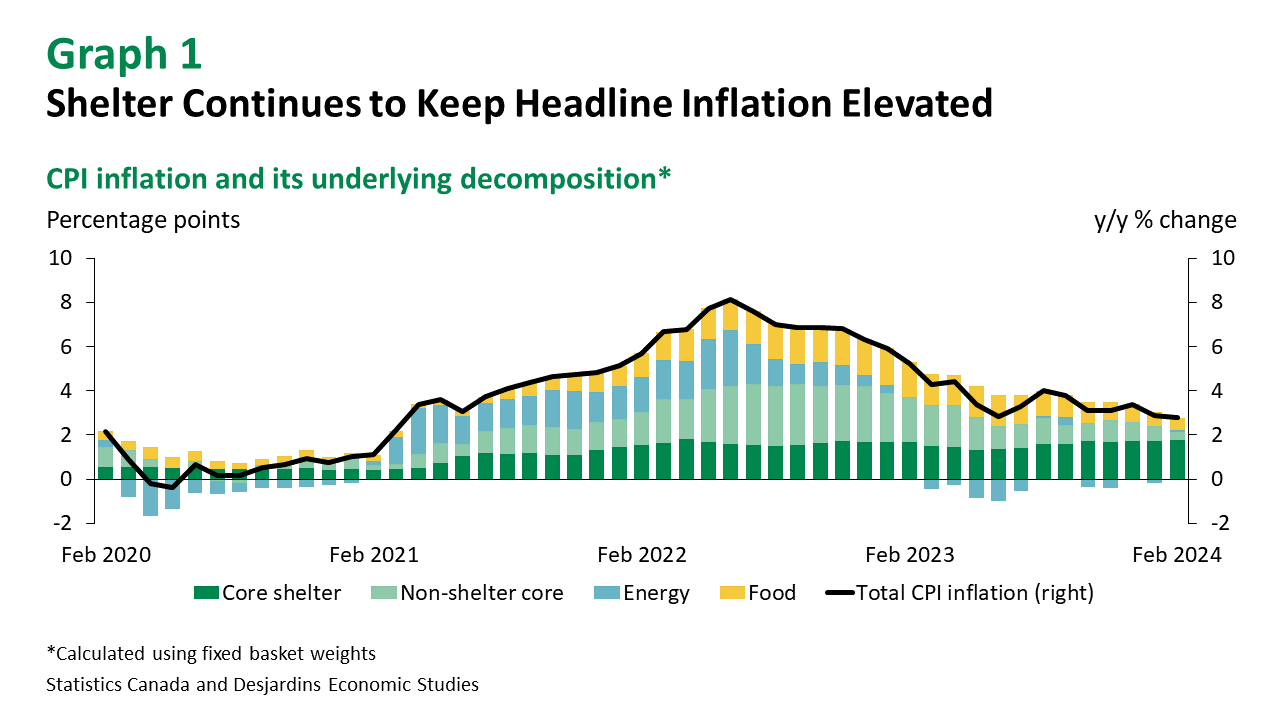

Unpacking the headline move, there was a lot to like in the February release. Food price growth (2.4%) continued to ease. And while posting a positive print on a year-over-year basis, the contribution from gasoline to February inflation was modest. As a result, the rise in total CPI excluding food and energy broadly matched the 2.8% increase in headline. Canadians also continued to pay less for cellular (-26.4%) and childcare (-2.8%) services in the month. However, it wasn’t all good news. Shelter prices accelerated on a year-over-year basis in February (graph 1), boosted by both rented (7.9%) and owned (6.9%) accommodation, the latter still largely being driven by mortgage interest cost (26.3%).

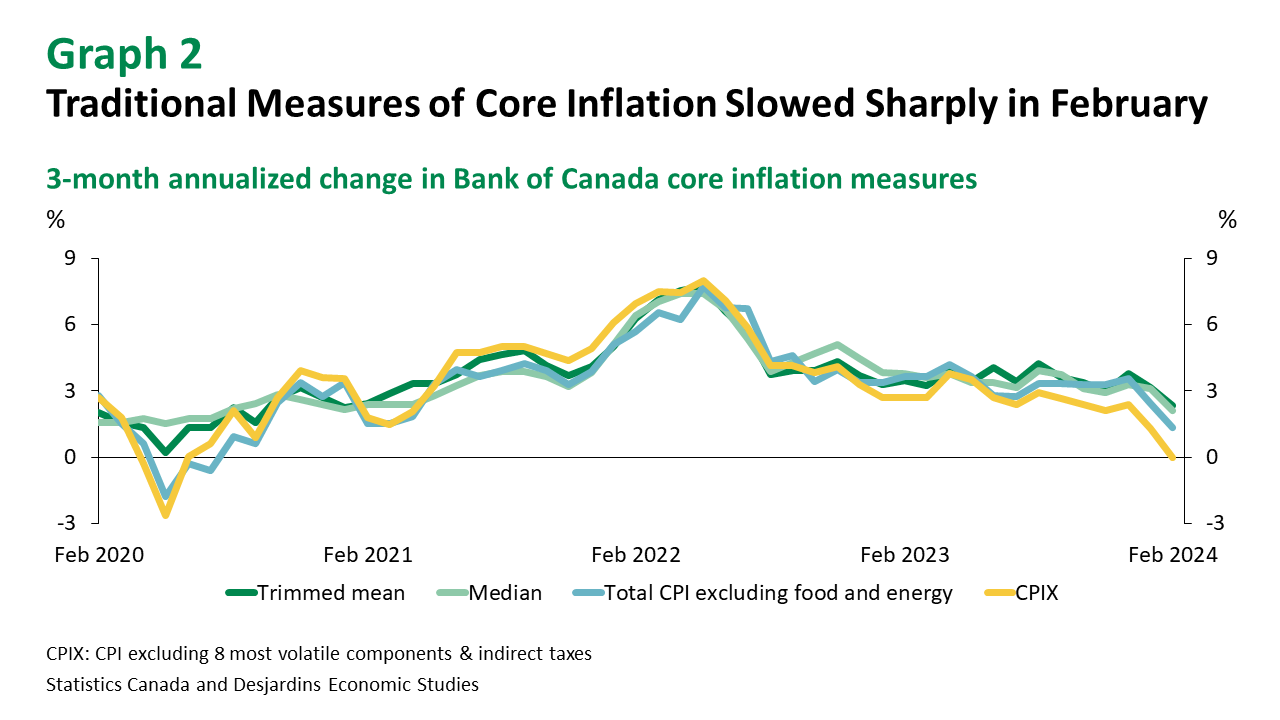

Digging deeper into the data, the Bank of Canada’s preferred measures of core inflation—CPI median and trimmed mean—decelerated again in February but remained above 3%. But on a 3-month annualized basis, these measures slowed on average by 0.9 percentage points to reach 2.1% and 2.4%, respectively (graph 2). However, as recent research External link. from our Macro Strategy team found, “the problem is that those measures have become biased, likely overestimating the true underlying inflation rate.” Instead looking to the more universally referenced total CPI inflation excluding food and energy, inflation on a 3-month annualized basis slowed sharply to 1.3% in February. And in a blast from the past, CPIX (CPI excluding the 8 most volatile components & indirect taxes)—the Bank’s former preferred measure of core inflation—was flat when calculated the same way, for the second consecutive month under 2%.

At 2.8% y/y, headline inflation in the first two months of 2024 is coming in well below the Bank’s forecast of 3.2% for Q1 in the January 2024 Monetary Policy Report. Along with weakness in the Bank’s consumer and business surveys and recent spike in business insolvencies, February’s inflation print helps to reinforce the case for rate cuts to begin in June 2024. The Bank will likely signal a change in policy at its upcoming April meeting.