- Francis Généreux

Principal Economist

Economic News

US Job Market Stays on Hot Streak in February

March 8, 2024

Highlights

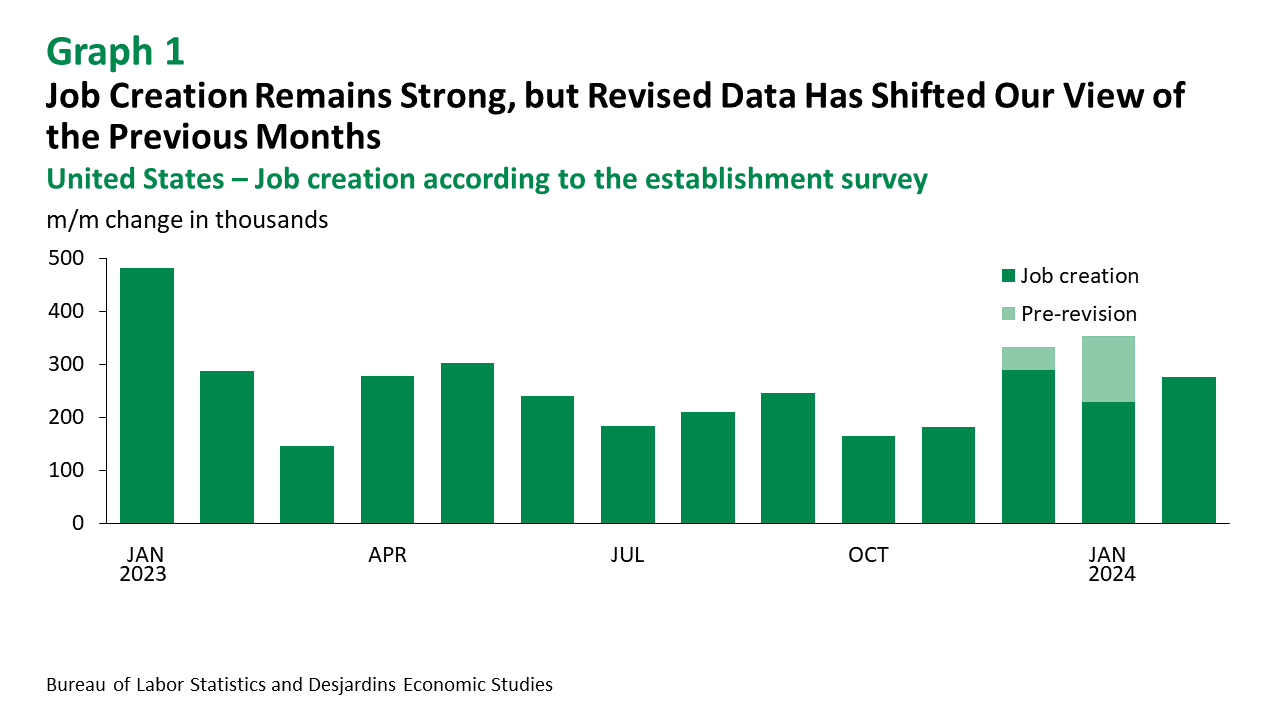

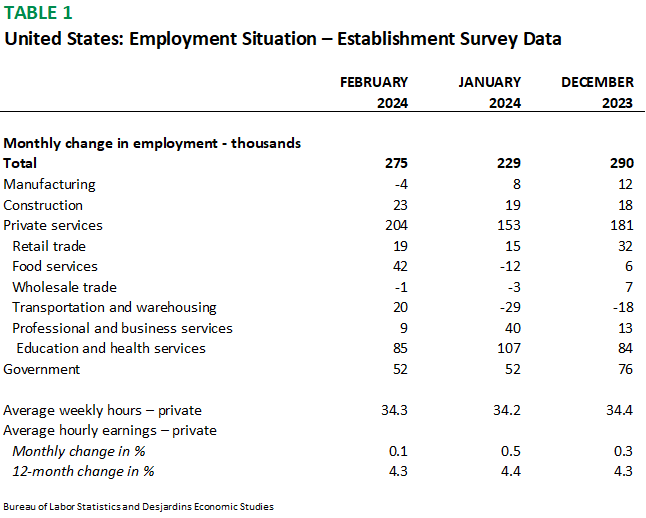

- According to the establishment survey, the US added 275,000 jobs in February.

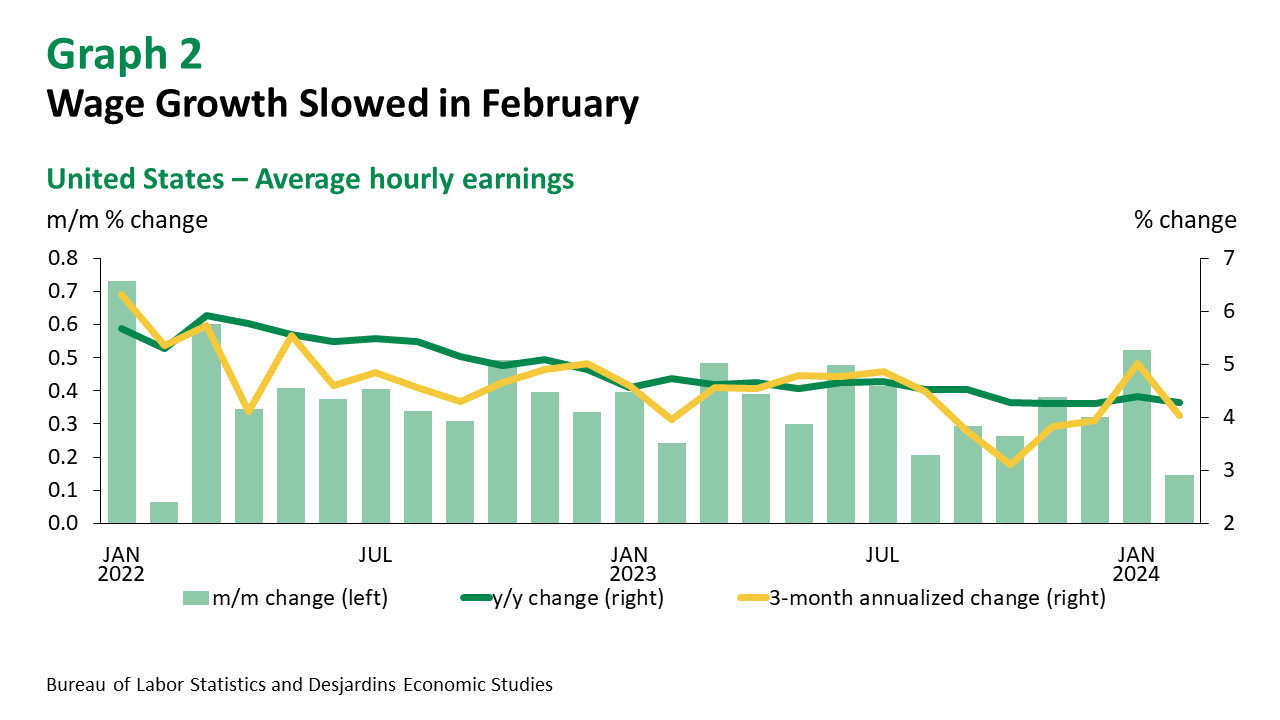

- After accelerating in January, average hourly wage growth slowed in February.

- Unemployment rose from 3.7% to 3.9%.

Comments

The monthly US jobs report is out and it's starting to look like Groundhog Day. Once again, the establishment survey showed more jobs were added than expected. The Bloomberg consensus had forecast 200,000 new jobs. Once again, the resilience of the US economy and the strength of its job market delivered an upside surprise. That said, the sunny picture painted by the February print was somewhat clouded by downward revisions of the preceding months' data. The 353,000 jobs first announced for January were downgraded to "only" 229,000, while December gains went down from 333,000 to 290,000. That said, the revised numbers are still very strong and remain above the consensus forecast prior to their initial release.

In addition, some of the negative impacts of the January cold snap (after a warm December) faded in February. Weekly hours worked lost ground in January, but edged up from 34.2 to 34.3 hours in February. Changes to the employment mix in January had resulted in strong average hourly wage growth of 0.5%. In February, this figure fell to 0.1%, the smallest gain in 2 years.

The percent of industries where employment increased also rose from January (61.8%) to February (62.6%). Job creation picked up in several sectors, including retail, food services, and transportation and warehousing. For the first time since October 2023, manufacturing saw net layoffs, even though these losses were low (-4,000) and mostly in chemical manufacturing (-2,100). Other soft spots included 15,400 jobs lost in temporary help services. This continues a 23-month-long slide for the sector, which is down 433,000 jobs since its peak two years ago.

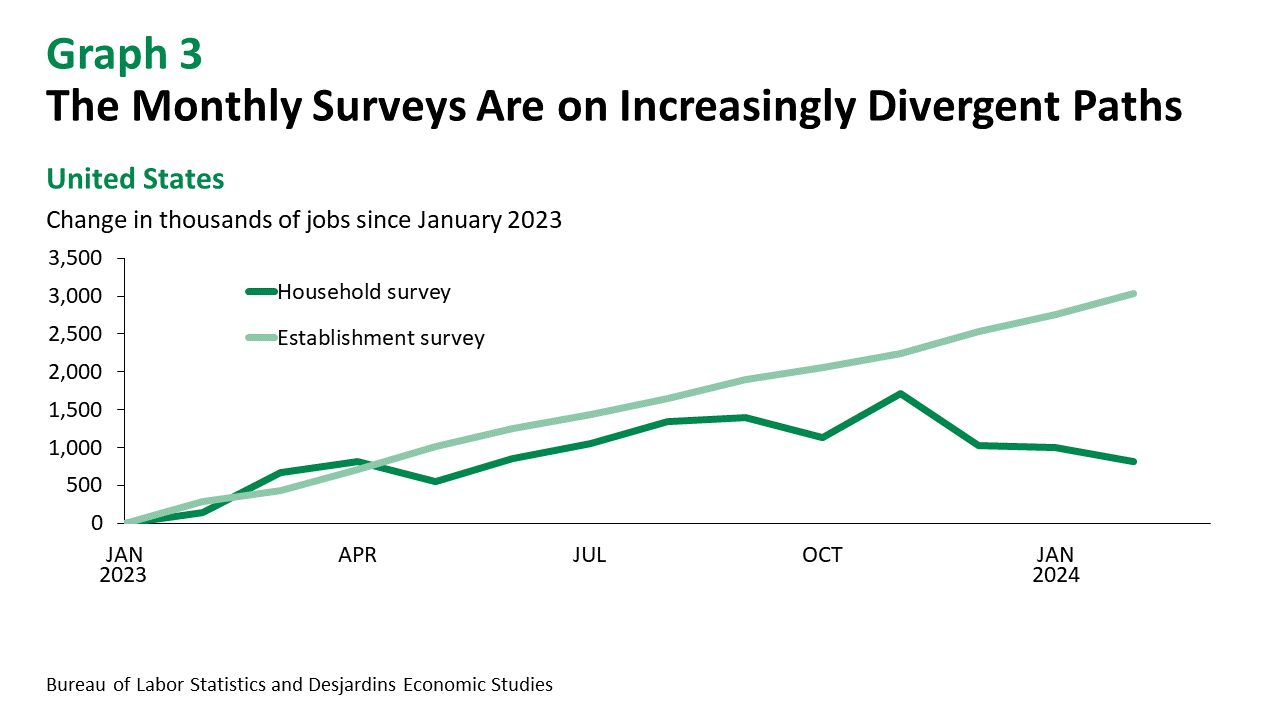

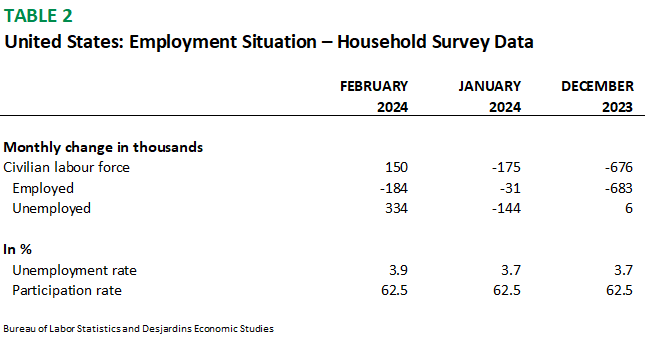

Once again, the data for the establishment and household surveys told contrasting stories. The household survey showed a decrease of 184,000 jobs in February. This represents the third consecutive month of declines, for a total loss of 898,000 jobs since the November high. At the same time, the establishment survey shows 794,000 new jobs. We need to keep in mind that the household survey is much less reliable and shows more volatility month-on-month. But the fact remains that the household survey's underperformance is driving up the unemployment rate, which climbed from a low of 3.4% in April 2023 to 3.9% in February. This is the highest it's been since January 2022.

Implications

The US job market is still running hot, at least according to the establishment survey. The downgrades to the December and January figures and the rising unemployment rate revealed by the household survey nevertheless suggest the market is cooling. If wage growth and inflation continue to slow in the coming months, the Fed may finally be able to start cutting rates in late spring.