- Francis Généreux

Principal Economist

Weekly Commentary

Will the Presidential Election Influence the Fed's Decisions?

April 26, 2024

It looks like the wind has shifted for the Fed. Just a few weeks ago, it seemed like the Fed was signalling that rate cuts were on the horizon. But since then the resilience of the US economy appears to have changed the central bank's plans. If economic indicators had come in as expected, the Fed's next meeting, ending on Wednesday, May 1, could have been used to lay the groundwork for an initial rate cut in June. But since they haven't, it's now quite possible that Fed Chair Jerome Powell will signal that the US central bank will wait and see before it starts cutting rates. He and the other Fed officials want to see clear signs that inflation is starting to fall back down to the 2% target. But so far this year, sticky inflation (including the resurgence of some inflation components), a strong labour market and robust first-quarter domestic final demand growth haven't exactly built a convincing case for a rate cut in the very near future.

We therefore expect the Fed to hold off on monetary easing. Of course, that would depend on the inflation trajectory and the likelihood of it converging toward the target. But could decisions on key rates also be influenced by the presidential election?

Officially, the Fed will always claim that politics don't affect its monetary policy decisions. Jerome Powell recently reiterated External link. that "We do not consider politics in our decisions. We never do. And we never will. And I think the record—fortunately, the historical record really backs that up."

It's clear that, if economic and financial conditions so require, the Fed won't have any qualms about making the choices needed to fulfill its mandate from Congress, which is to promote maximum employment and stable prices. Just before the 2008 election, with the global financial crisis in full swing, the Fed forged ahead with interest rate cuts and an array of ambitious measures to protect the US banking sector.

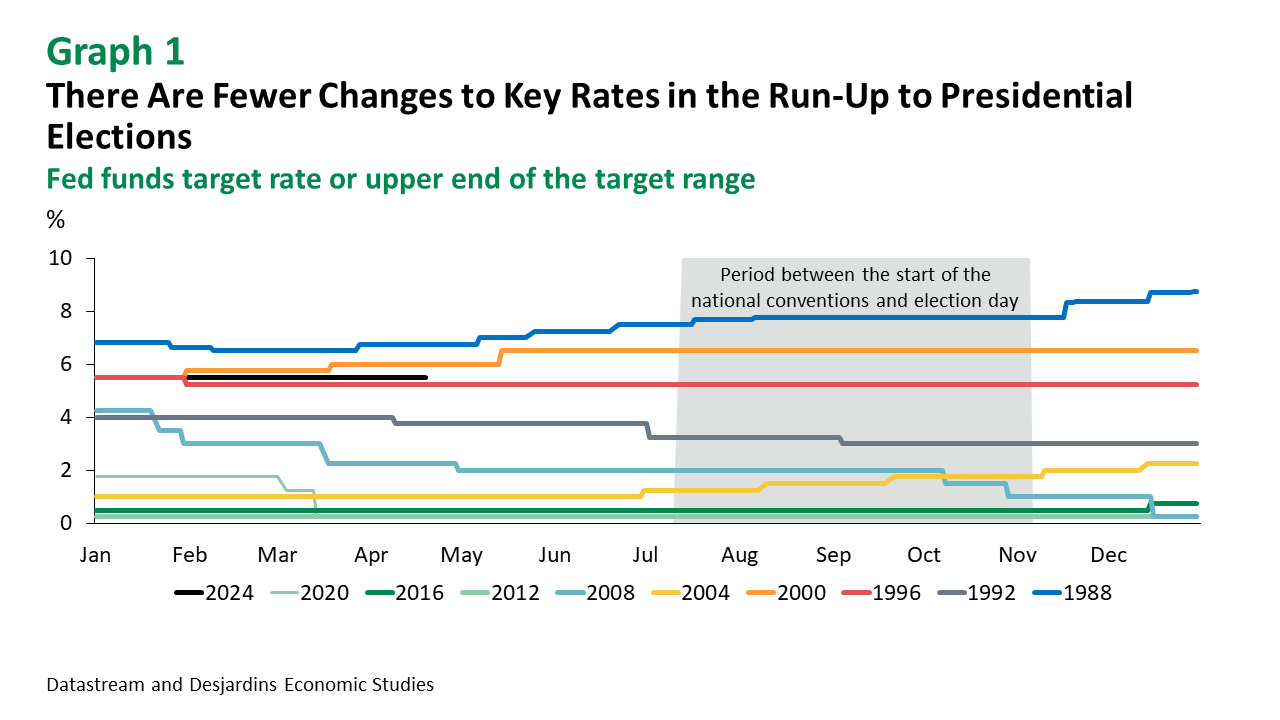

But when we look at key rate movements in every election year since the late '80s (graph 1), we can see that the Fed hasn't changed, much less reversed course on, monetary policy during the run-up to elections (which are always at the start of November). In the past, it hasn't been shy about raising or lowering rates if they were already moving in that direction. That's what happened with the rate cuts in 1992 and 2008, as well as the hikes in 1988 and 2004.

In fact, that's the crux of the problem for this cycle. By ruling out next June's meeting, the Fed will not be able to use the movement already in place to decree a rate cut during the peak election period, which runs from the start of the Republican National Convention on July 15 to election day on November 5. The July 30–31 meeting, which falls between the two conventions (the Democratic National Convention begins on August 19), may also be too early for Fed officials. They want to see inflation fall for several months before they start cutting rates.

Looking further ahead, the meeting that ends on September 18 is just seven weeks before the election, around the time that the televised presidential debates usually begin. Fed officials would have to be pretty gutsy—and able to ignore criticism—if they decide to pivot then. Given the circumstances, and the stubbornness of current inflation, an initial cut just after the November election now seems more likely. Our latest Economic and Financial Outlook External link. sees this as the most likely hypothesis.

Fed officials will also want the first rate change to be fully priced in by the markets before it happens. The detailed minutes of Fed meetings leading up to previous elections show that the Fed views presidential races as a source of uncertainty for financial markets and for businesses’ investment decisions. The Fed will likely want to ease that uncertainty by clearly signalling its intentions, although a rate cut probably wouldn't trigger as much instability as the start of another tightening cycle.

Obviously, if the Fed lowers rates before the election, most of the criticism will come from Republicans. Donald Trump already started sniping at Jerome Powell back in February, saying External link. "It looks to me like he's trying to lower interest rates for the sake of maybe getting people elected, I don't know ... I think he's going to do something to probably help the Democrats, I think, if he lowers interest rates." We can expect more attacks if surprisingly the Fed starts cutting rates just a few weeks before the big day. And if Trump returns to the Oval Office, he'll have some old scores to settle with the Fed. He'll take the first opportunity to appoint his loyalists to the seats on the Fed's board of governors, including a new Fed Chair in 2026.