- Jimmy Jean, Vice-President, Chief Economist and Strategist

Lorenzo Tessier-Moreau, Principal Economist • Hendrix Vachon, Principal Economist

Investment Strategy and Interest Rate Analysis

Key Interest Rate Cuts Are Coming but They Will Be Gradual

February 6, 2024

Highlights

- The US economy remains surprisingly resilient while the rest of the world stagnates.

- The Bank of Canada recognizes the economy is weak but is taking a wait-and-see approach.

- The Canadian dollar will likely remain low if the Bank of Canada is among the first central banks to initiate rate cuts.

- After renewed optimism in late 2023, uncertainty hangs over the stock markets this year.

Economic Trends and Interest Rates

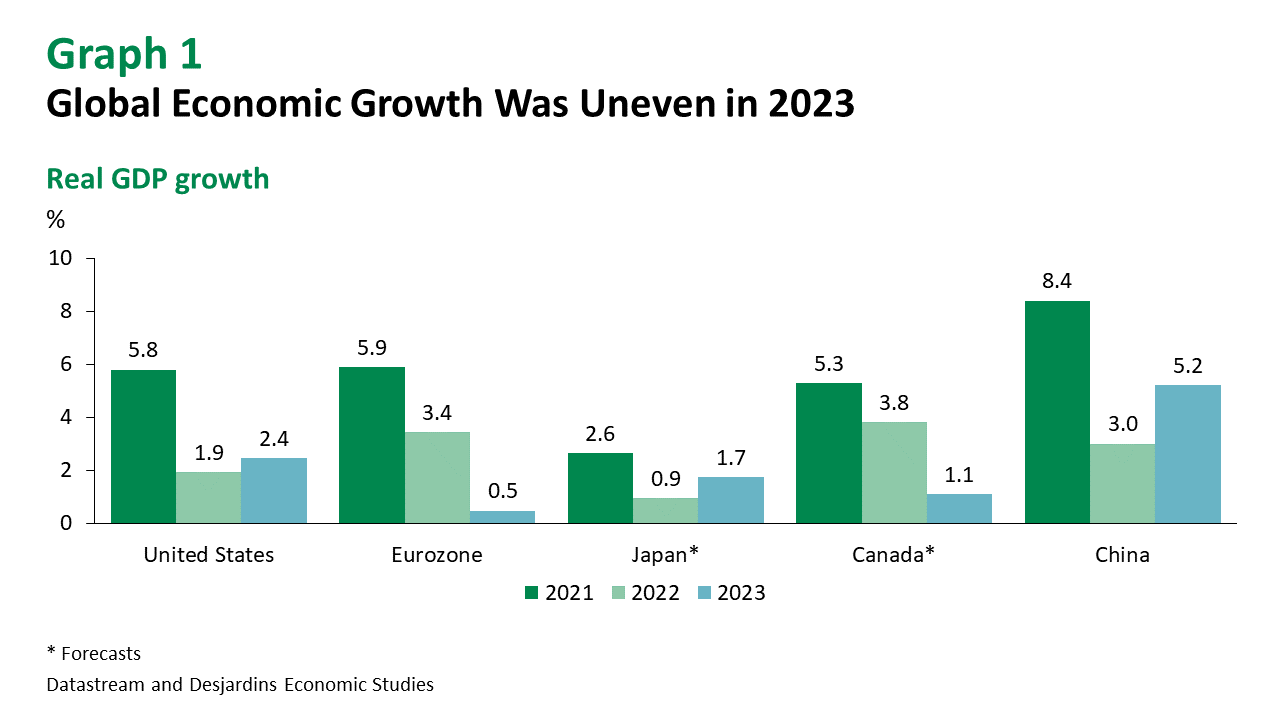

The US Economy Remains Surprisingly Resilient While the Rest of the World Stagnates

Nothing seems to be able to stop economic growth in the United States, where real GDP increased at an annualized rate of 3.3% in the fourth quarter of 2023. The US labour market also continued to show surprising strength by adding more than 350,000 new jobs in January. Not all countries are enjoying this kind of economic vigour. The Chinese economy is going through a difficult transition period. The eurozone narrowly avoided a technical recession, as a stable real GPD figure in the fourth quarter brought down its annual growth to a mere 0.5% (graph 1).

The Fed Isn't Ready to Cut Rates Yet

At its meeting on January 31, the Federal Reserve (Fed) signalled that it was moving a little closer toward federal funds rate cuts. This time, the press release didn't mention the possibility of additional monetary tightening, reflecting a shift to a more neutral stance. However, the Fed did say it doesn't expect it will be appropriate to reduce the key rate until it has gained greater confidence that inflation is moving sustainably toward the target range. Fed Chair Jerome Powell explicitly indicated a low probability of a rate cut in March, contrary to what many investors were expecting.

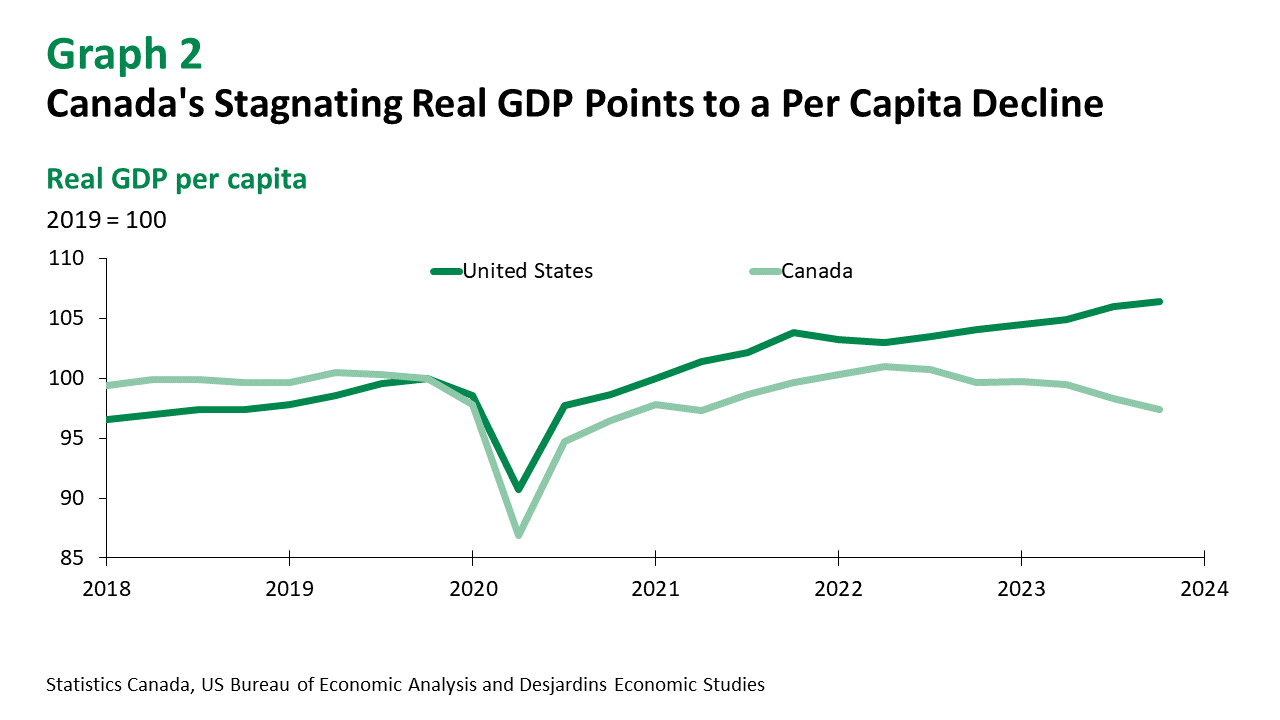

Despite Signs of Weakness, the Canadian Economy Still Isn't in a Recession

There's no doubt that the Canadian economy is going through a rough patch. Unemployment has been on the rise for several months, as job creation fails to keep up with strong demographic growth. Canadians have also seen their purchasing power dwindle over the past several months (graph 2). But the Canadian economy still isn't in a recession, as evidenced by figures from the latest GDP by industry report. Preliminary data from Statistics Canada indicates that production rebounded in November and December, which could push fourth-quarter real GDP about 1.0% higher.

The Bank of Canada Recognizes the Economy Is Weak but Is Taking a Wait-and-See Approach

Like the Fed, the Bank of Canada (BoC) refrained from mentioning the possibility of additional hikes in the press release associated with its meeting on January 24. The BoC left interest rates unchanged due to ongoing concerns about upside risks to inflation. However, the economic outlook published in the Monetary Policy Report was revised downward based on the latest indicators. We expect the BoC to initiate a rate cutting cycle in April. Having said that, we'll be watching Canada's inflation rate, which edged up a notch in December.

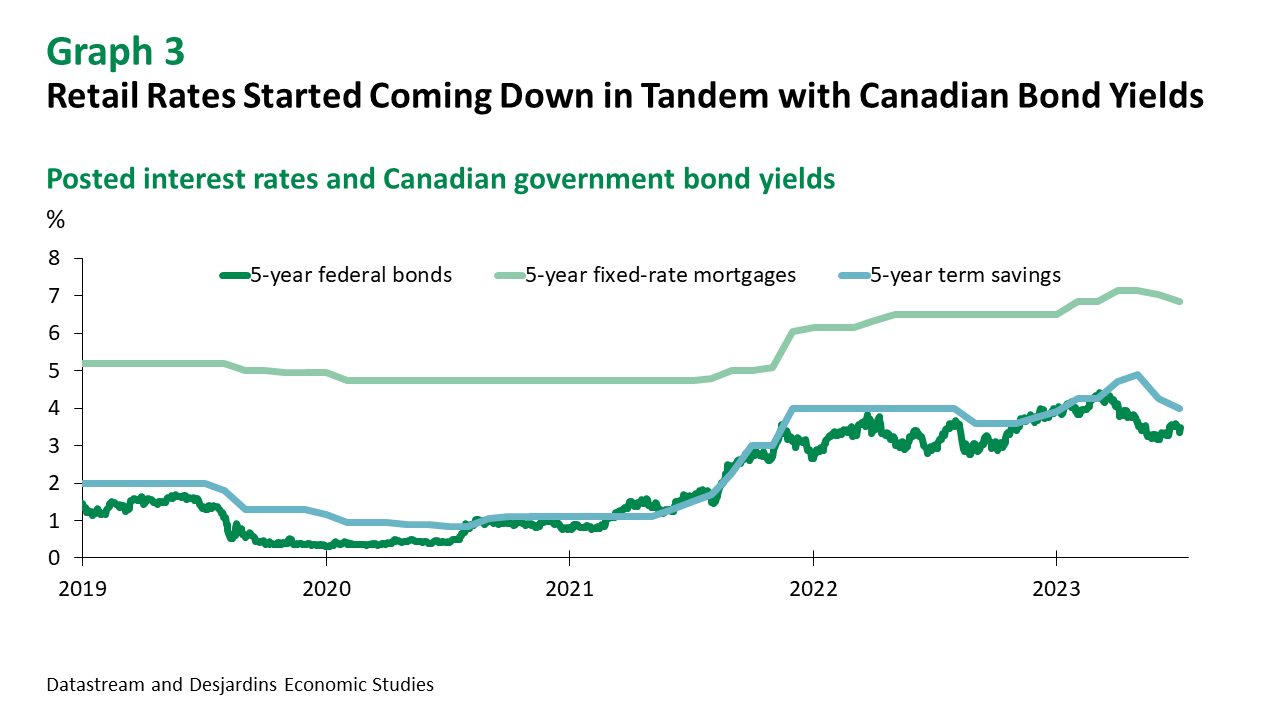

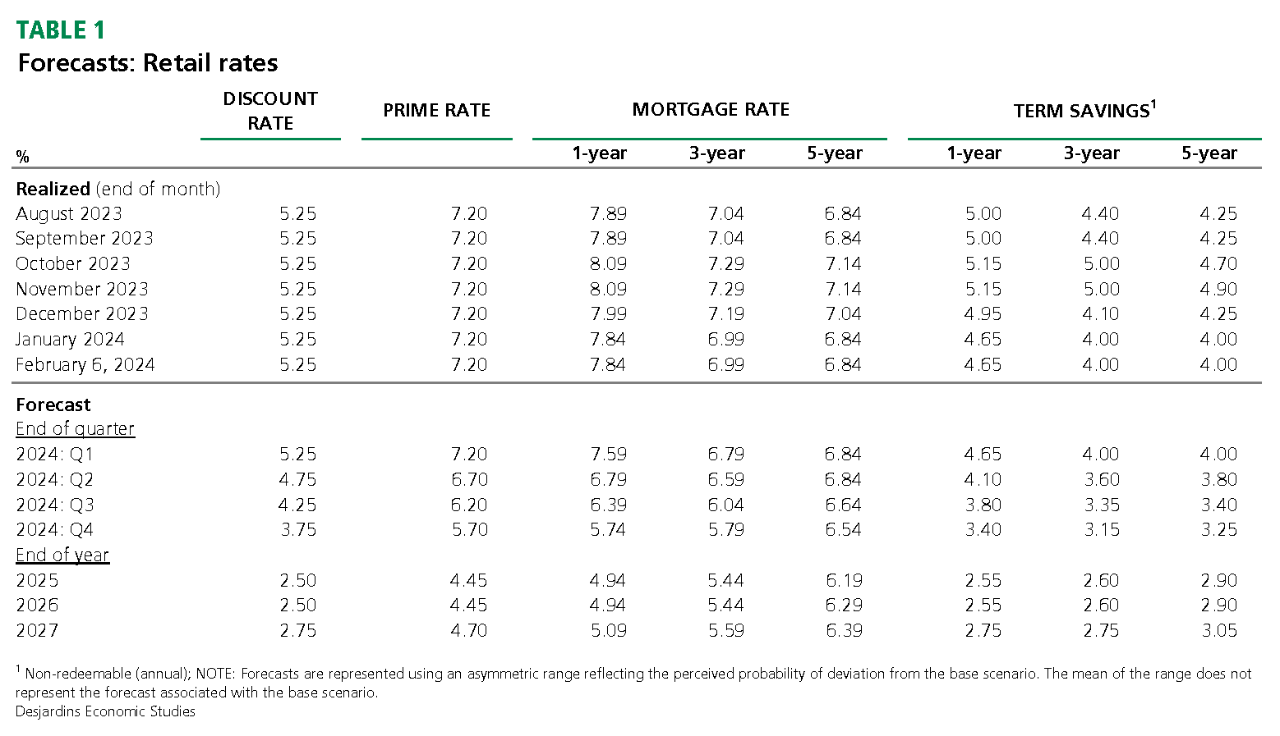

Retail Rates Should Start to Come Down Gradually

Even though policy rates are holding steady, many retail rates have already started coming down. Longer-term bond yields have fallen sharply in recent months, affecting mortgage rates and savings vehicles with the same term (graph 3). Even though key rate cuts are most likely on the way, their impact on retail rates may be limited. For the most part, current rates already reflect the expected key rate cuts.

Exchange Rate

The Canadian Dollar Will Likely Remain Low If the Bank of Canada Is Among the First Central Banks to Initiate Rate Cuts

The Fed's more accommodative stance in December influenced the currency market toward the end of 2023. Expectations for more expedient rate cuts in the US narrowed the differential with other countries and led to several currencies appreciating against the greenback. The gains were also driven by investors' higher risk appetite and increased confidence in a soft landing (lower inflation, lower interest rates and continued economic growth).

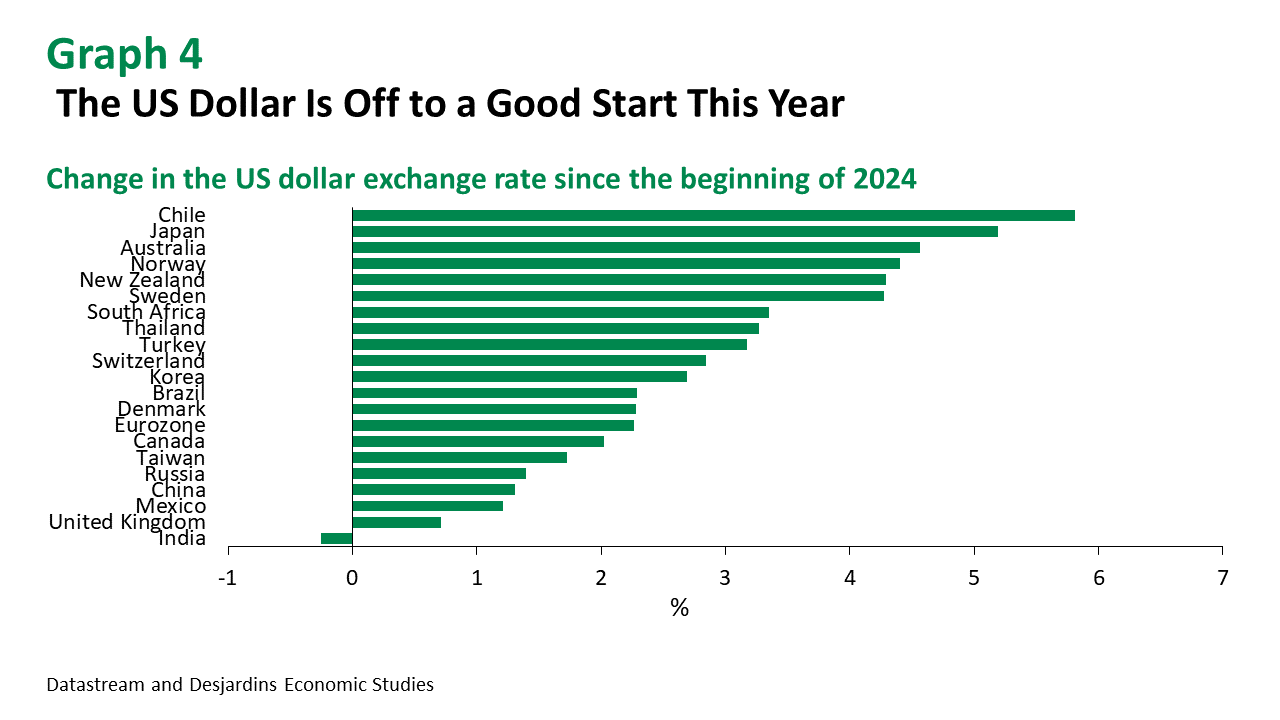

But since the beginning of 2024, the value of the US dollar has recovered against many currencies as US rate cut expectations moderated (graph 4). As a result of the greenback's renewed strength, the Canadian dollar fell roughly 2.0%. And yet, the loonie is faring a little better than other currencies. With certain core inflation measures rising again and recent monthly GDP data pointing to a stronger-than-expected economy, doubts have cropped up about upcoming interest rate cuts in Canada. However, like many other central banks, the Bank of Canada recently changed its tone by stating that it no longer expects to have to raise rates further.

Exchange Rate Volatility Is Expected to Remain High in the Near Term

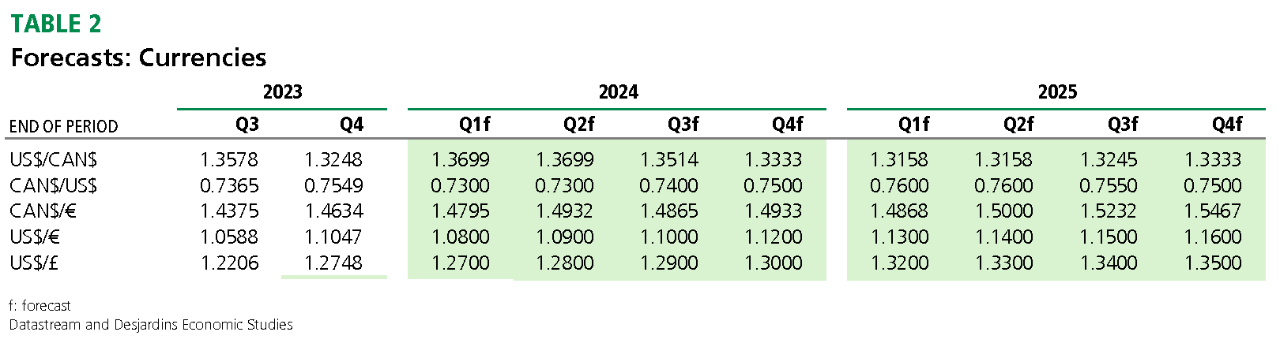

In the coming months, changing monetary policy expectations should fuel a lot of currency movement. Countries that cut rates sooner will likely see their currencies depreciate more. This could be the case for the Canadian dollar if inflation slows as expected and the next round of economic data points to deteriorating conditions. By spring, the loonie could be trading around C$1.37/US$ (US$0.73).

In the second half of the year, we should see the loonie and several other currencies appreciate against the greenback, which tends to lose value as investor risk appetite increases. We also expect commodity prices to rebound later in the year, which should bolster the Canadian dollar (graph 5).

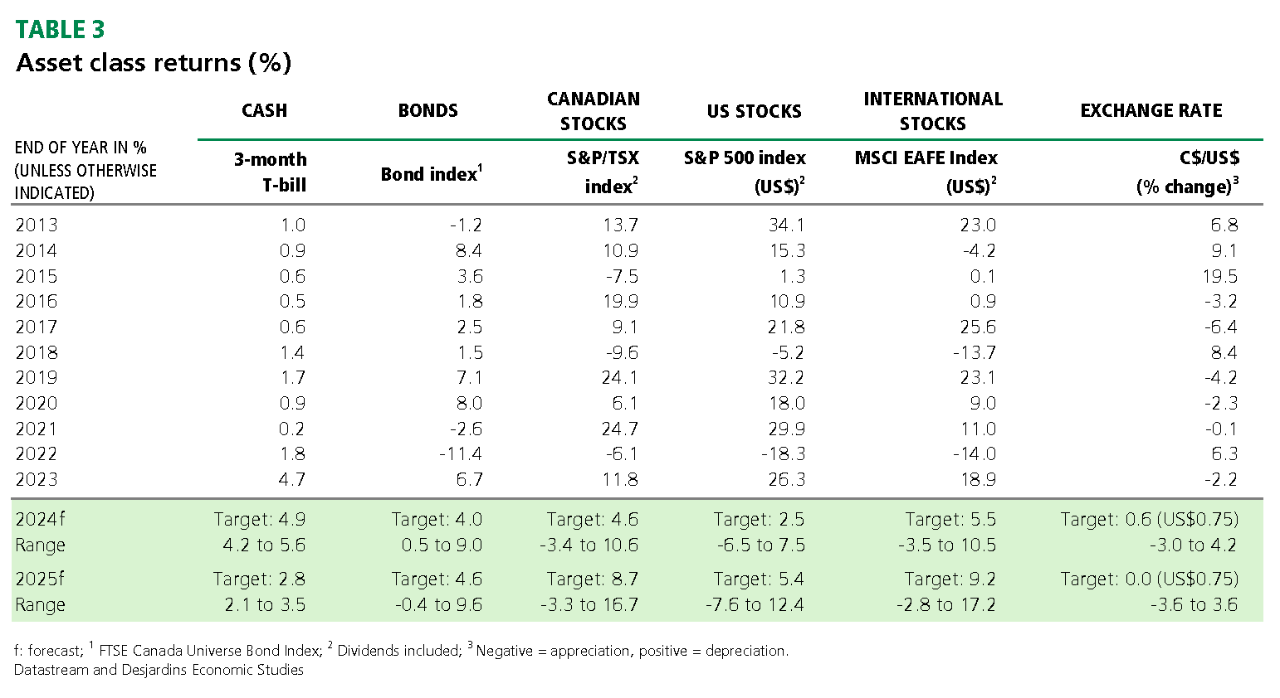

Asset Class Returns

After Renewed Optimism in Late 2023, Uncertainty Hangs over the Stock Markets This Year

Investor Sentiment Remains Positive at the Start of the Year

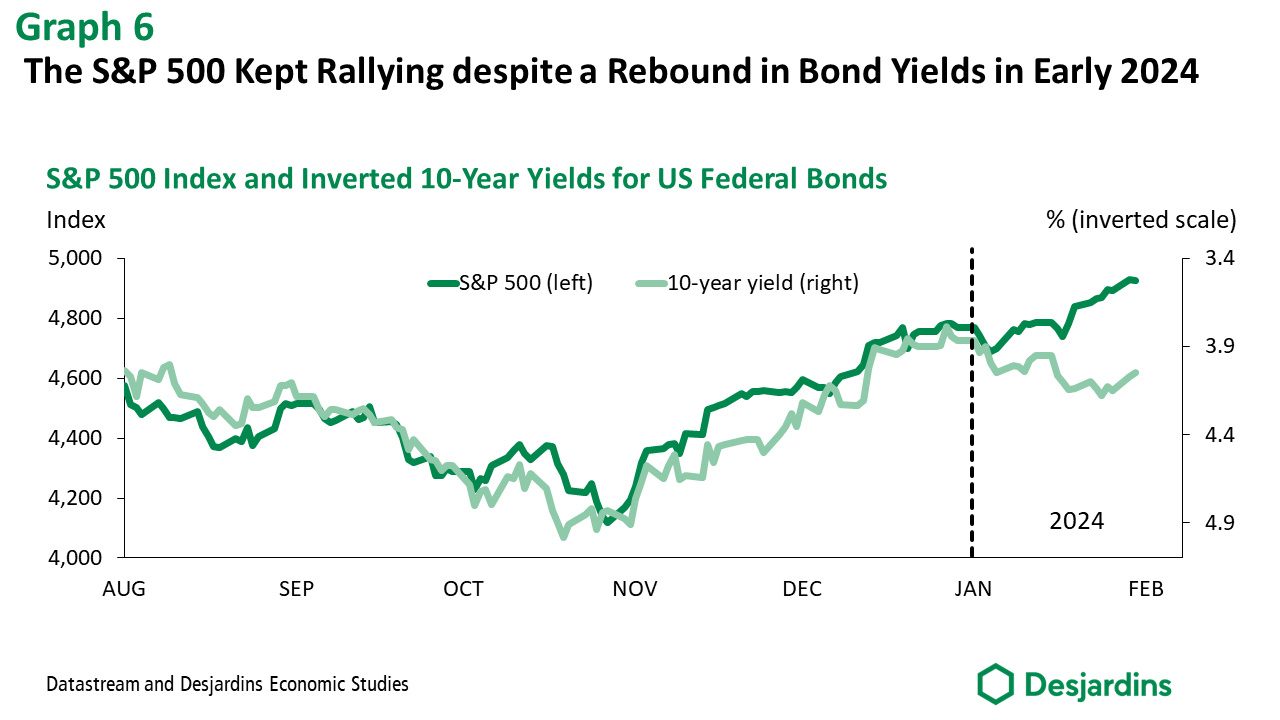

Global stock market indexes ended 2023 with strong gains fueled by a rapid decline in long-term bond yields. And yet, investor optimism wasn't shaken when yields increased in early 2024 (graph 6). Stock market indexes kept climbing at the beginning of the year, particularly in the United States in response to positive signals about economic growth and inflation. While the rate cuts expected this year should be good news for market returns, it seems that investors have largely anticipated this effect already.

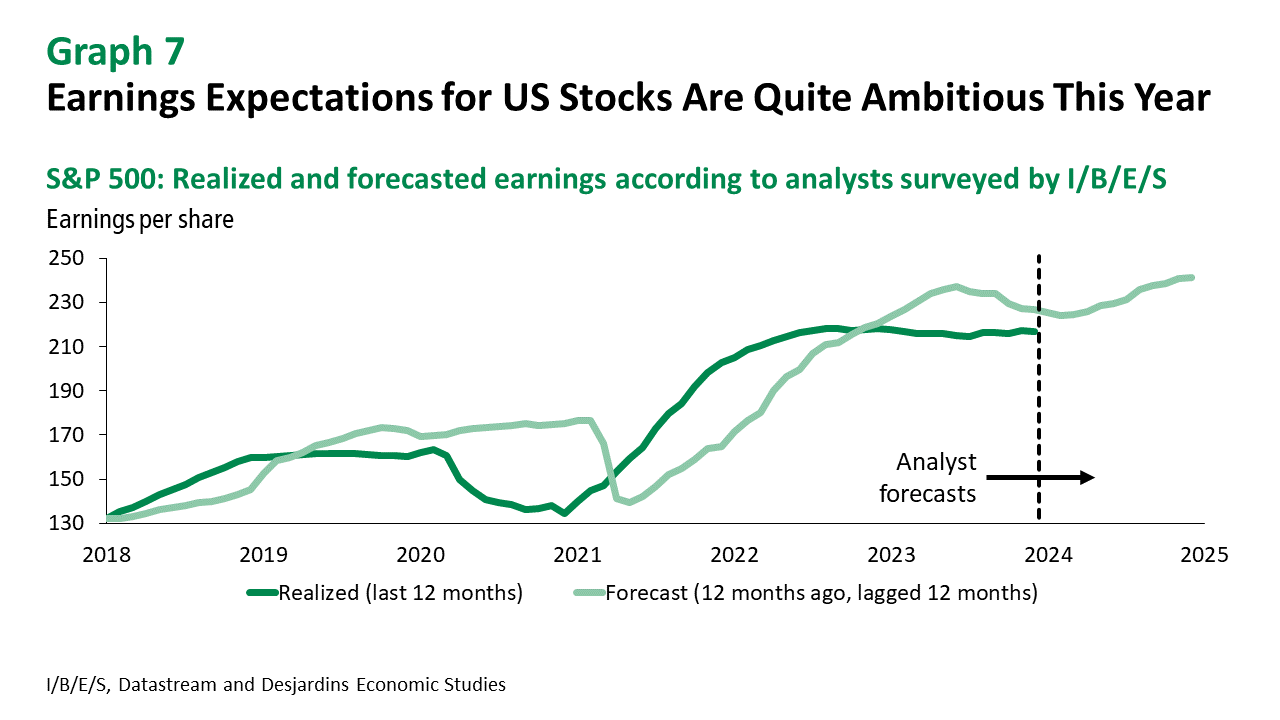

2023 Set the Bar High for This Year's Stock Market Returns

The strong stock market performance in 2023 isn't necessarily good news for returns this year. Even though the market rally is partly attributable to the improved economic outlook and higher earnings expectations, it's also supported by some very ambitious expectations for select companies (graph 7). In fact, the seven largest companies in the S&P 500—often referred to as the Magnificent Seven—contributed to roughly 60% of the index's gains in 2023. These companies have price-to-earnings ratios that vary between 25 and 80, which suggests that their valuations are strongly based on their ability to expand rapidly.

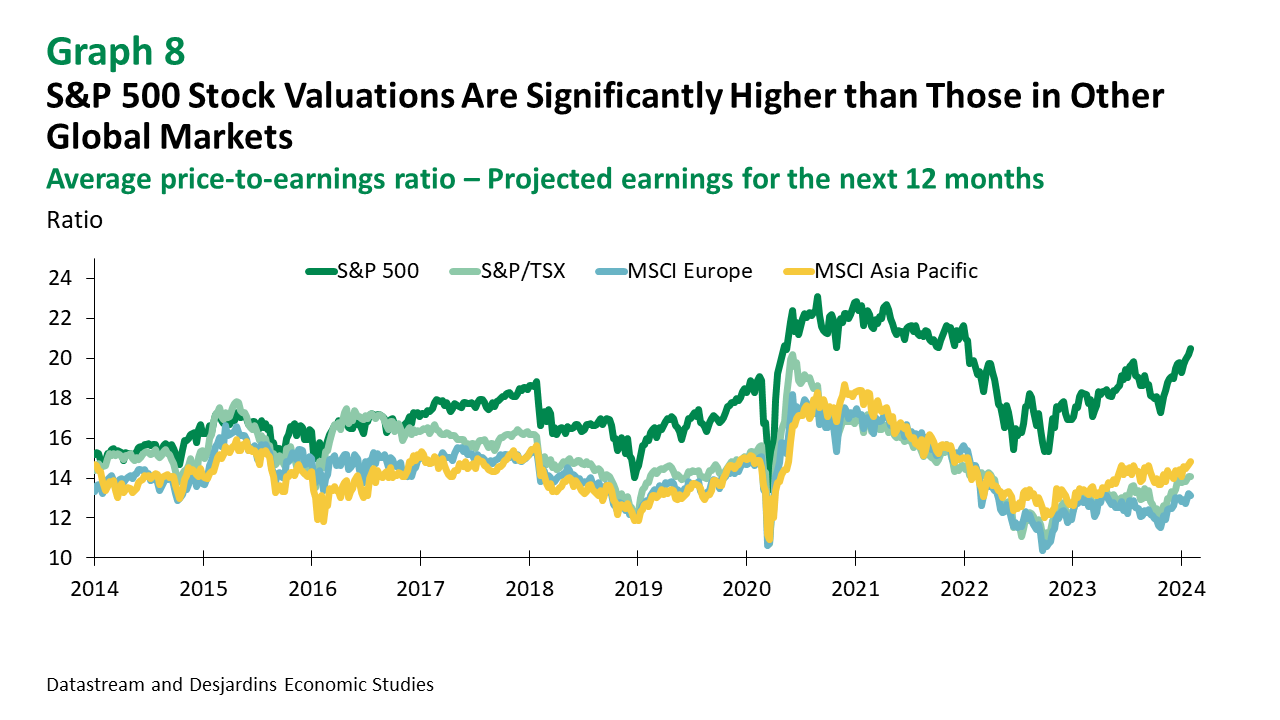

The Gloomy Outlook for the Canadian Economy Is Weighing on the S&P/TSX

Despite rallying in late 2023, the S&P/TSX is still starting the year with a much lower average valuation than the S&P 500 (graph 8). That's because the Canadian economy faces its own set of risks. To begin with, the Canadian economy should continue to experience difficulties, which would result in lower corporate profits. Canada's highly indebted households will continue to struggle under elevated interest rates, with repercussions extending beyond 2024. Their high debt levels put the financial sector's profits at risk. However, support could come from recovering commodity prices.

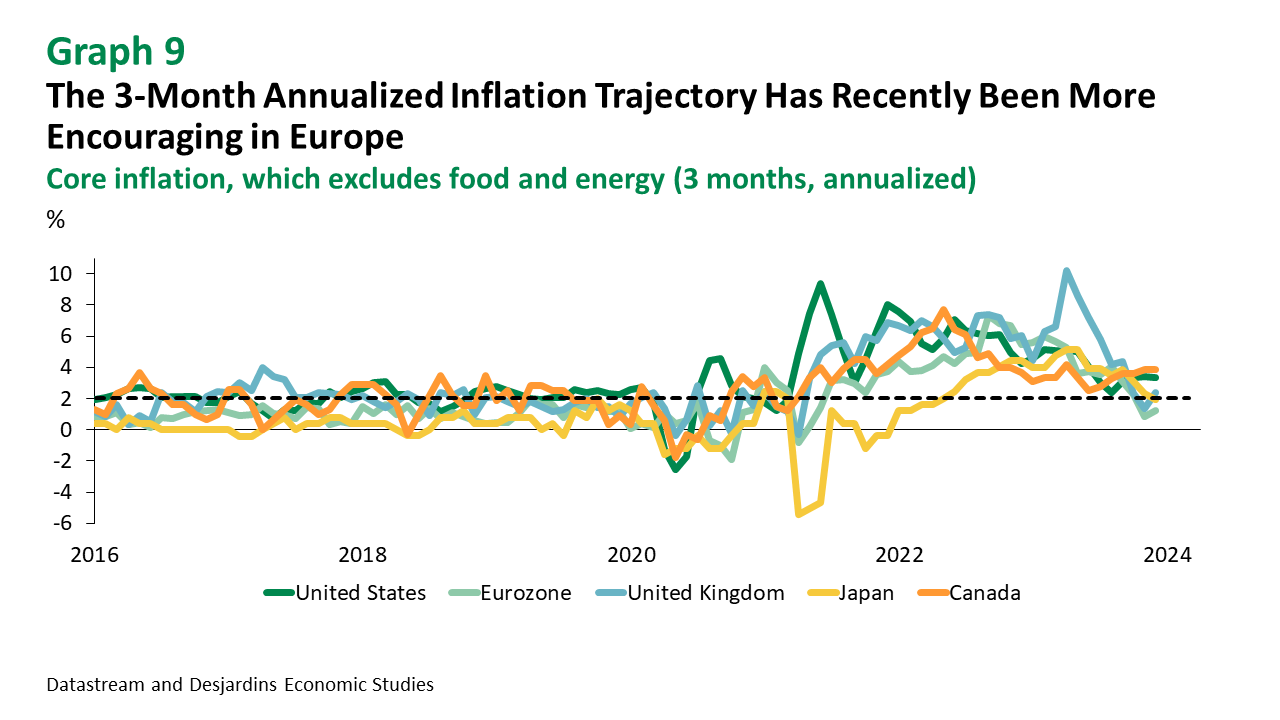

Central Banks in Several Countries Have Become More Dovish in Tone

Most central banks have closed the door to additional rate hikes. The Bank of Japan is an exception, having postponed interest rate hikes for fear that inflation will weaken again in the medium to long term. The European Central Bank is expected to cut rates this spring and the Bank of England will likely follow suit this summer. Across Europe, real progress has been made to tame inflation in recent months (graph 9). In the second half of the year, rate cuts in most economies will spur investors to take more risks. Even though many stock market indexes may face headwinds in the coming months due to ongoing economic challenges, the outlook is more encouraging if we look a little further down the road.

New Sources of Uncertainty Could Affect Returns in 2024

Going into the new year, investors seem to be looking past certain risks. Inflation is less of a concern, as demonstrated by plummeting bond yields, and the stock market rally seems to reflect a lower risk of recession. But asset valuations are already factoring in this improved outlook, and earnings could be more moderate going forward. Other sources of uncertainty could affect returns in 2024 as the economy normalizes. Technologies like generative artificial intelligence, which has garnered a tremendous amount of enthusiasm, and high valuations for select companies, will be put to the test. The US presidential election could also trigger market turmoil, while geopolitical risks, such as the war in Ukraine and the Israeli offensive in Gaza, continue to be potential sources of disruption.