- Hendrix Vachon

Principal Economist

FX Analysis

Bond Yield Spreads Are Still Favourable to the US Dollar

October 26, 2023

Highlights

- US bond yields are rising more quickly than in many other countries, which is positive for the greenback. More investors are pricing in a scenario where the Federal Reserve keeps rates higher for longer. The markets aren't expecting many interest rate cuts in 2024. The US economy continued to show its strength throughout the third quarter, making a recession in the coming quarters less likely.

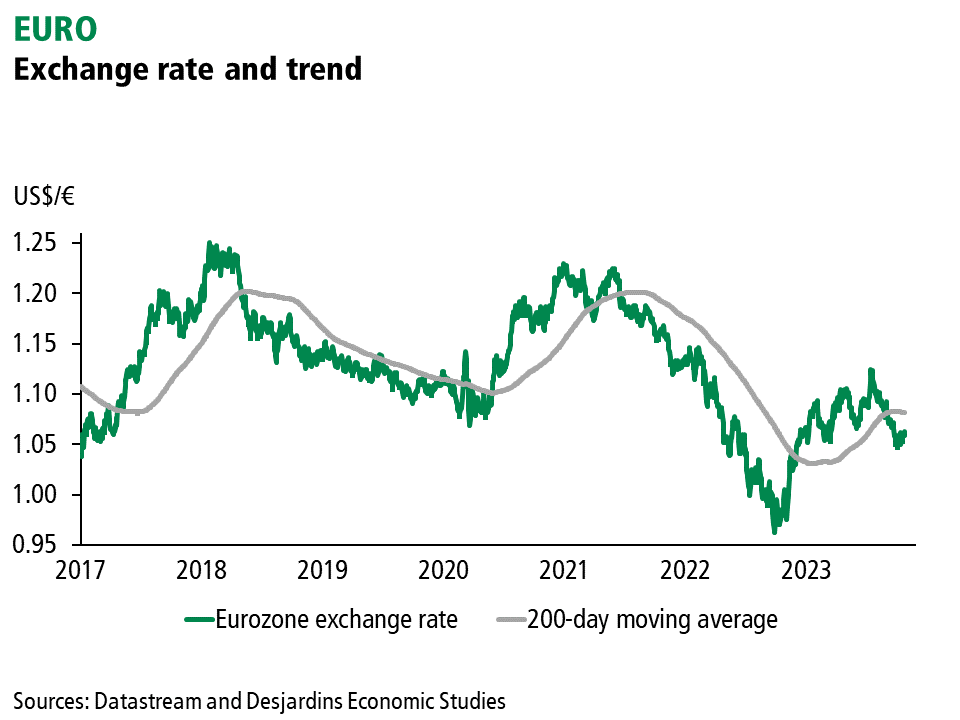

- That said, the US dollar isn't as strong as it was last year. Recession fears in several countries were more acute in the fall of 2022 amid rapidly rising interest rates. The financial markets were more volatile, with stock markets posting larger losses. Although a degree of uncertainty remains, the US dollar isn't as much of a safe haven as it was a year ago. This is particularly true against European currencies which are no longer hampered by major risk of an energy crisis.

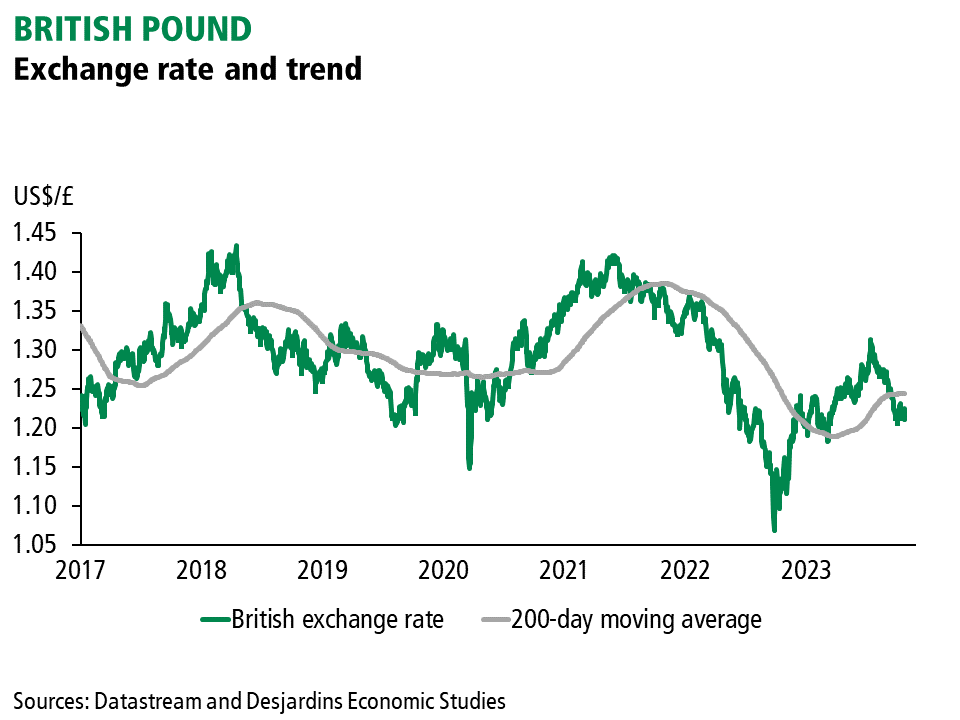

- At near US$1.06, the euro is trading below its historical average, however. Economic growth is almost flat in the eurozone. This has helped rein in inflation and the European Central Bank paused its monetary tightening. The scenario for the pound is a little different. The UK economy is also facing headwinds—although inflation is falling, it's much higher than in the eurozone. The Bank of England hit pause at its last monetary policy meeting, but that could prove short-lived.

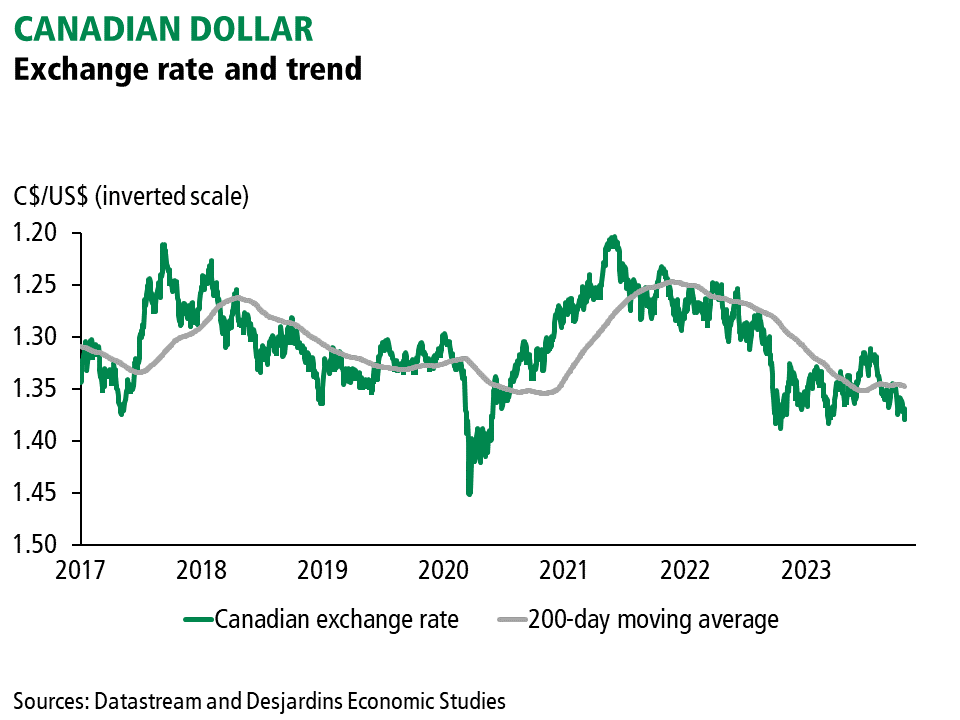

- The Canadian dollar has been trading at around CAN$1.37/US$ since early October, which is about where it was a year ago. High oil prices haven't been enough to offset the other issues holding the loonie back, such as Canada's deteriorating economic situation and widening bond yield spreads with the US. Instead of tracking the 2-year yield spread, the Canadian exchange rate now seems more closely aligned with the 10-year spread.

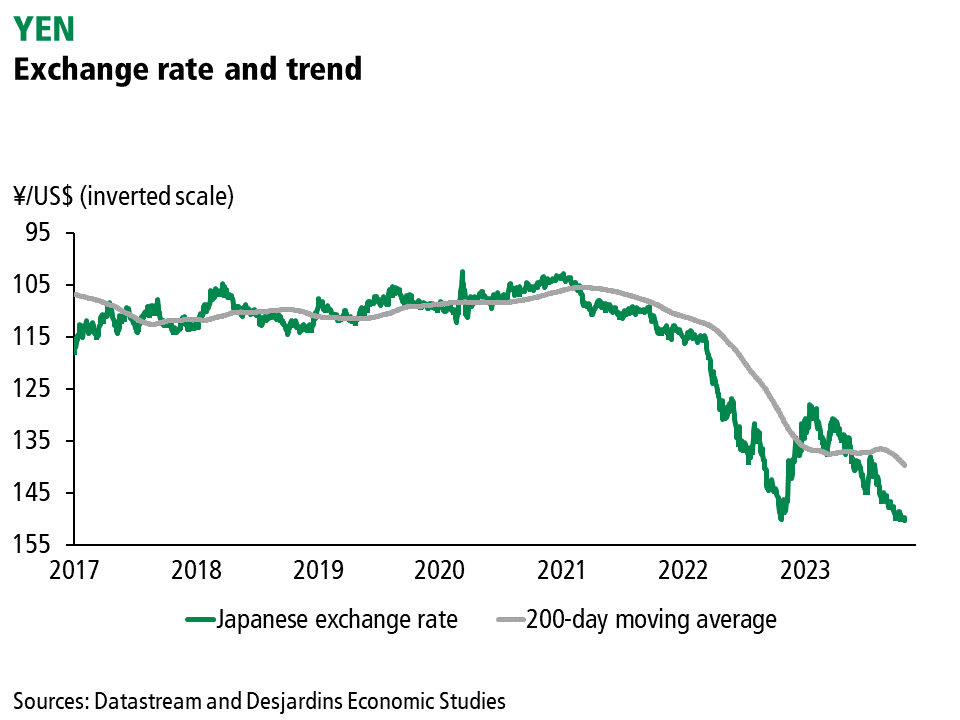

- The Japanese yen is holding close to 150 yen/US$. The Japanese monetary authorities propped up the yen in the fall of 2022 by selling off assets in US dollars. History might be repeating itself already. However, a more effective way of supporting the yen would be to raise interest rates, which the Bank of Japan has so far refused to do, although it's being more flexible with the cap on the 10-year bond yield, which is approaching 0.90%.

Main Factors to Watch

- Although the US economy is still holding up, it's expected to slow significantly over the coming quarters. As excess savings accumulated during the pandemic are depleted and student loan payments resume, demand should eventually start to weaken. The labour market is also rebalancing, and the number of job vacancies is declining, which should mean lower wage growth for employees. Bond yields could quickly resume their downward trend in 2024, which would remove a significant support for the US dollar.

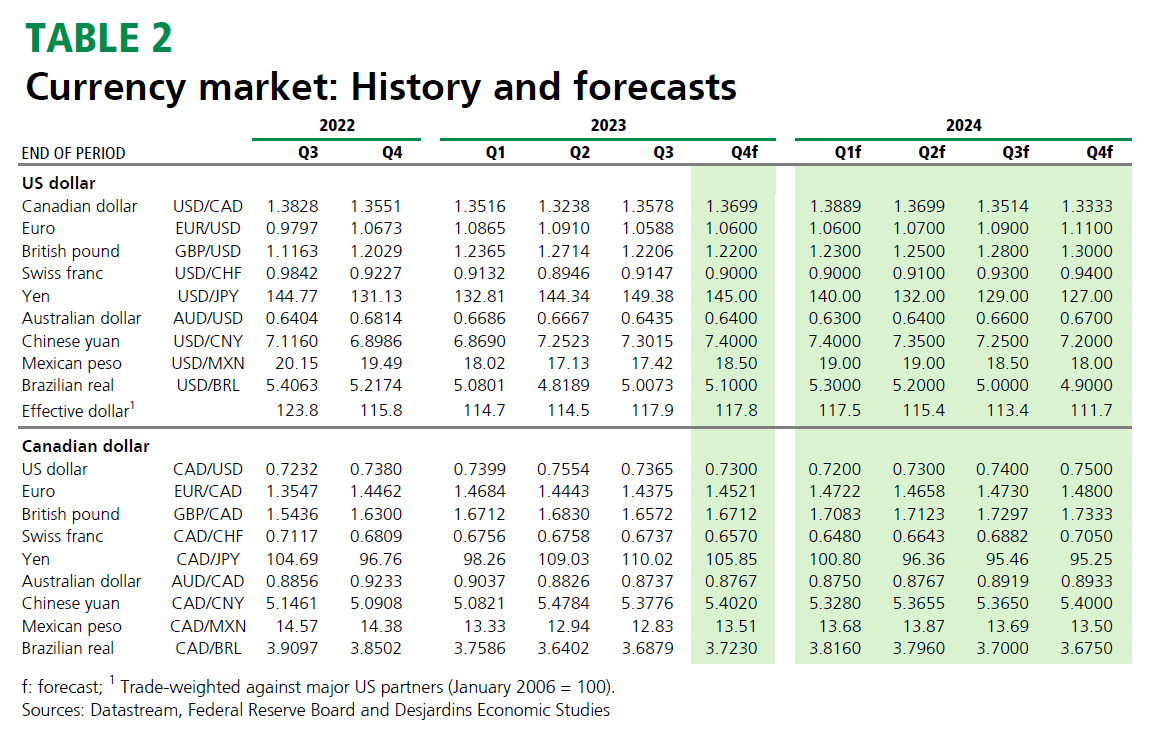

- The Canadian dollar is expected to remain weak in the short term. It could fall to US$0.72 (CAN$1.39/US$) in early 2024. This would be in line with the mild recession forecast in Canada and the decline in commodity prices, including oil. A modest appreciation could follow, underpinned by an economic recovery and higher commodity prices. However, bond yield spreads are likely to continue hampering the loonie, as the Bank of Canada is expected to start cutting interest rates earlier than the Fed.

Main Exchange Rates