- Hendrix Vachon

Principal Economist

FX Analysis

The Greenback Falls on Lower Bond Yields

November 29, 2023

Highlights

- We've seen a reversal of fortunes in many currency pairs in recent weeks. This has been driven primarily by declining bond yields, especially in the United States, hitting the greenback hard. Renewed risk appetite also exacerbated the US dollar's overall weakness.

- The turning point for bond yields and exchange rates was the Fed's shift to a more dovish stance after its November 1 monetary policy meeting. The good news on inflation, which is falling slightly faster than expected in many countries, also reinforced the notion that most central banks have reached the end of their tightening cycle. Investors have lowered their expectations on interest rates for next year as well.

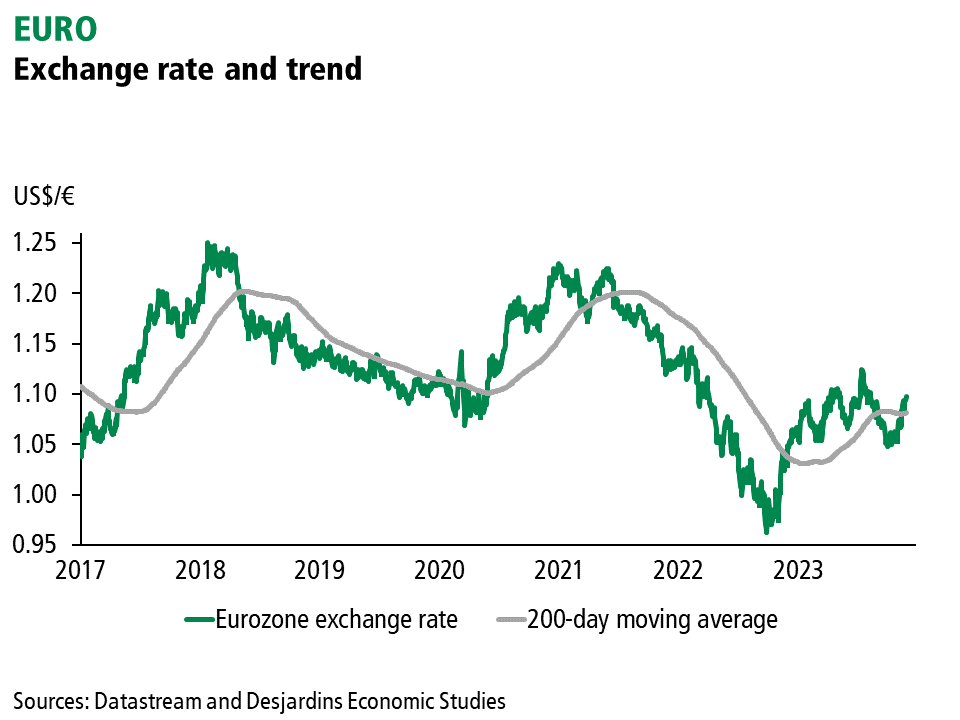

- The US 10-year yield, which spent the second half of October hovering between 4.80% and 5.00%, is now around 4.40%. But yields have come down more in some places than in others, buoying currencies in Europe and elsewhere. The euro, which was trading below US$1.06 in late October, is now trading near US$1.10. Meanwhile the pound is up to US$1.27 after ending October below US$1.22.

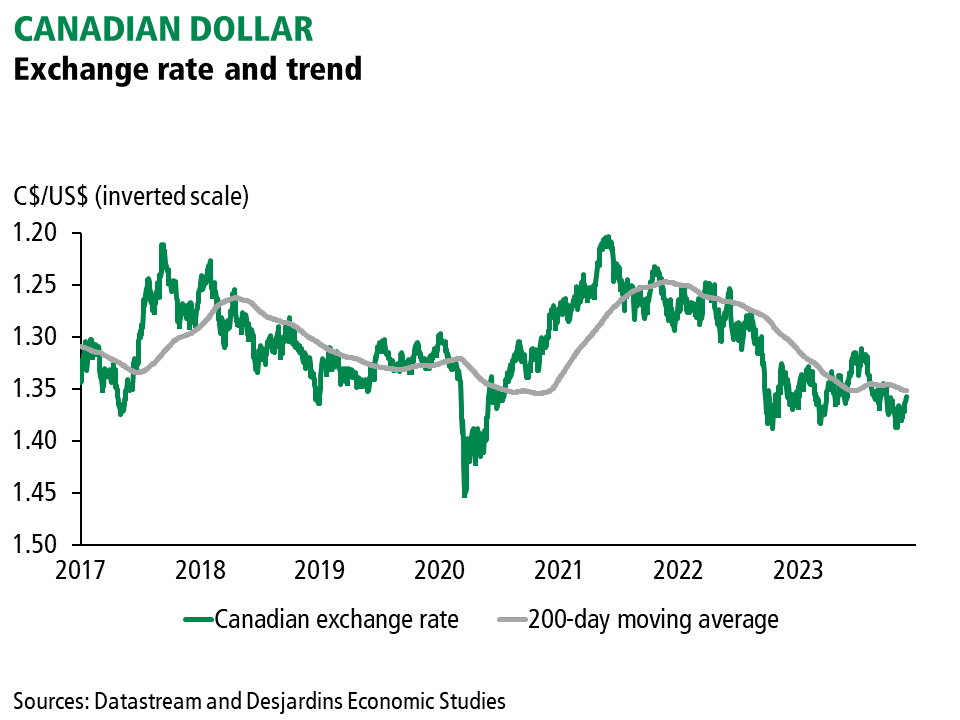

- The Canadian dollar got one of the smallest bumps from widening yield spreads, appreciating by about 2% in November. Canadian bond yields have followed the trend in US yields more closely. The loonie's rise began in earnest in mid-November, after US inflation data and several more encouraging economic indicators for the Chinese economy were released. Those numbers sharpened investors' risk appetite.

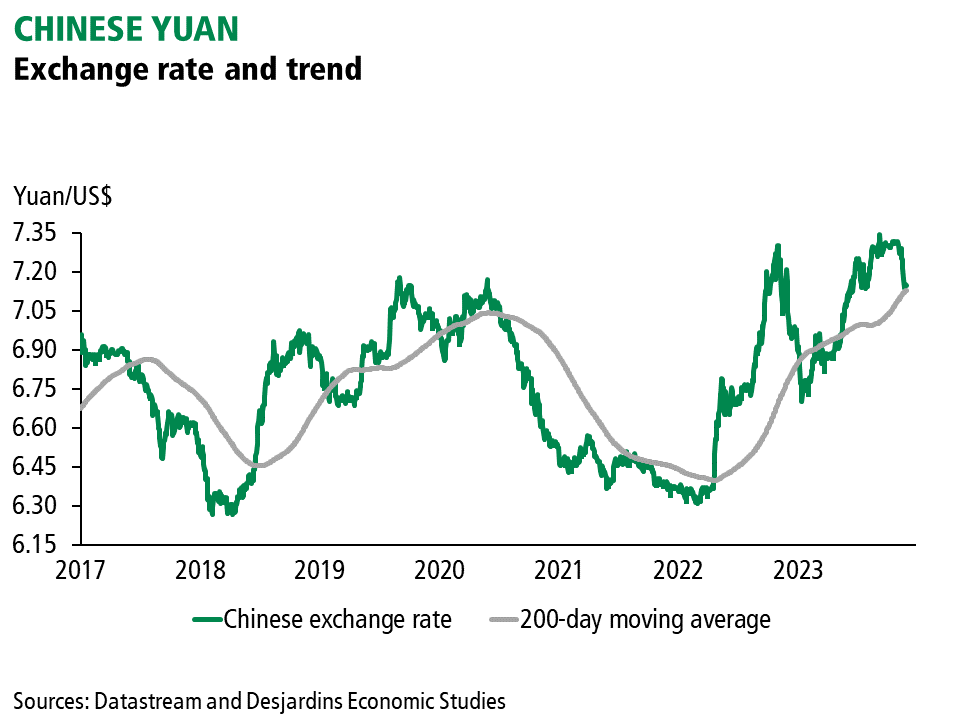

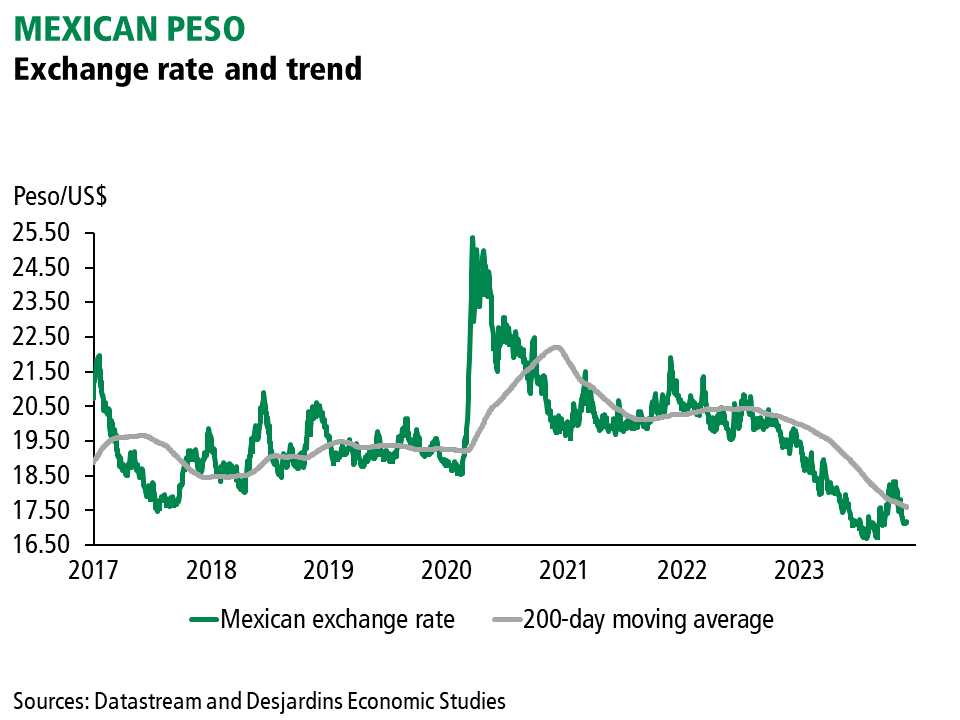

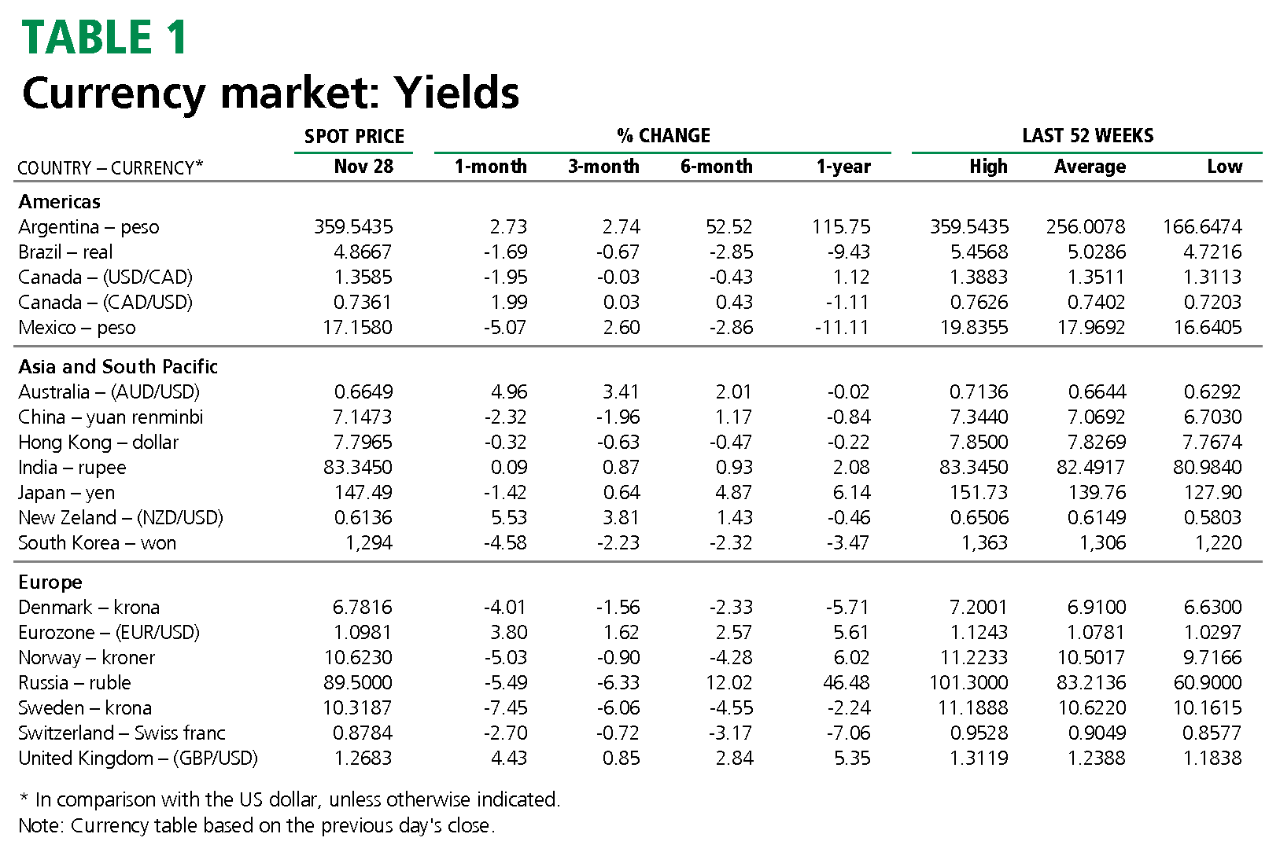

- The more upbeat Chinese data boosted the yuan, which is again trading around 7.15 yuan/US$. Several other emerging market currencies posted substantial gains in November, including the Mexican peso, which jumped more than 5%.

Main Factors to Watch

- The current slump in a number of bond yields remains in line with our forecast for the end of 2023. Even so, markets may continue to be highly volatile. If central bankers take a slightly more hawkish tone or inflation readings come in a bit higher than expected, bond yields and currencies could lose some of their recent momentum. On the flip side, yields may drop further in the coming weeks if inflation keeps falling sharply and central banks signal more openness to future interest rate cuts.

- Risk appetite could have an even bigger impact on exchange rates in the weeks and months to come. Our baseline scenario sees many economies experiencing economic hardship over the short term. That includes China, which is still grappling with major structural weaknesses. We therefore believe the US dollar will rebound by the end of this year or early next year amid lower risk appetite.

- Meanwhile the Canadian dollar remains very sensitive to investor sentiment and the state of the global economy. We believe it will depreciate slightly in the short term before bouncing back later in 2024. The Canadian economy also faces its own challenges. We still expect Canada to dip into a mild recession in the first half of 2024.

Main Exchange Rates