- Jimmy Jean, Vice-President, Chief Economist and Strategist • Hendrix Vachon, Principal Economist

FX Analysis

The US Dollar Holds Strong as Interest Rate Cuts Are Expected to Be More Gradual in the United States

March 28, 2024

Highlights

- While some data suggest that the US economy is slowing, it’s still faring better than most other advanced economies. According to our latest forecasts External link., US GDP growth should come in around 2% in the first quarter and then possibly slow a little more in the second quarter. Meanwhile, many other countries can expect their economies to stagnate with practically zero growth. Inflation also seems to be stickier in the United States than elsewhere. This complicates things for the Federal Reserve, but the central bank has nonetheless left the door open to cutting interest rates in the near future. That said, the pace of rate cuts is expected to be gradual, which is helping to keep the US dollar at historically high levels.

- Eurozone inflation is also proving to be more stubborn than expected, falling slightly short of expectations in February. As a result, the euro appreciated in early March, but was unable to maintain its gains. It’s currently trading at just over US$1.08, which is similar to last month. The European Central Bank maintained a relatively cautious tone during its March monetary policy meeting but conceded that it could review its position by June in light of recent data and forecasts.

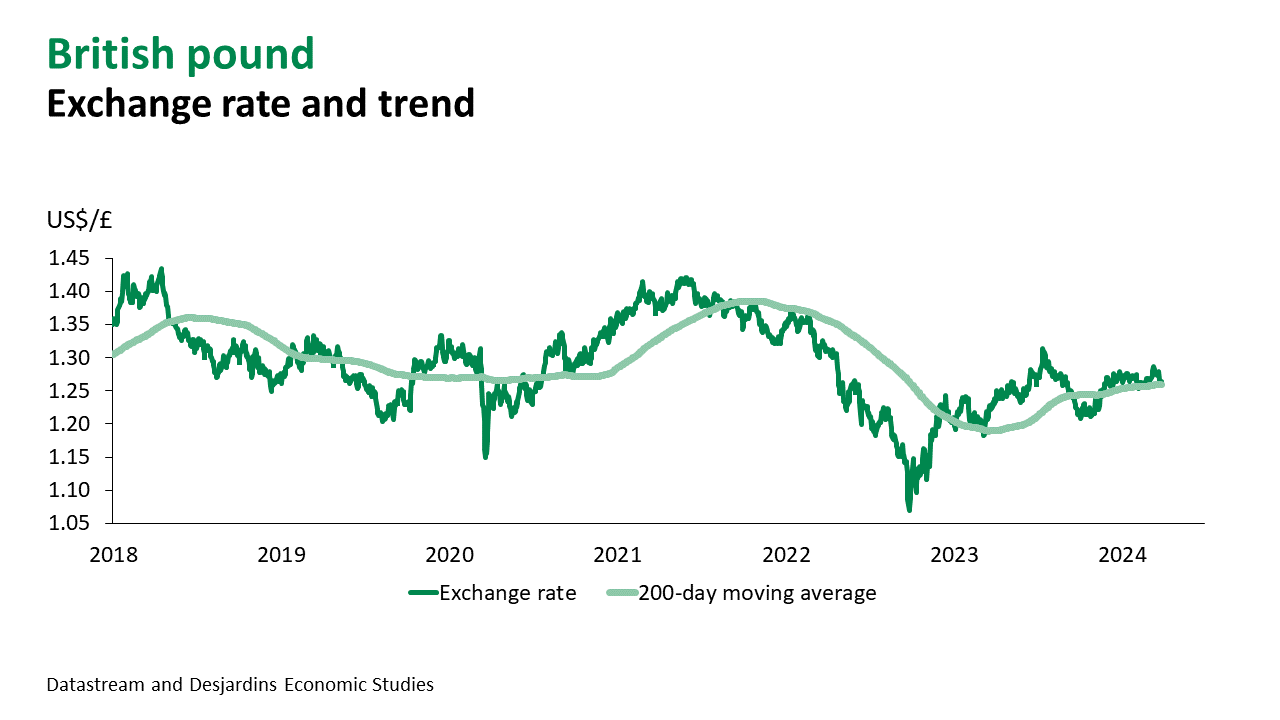

- The pound didn’t do much better than the euro in March and is currently trading at around US$1.26. Even though inflation is running higher in the United Kingdom, the Bank of England is encouraged by recent easing. At its most recent Monetary Policy Committee meeting, no members voted to increase the policy rate, in contrast with two at the previous meeting.

- Canada’s economy seems to be a little stronger than Europe’s, but its situation is more precarious if you exclude the effects of demographic growth. Inflation has continued to edge down recently, even more than expected. Now that a long streak of rate cuts seems more likely in Canada, spreads with US bond yields have widened and the Canadian dollar has remained stuck at around CAN$1.36/US$.

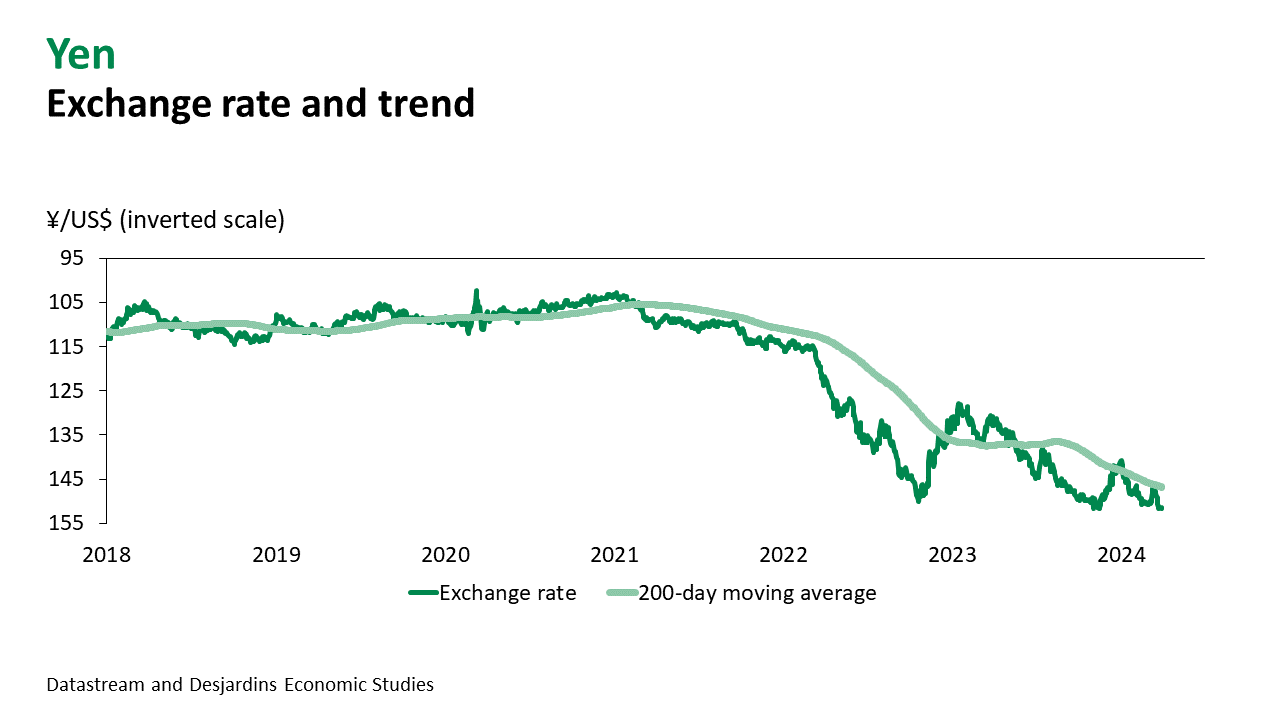

- We were interested to see how the yen would react to the recent monetary policy pivot in Japan. Despite the country’s first interest rate hike since February 2007, the yen depreciated, finishing comfortably above ¥150/$US. Since investors don’t expect to see multiple rate hikes in Japan, rate spreads with the United States continue to weigh heavily on the yen.

- The Swiss franc depreciated again after the Swiss National Bank announced a first interest rate cut in March. The decision was justified, however, as the country’s inflation rate has been below 2% for a while. The franc is now trading at over 0.90 francs/US$.

Main Factors to Watch

- Changing expectations for monetary policy could still influence the currency market over the next few months. Following much speculation about the timing of the first rate cut, investors will likely turn their attention to the pace of upcoming cuts and potential differences in major central bank decisions. Everyone will be watching inflation data closely. For the time being, it looks like the Federal Reserve will cut rates a little more gradually than most other central banks, which should continue to buoy the US dollar. But if the global economy starts to recover, many currencies could make some gains later this year and in 2025.

- The potential for appreciation seems lower for the Canadian dollar. Inflation has already come down considerably in Canada, and we still believe the Bank of Canada will make several interest rate cuts starting in June. Interest rate spreads will probably hold the loonie back. Commodity prices are expected to go up, but not enough to sustainably push the Canadian exchange rate below CAN$1.33/US$ this year or next.

Main Exchange Rates

Currency Market