- Jimmy Jean, Vice-President, Chief Economist and Strategist • Hendrix Vachon, Principal Economist

FX Analysis

Several Currencies Kicked Off the Year by Erasing Some of Their December Gains

January 25, 2024

Highlights

- The Federal Reserve’s more dovish tone in December was a pivotal moment for the currency market. Interest rate differentials narrowed as hopes grew for sooner-than-anticipated rate cuts in the United States, and several currencies appreciated against the US dollar. These gains were also fueled by higher investor risk appetite and a growing confidence in the soft landing scenario—a drop in inflation, lower interest rates and continued economic growth. But this momentum has faded somewhat.

- Since the beginning of the year, expectations of an interest rate cut have been more moderate. Some caution still seems warranted: the fight against inflation is not yet over, and the most recent inflation data suggest that progress has been more limited in some countries.

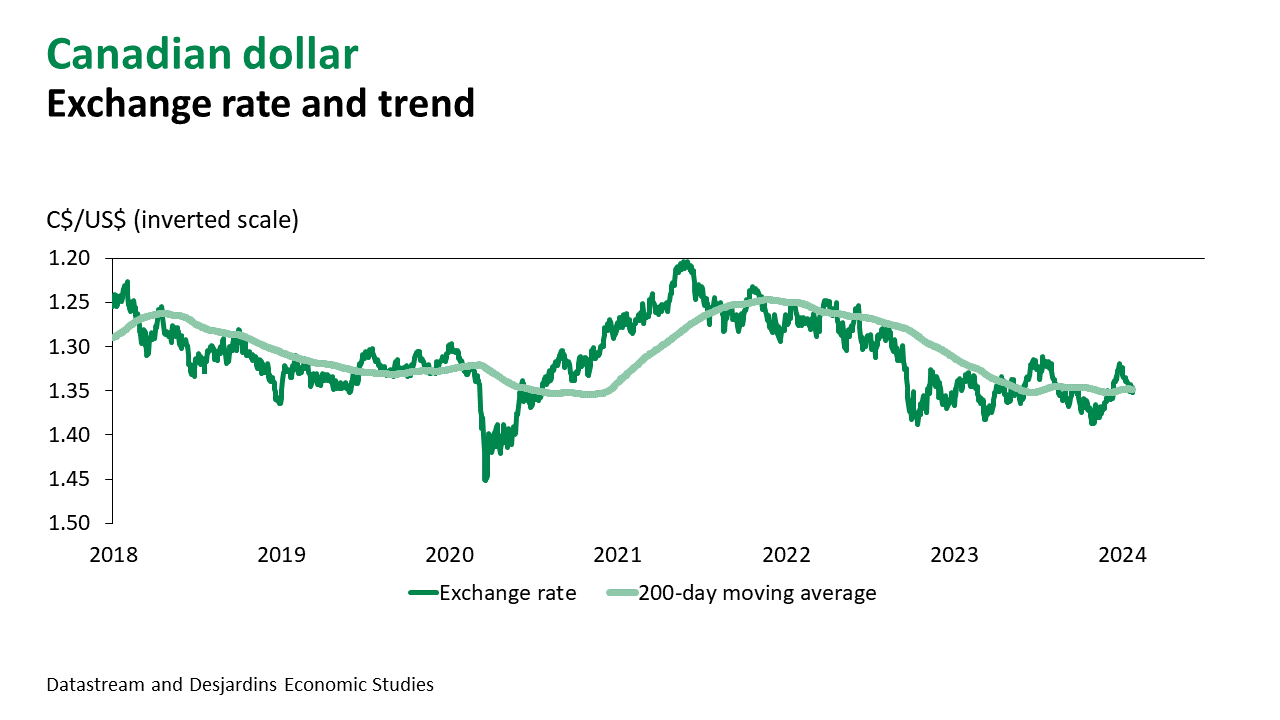

- Canada’s numbers were among those that disappointed, with several core inflation measures accelerating. All the same, the Bank of Canada adopted a more neutral tone at its January 24 meeting, bearing in mind that the Canadian economy has stalled. It closed the door to further rate hikes, which brought the loonie down a bit. The Canadian dollar had gained about 3% against the US dollar in the last weeks of December, before losing close to 2% in January.

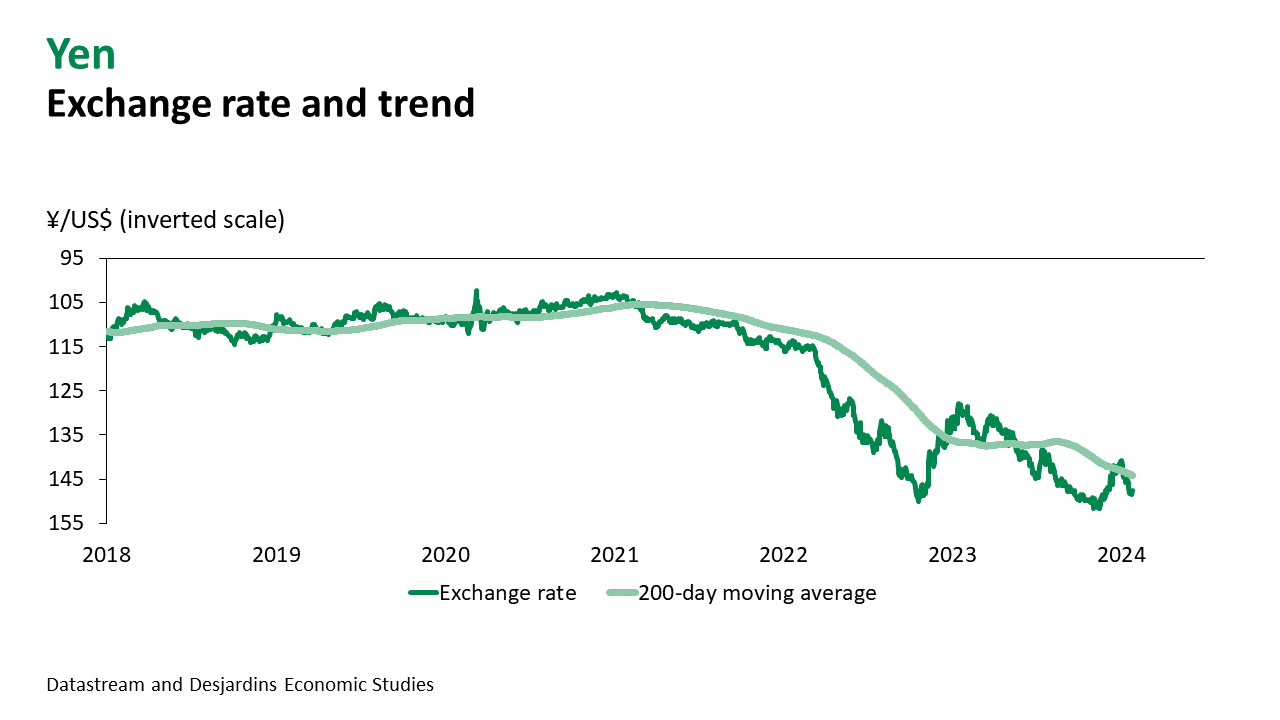

- It wasn’t the worst showing by a major currency, though. The yen had a rocky start to the year, falling nearly 5%. The currency remains hamstrung by the fact that the Bank of Japan (BoJ) has not yet begun to tighten its monetary policy, amid concerns that inflation will drop back below its target in the coming years. The BoJ has signaled that the annual wage negotiation results, which will be announced in April, could act as proof that their inflation target is attainable. This would then set the stage for monetary policy normalization.

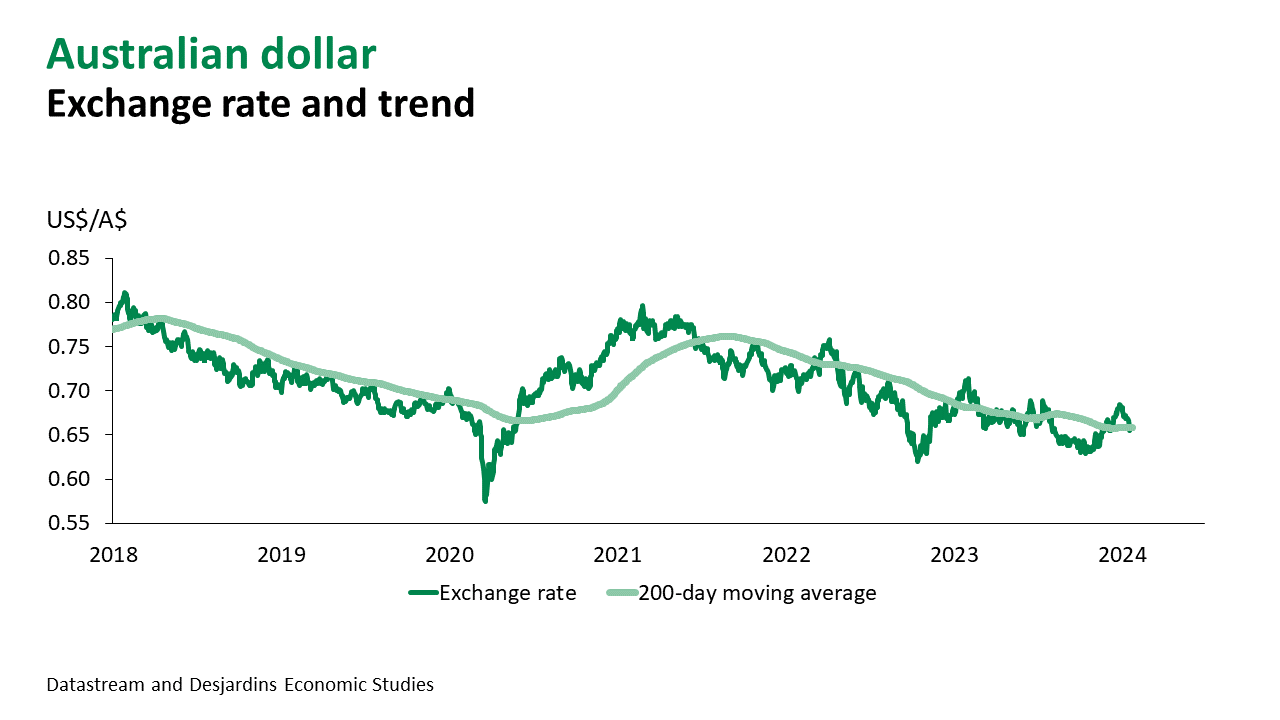

- The Australian dollar is also struggling, pulling back about 3% so far in January, in response to weaker commodity demand and fears of further economic deterioration in China. However, the announced reduction in the reserve requirement ratio for banks in China, which could stimulate credit, has revived some optimism.

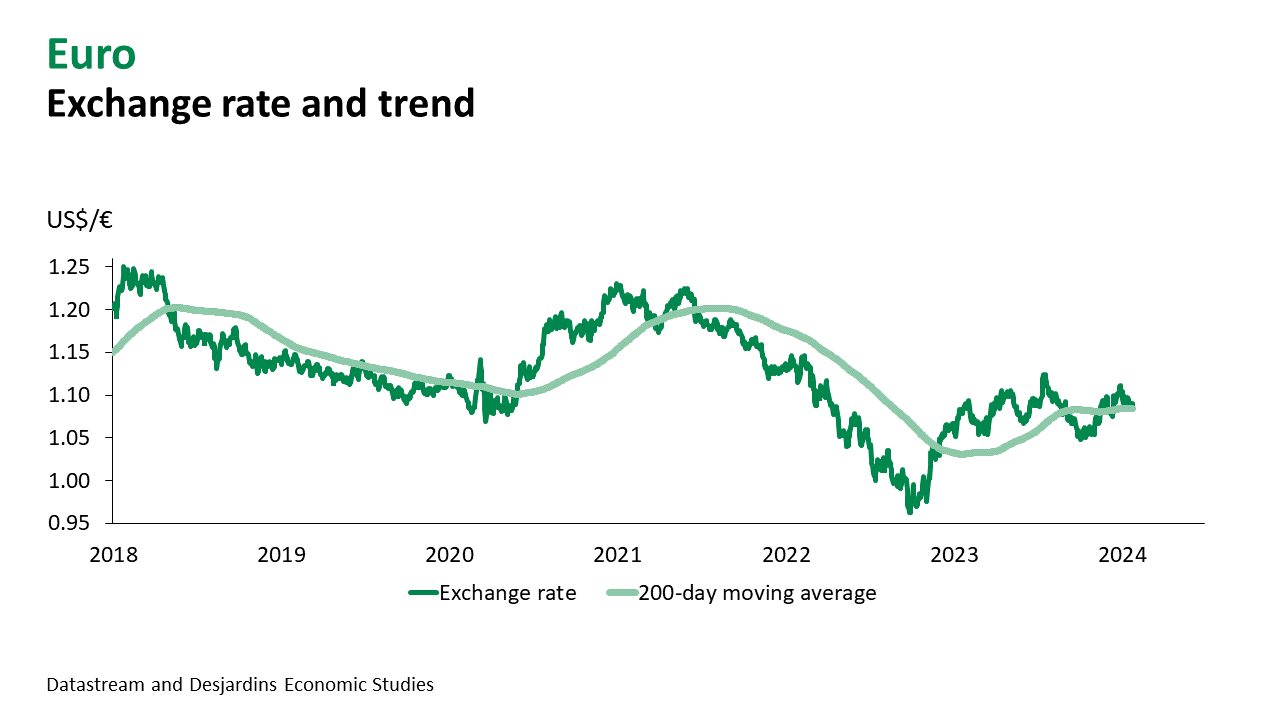

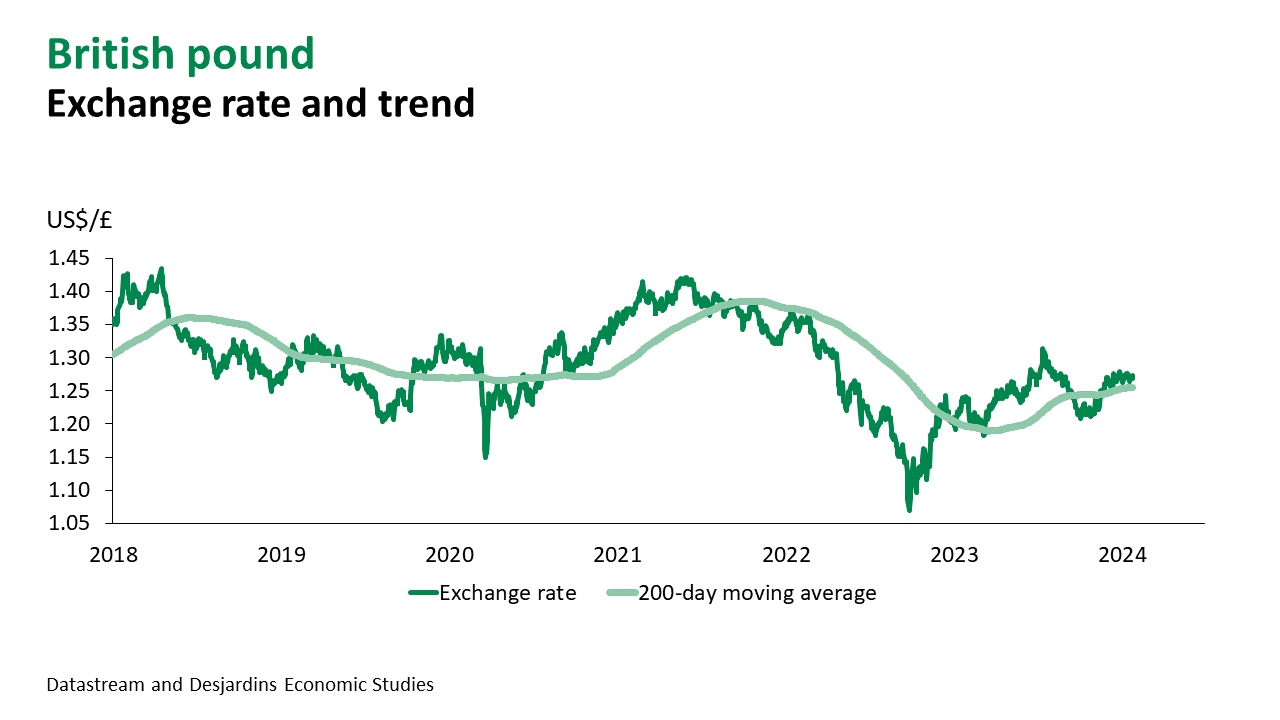

- On the European front, the pound has been remarkably resilient, holding strong at close to US$1.27. The most recent employment and inflation numbers surprised to the upside, suggesting that a rapid decline in key interest rates is unlikely. The euro depreciated slightly after hitting US$1.10. The eurozone economy continued to show signs of fragility. However, the European Central Bank remained cautious on inflation at its January meeting.

Main Factors to Watch

- Changing expectations for monetary policy could still shake up the currency market in 2024. In the short term, countries where key interest rates are lowed more quickly will see their currencies depreciate further. This may well be the case for the Canadian dollar.

- The economic situation and investor risk appetite will also bear watching. Some countries may experience greater difficulties in the months ahead. We’re still anticipating External link. This link will open in a new window. a mild recession in Canada, flat growth in Europe (though some countries could fall into a mild recession) and weak-but-positive growth in the United States.

- In the long term, rosier economic outlooks and greater risk appetite both suggest that many currencies will start to recover against the US dollar. However, the loonie’s potential for appreciation may be slightly lower, as we are not forecasting strong increases in commodity prices in 2025. Moreover, investors could still price in risks in the Canadian housing market, especially as mortgages continue to renew at elevated interest rates.

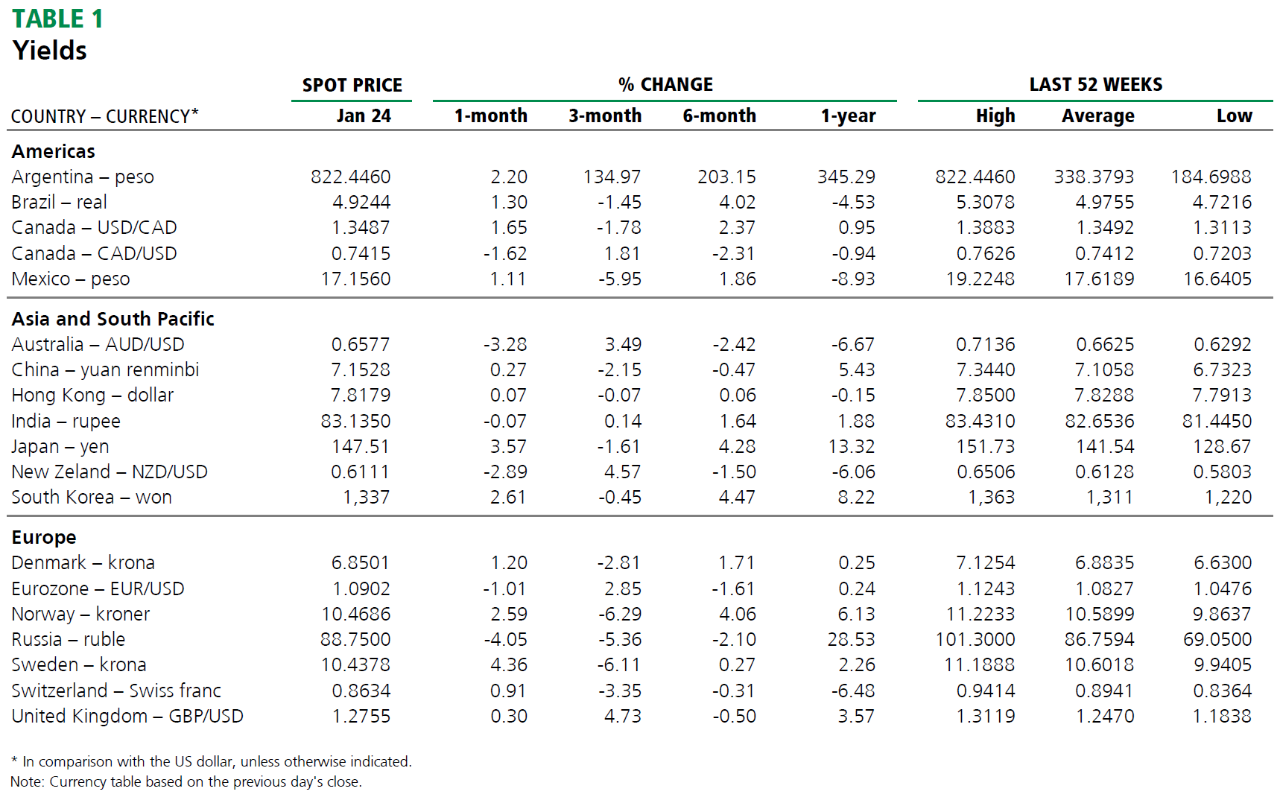

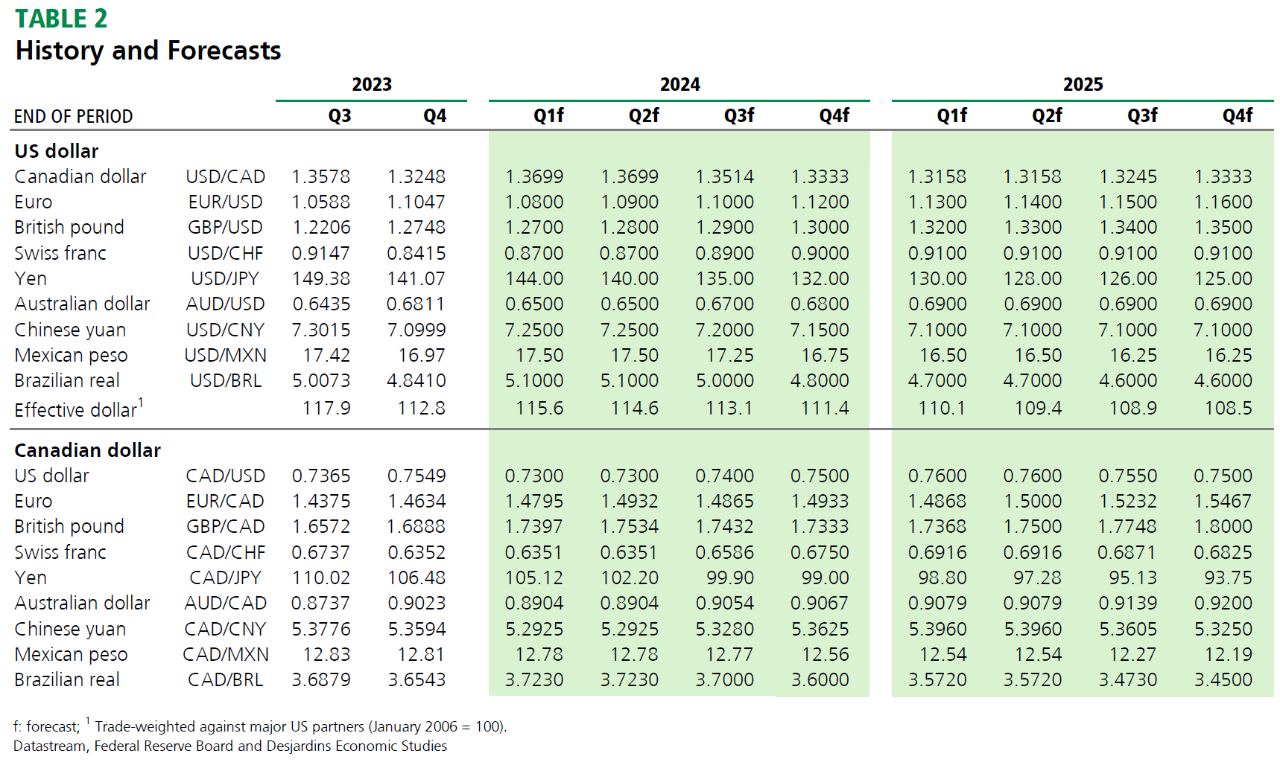

Main Exchange Rates

Currency Market