- Jimmy Jean, Vice-President, Chief Economist and Strategist • Hendrix Vachon, Principal Economist

FX Analysis

Synchronized Interest Rate Cuts Would Limit Volatility for a Number of Currencies

February 29, 2024

Highlights

- We’re not there yet, but we’re getting close! Spring is just around the corner, and this year we expect interest costs to melt away with the snow, or soon after. For many currencies, the worst-case scenario would be rate cuts starting in the second quarter while the Federal Reserve (Fed) continues to hold amid a still-hot US economy. In this scenario, the US dollar would benefit from more favourable interest rate spreads and likely be considered a safe haven as economic conditions outside the United States remain more challenging. This explains why exchange rates continue to be highly volatile in response to key US data releases.

- In February, all eyes were on the US inflation rate, which slowed less than expected. On top of that, job creation held steady, with few signs of wage moderation. But it hasn’t been all roses for the US economy since the beginning of the year. Retail sales, industrial production and housing starts have all slowed. The cumulative effect on the effective US exchange rate was a slight appreciation in February, following more substantial gains in January.

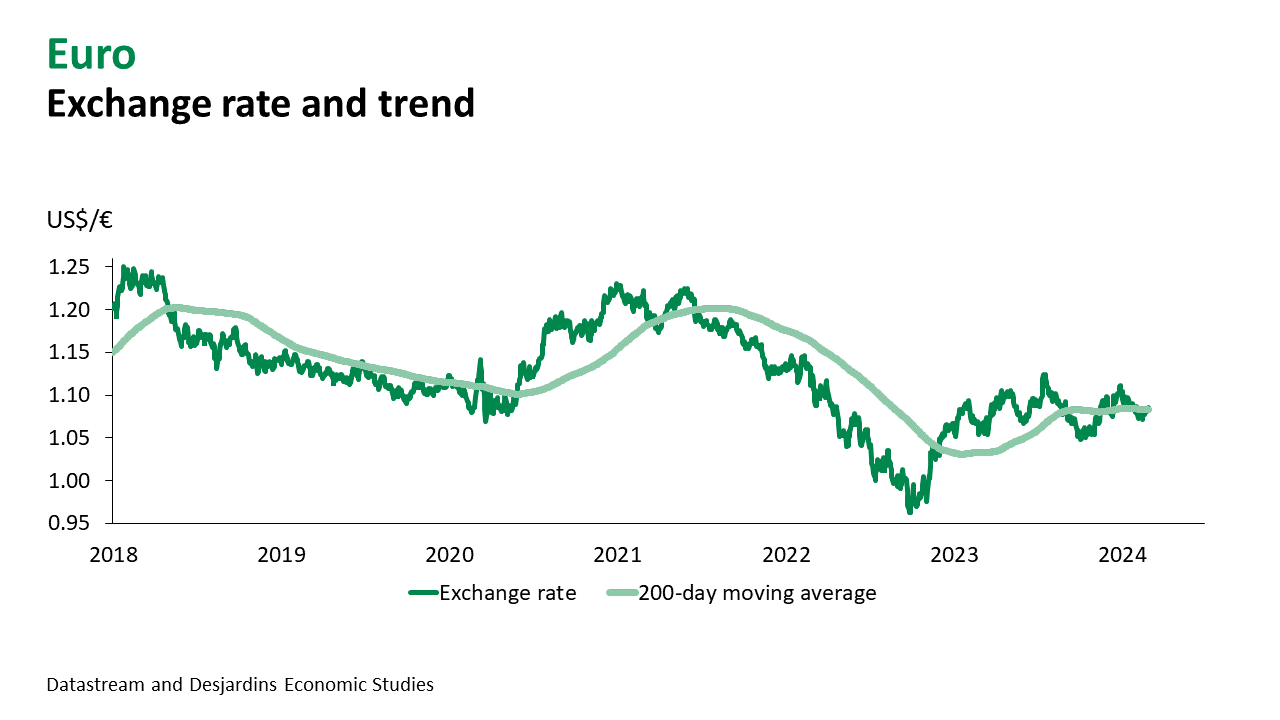

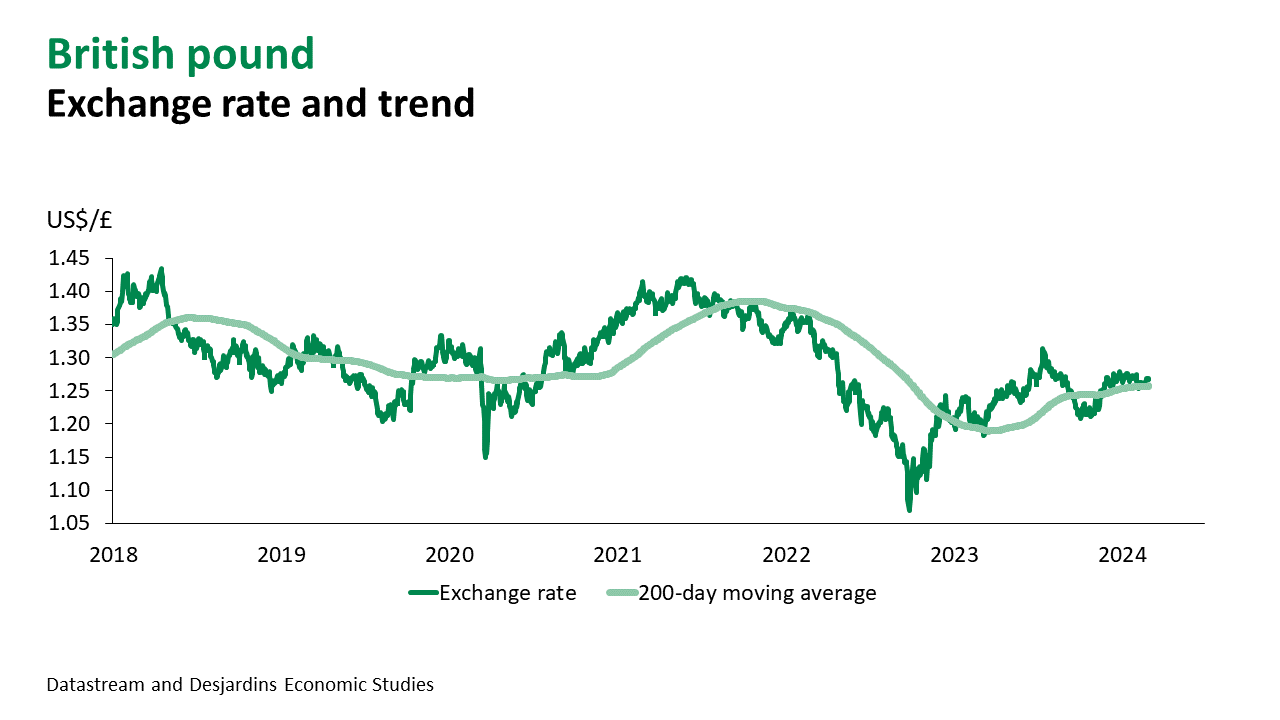

- In Europe, a few countries have officially fallen into a recession after posting at least two consecutive quarters of negative real GDP growth. The United Kingdom is among those now grappling with a recession. At the same time, its inflation rate continues to ease. The pound fell below US$1.26 a few times in February. The eurozone economy remains fragile, which is helping bring down inflation. The annualized 3-month change in core inflation, which strips out food and energy, stands at 2%. The common currency hovered around US$1.08 in February, dipping to a low of US$1.07 mid-month after US inflation figures were released.

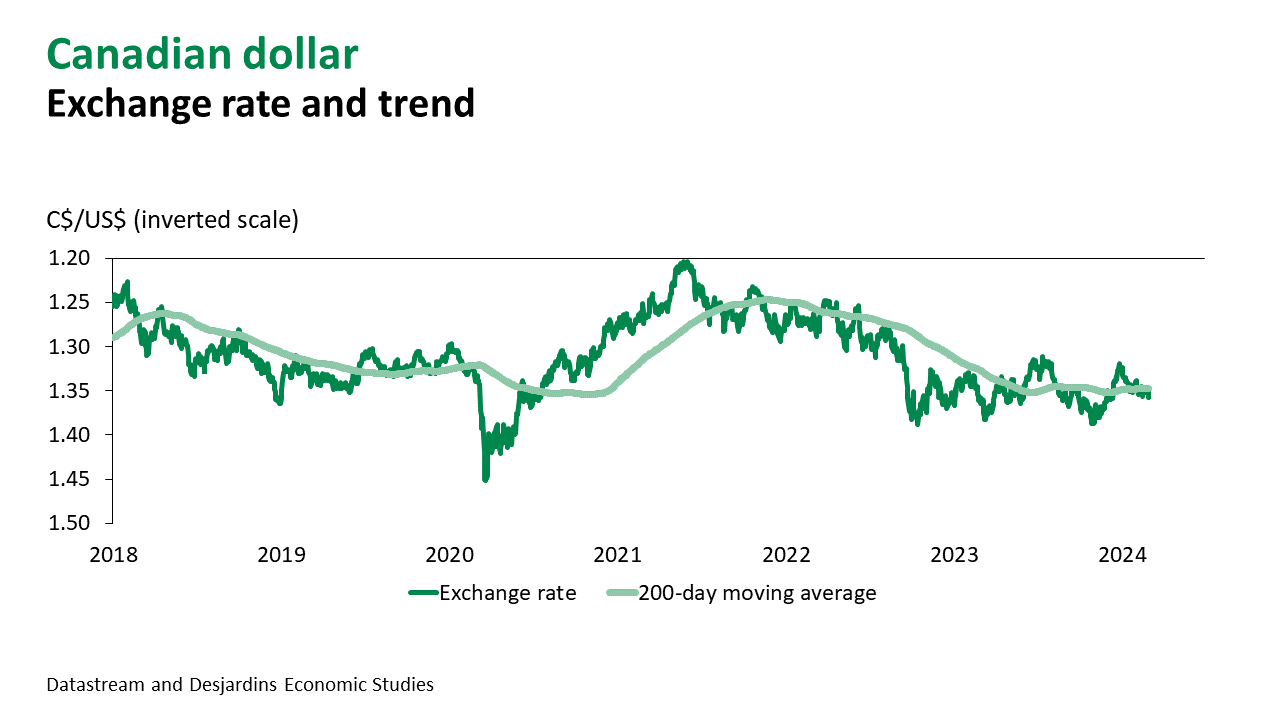

- The Canadian dollar traded around CAN$1.35/US$ (US$0.74). In Canada, inflation surprised to the downside, unlike in the US. But other data suggests the Canadian economy is still growing, which could delay a sustainable return to the inflation target. The Bank of Canada expected the economy to stagnate at the end of 2023, but instead real GDP grew 1.0%. The housing market has also shown signs of a rebound.

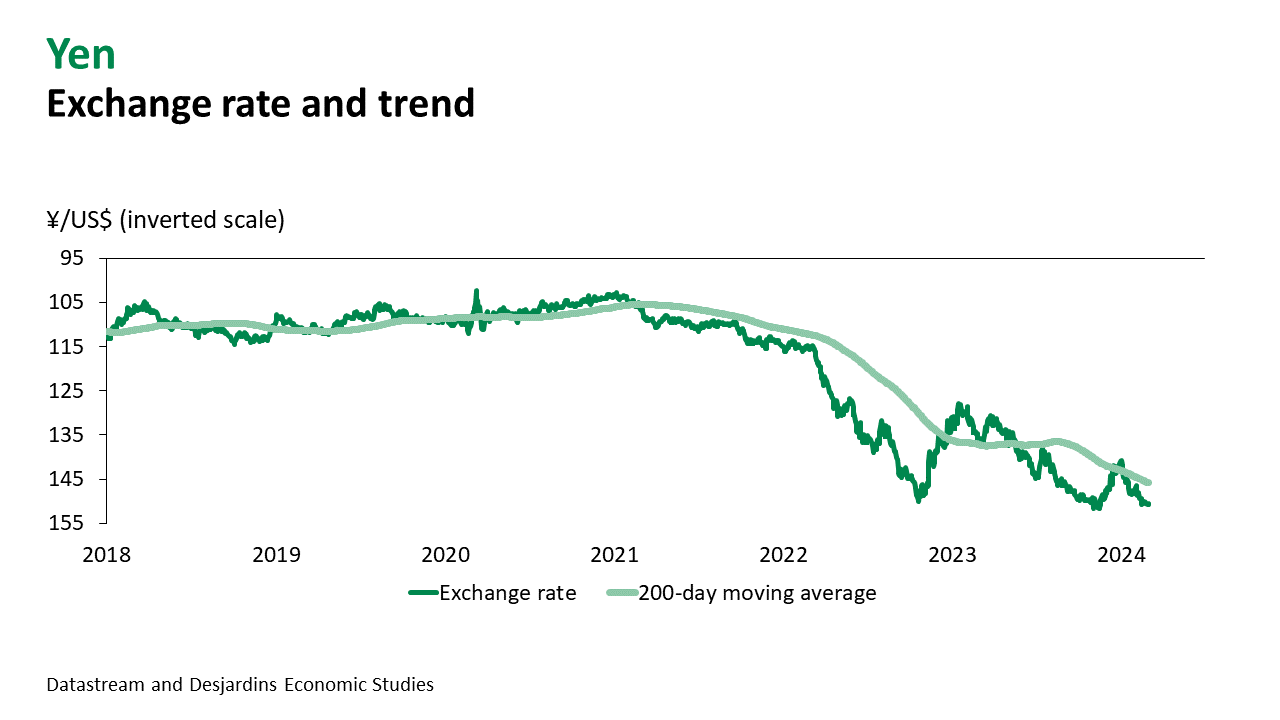

- The Japanese yen remains under pressure. Its exchange rate pushed above ¥150/US$ in recent weeks. Japan’s real GDP contracted for the second consecutive quarter, seeding doubt about the Bank of Japan’s ability to start raising interest rates this spring. We’ll be paying close attention to wage negotiations at major Japanese companies. Significant wage growth again this year would likely spell the end of the country’s negative interest rate policy and help narrow the gaping interest rate spread with the US.

Main Factors to Watch

- Changing expectations for monetary policy could still shake up the currency market in the short term. Currencies could weaken in the countries expected to introduce rate cuts first.

- However, our baseline scenario sees the major central banks cutting key rates on roughly the same timeline in 2024. Right now, the Fed appears most likely to hold off on rate cuts, but we expect US economic data to continue moderating over the short term. The Fed also seems willing to do everything in its power to avoid a hard landing. After all, the Fed has a dual mandate: price stability and maximum employment. Finally, since it’s an election year in the US, the Fed may not want to make a stir by unnecessarily slowing the economy. It therefore seems unlikely the Fed will put off rate cuts for a lot longer than other major central banks in 2024.

- We expect the Canadian dollar to continue trading around CAN$1.35/US$ (US$0.74) in the coming months. It should bounce back a little once the global economy picks up in the second half of the year and in 2025 and as commodity prices start rising.

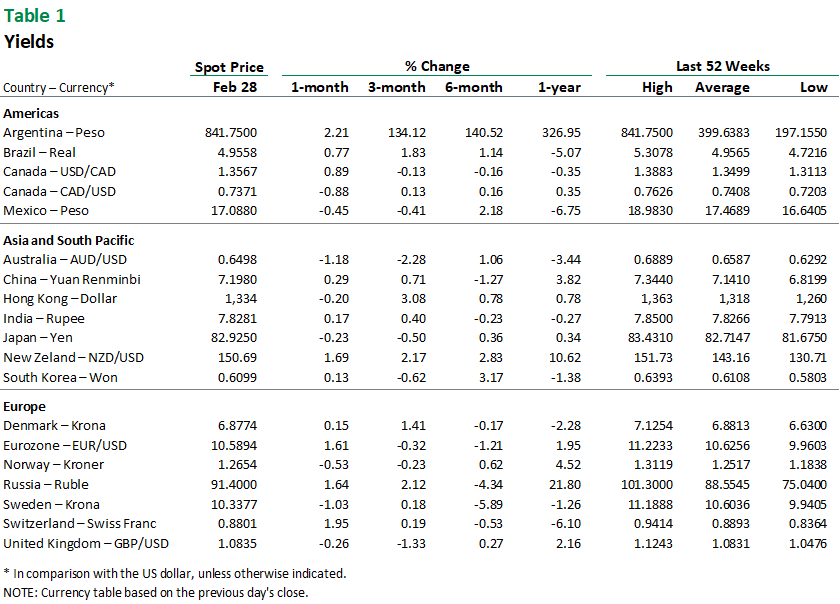

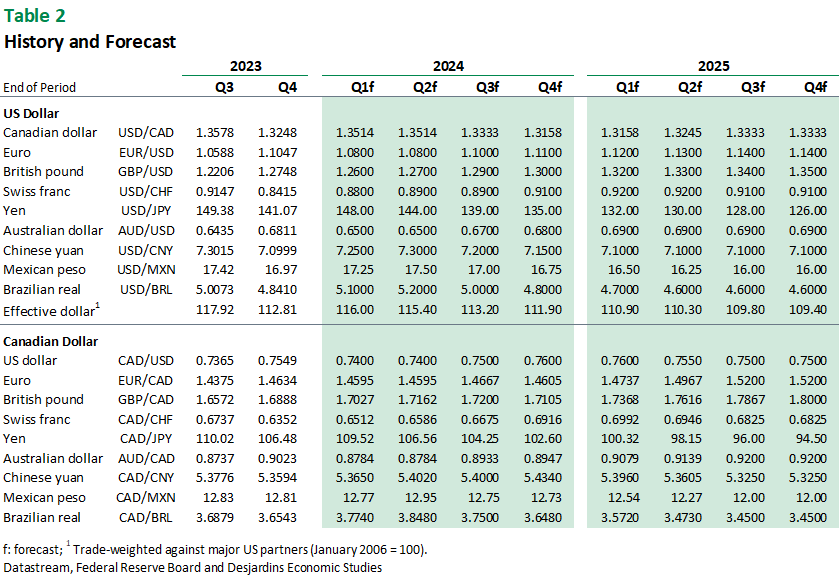

Main Exchange Rates

Currency Market