- Jimmy Jean, Vice-President, Chief Economist and Strategist • Hendrix Vachon, Principal Economist

FX Analysis

After a tough April, many currencies could continue to struggle in May and June

April 26, 2024

Highlights

- US interest rates resumed their upward climb in April, giving the US dollar an edge over several other currencies. One of the contributing factors was the lack of progress on inflation numbers, which were published on April 10. It’s becoming increasingly clear that the Federal Reserve (Fed) is headed down a different path than most other major central banks. Unless the next US data releases point to an abrupt turnaround, the Fed will almost certainly decide to wait a while longer before cutting interest rates.

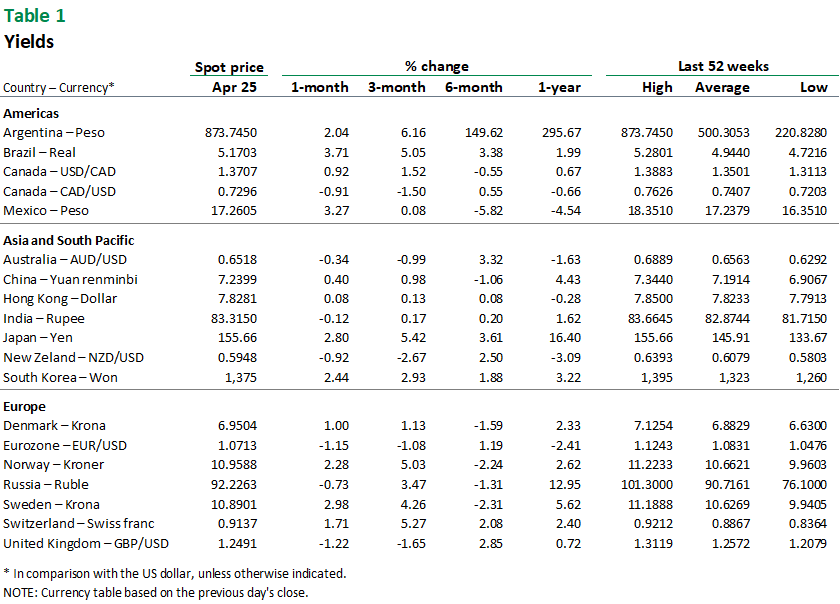

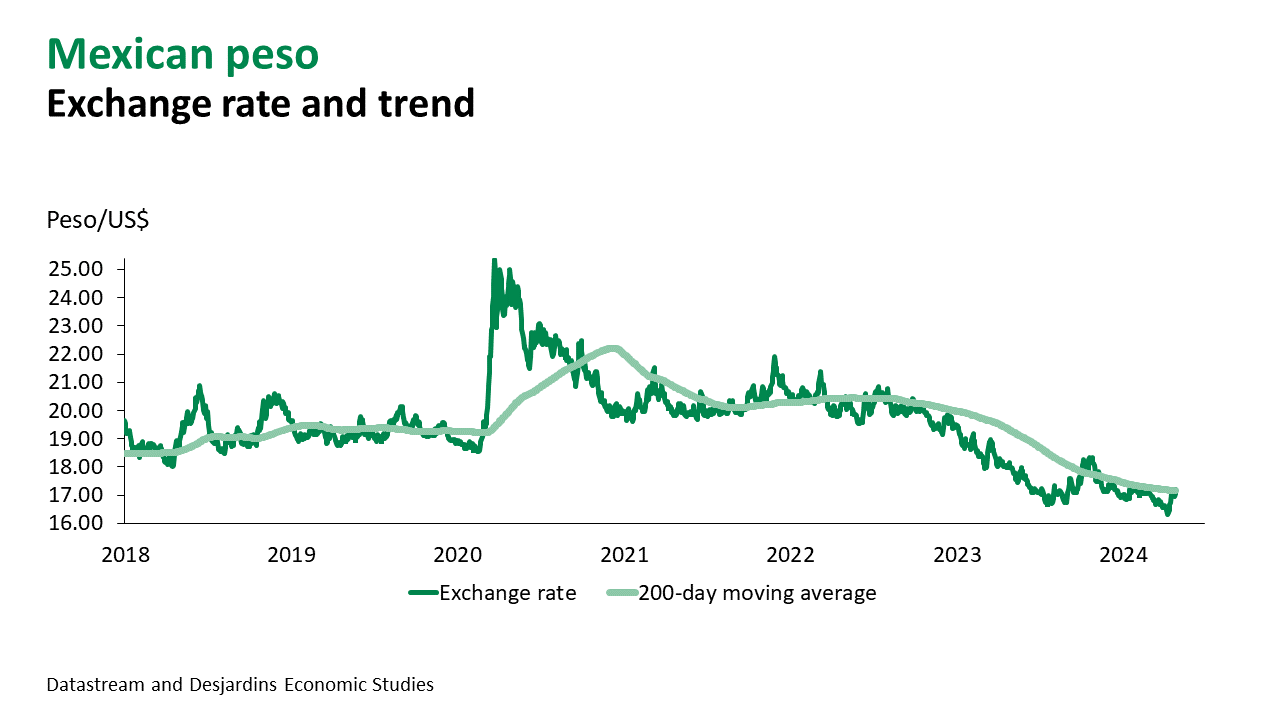

- Emerging market currencies experienced the biggest losses. The rise in US interest rates has added another layer of financial stress for many of these countries since they typically borrow in US dollars. Mexico and Brazil were among those that saw their currencies depreciate the most. The fact that both countries’ central banks have already started lowering their key interest rates added to the downward pressure on these currencies. Considering that Mexico’s key rate is 11% and Brazil’s is 10.75%, there is plenty of room left to cut rates.

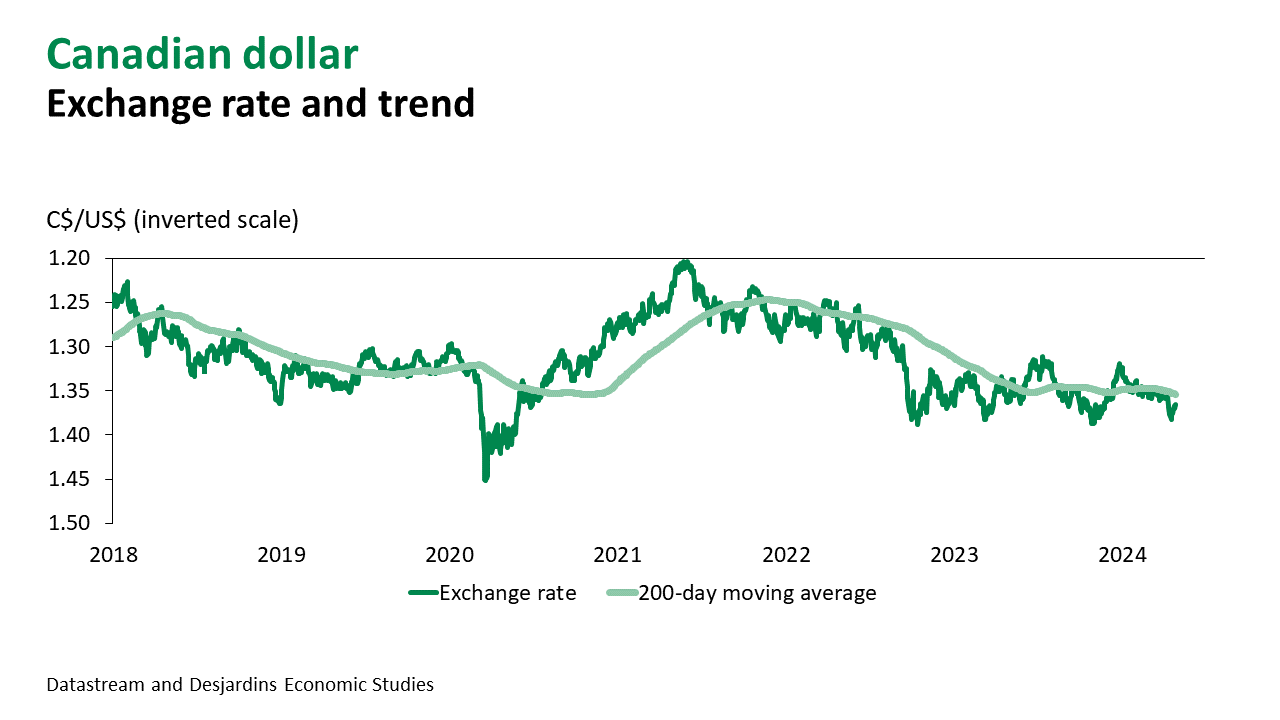

- The Canadian dollar lost just over 1% in April, though at one point during the month it was down more than 2%. Investors still aren’t betting on Canada’s monetary policy diverging significantly from the US’s, but the Bank of Canada (BoC) has good reasons to start cutting rates sooner. Several inflation measures have come down and are unlikely to rise again given that the Canadian economy has slowed considerably. That said, the BoC won’t be able to blaze ahead with several rate cuts while the Fed stands pat. Doing so would send the Canadian dollar plunging too low, which in turn would drive up import prices and feed inflation.

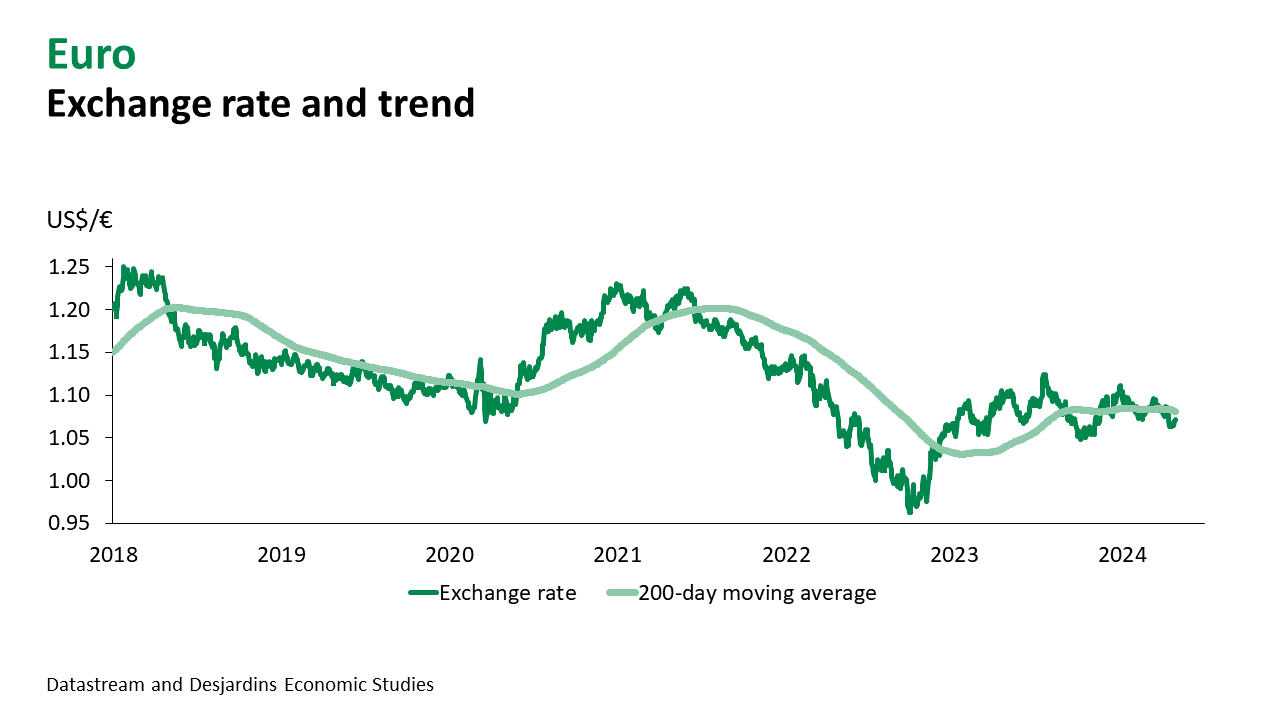

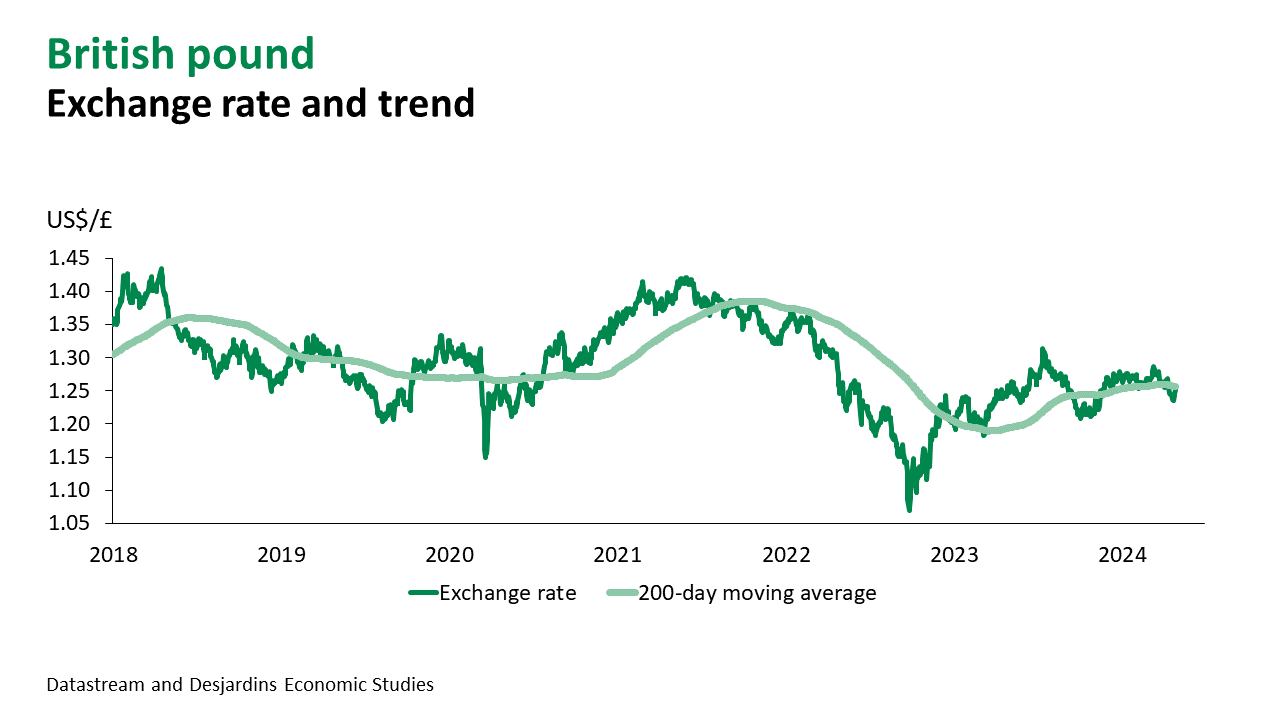

- Investors are more convinced that eurozone key rates will start coming down in June. There has been considerable progress on inflation and the region’s economy clearly remains in disinflationary territory. Even though some economic indicators have improved recently, they still fall shy of signalling a rapid return to normal levels of economic growth. The euro started April trading at US$1.08, but then it slumped to nearly US$1.06. Across the Channel, the pound weakened relative to the euro as the United Kingdom’s unemployment rate edged up 0.3%. There too, inflation continued its downward trend, but it still may not be enough to convince the Bank of England to start cutting interest rates in June.

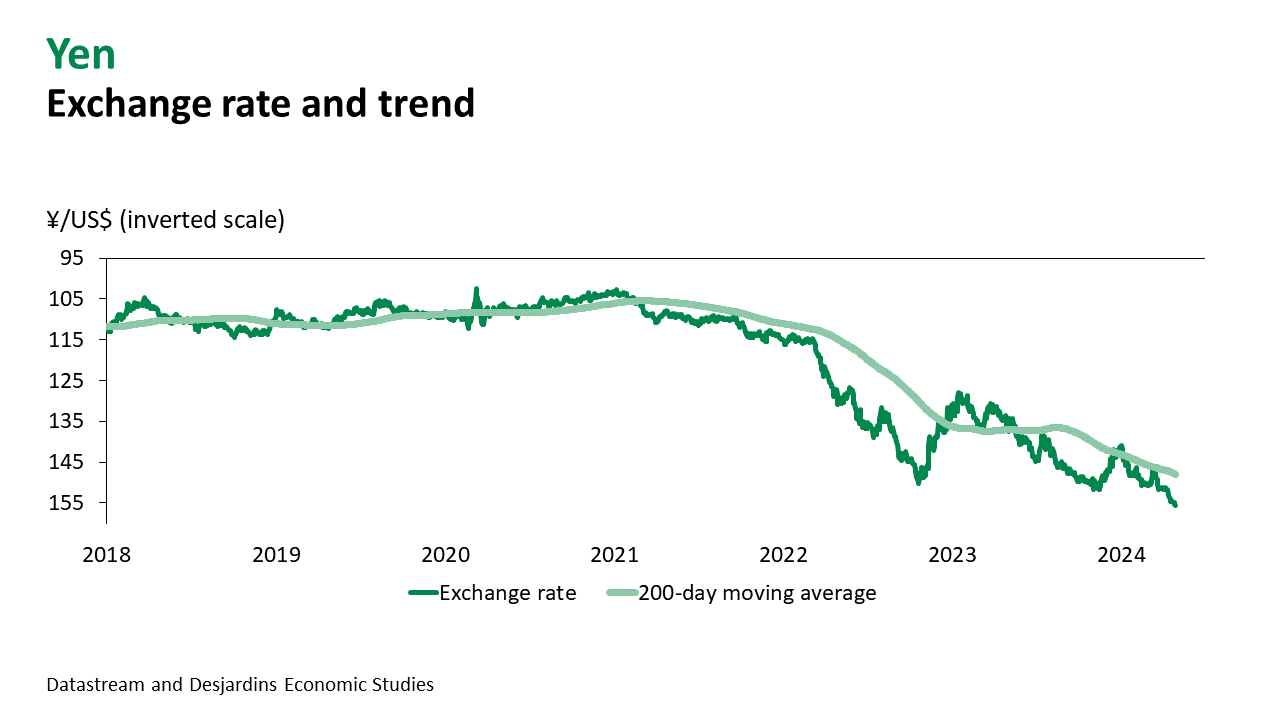

- The yen lost another 3% in April despite the fact that the Bank of Japan ended its negative interest rate policy. Since the potential for rate increases in Japan remains limited, the spread with US rates has widened. With Japan’s currency now trading at ¥156/US$, many speculators believe the country will soon start selling off its foreign exchange reserves in a bid to lift the yen.

Main Factors to Watch

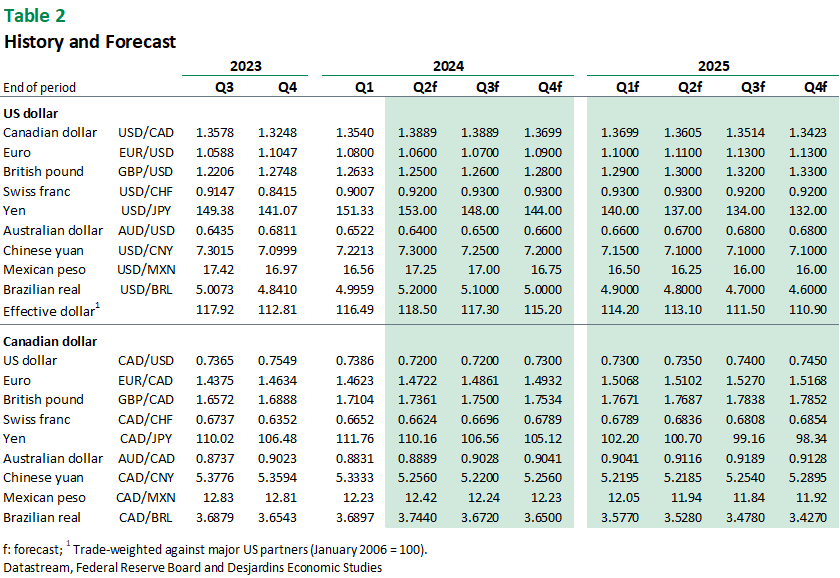

- May and June will likely look a lot like April. Changing monetary policy expectations will likely continue to shake up the currency market. We now believe the Fed will wait until the fall before it makes an initial rate reduction. Before that can happen, both inflation and the US economy have to cool enough to convince the central bank. Once US rate cuts look more probable, the greenback could start trending downward again relative to several other currencies. More generally, we don't expect there to be a marked slowdown in global economic growth, and therefore we don't anticipate investors flocking to safe-haven assets and driving up the US dollar.

- The Canadian dollar will likely continue to slide over the next few months. We expect the BoC to announce two rate cuts—one in June and another in July—before the Fed starts its monetary easing in the fall. In the coming months, there's a good chance the Canadian dollar will approach CA$1.40/US$. However, the loonie could start recovering before the fall in anticipation of US rate cuts.

Main Exchange Rates

Currency Market