- Randall Bartlett

Senior Director of Canadian Economics

Essentials of Monetary Policy

The Bank Plays Coy on the Timing of Future Rate Cuts

March 6, 2024

According to the BoC

- As was widely expected, the Bank of Canada kept the overnight policy rate unchanged today at 5.00%, matching every decision since September 2023.

- According to Governor Macklem in his Press Conference Opening Statement, “[t]oday’s decision reflects Governing Council’s assessment that a policy rate of 5% remains appropriate. It’s still too early to consider lowering the policy interest rate.”

- While much of the language remained unchanged from the prior rate announcement, there was some softening in the Bank of Canada’s tone on the margins. The Bank emphasized that underlying price pressures persist. But in recognizing that “year-over-year and three-month measures of core inflation are in the 3% to 3.5% range, and the share of CPI components growing above 3% declined but is still above the historical average,” it also tacitly acknowledged that progress is being made on inflation. But “the path back to our 2% target will be slow, and progress is likely to be uneven.”

- Looking to the broader economy central bankers said, “demand pressures have eased, and the economy now looks to be in modest excess supply.” Further, [l]abour markets have continued to ease gradually.” But “with the labour market coming into better balance, we are looking for further evidence that wage growth is moderating.”

- Governing Council “is still concerned about risks to the outlook for inflation, particularly the persistence in underlying inflation… [It] wants to see further and sustained easing in core inflation and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour.”

- The Bank is continuing its policy of quantitative tightening, with no new information provided.

Implications

We weren’t at all surprised by the slight shift in the Bank of Canada’s tone today. As our Macro Strategy team highlighted earlier in the week, there are plenty of reasons for the Bank to stay on hold but begin waxing dovish.

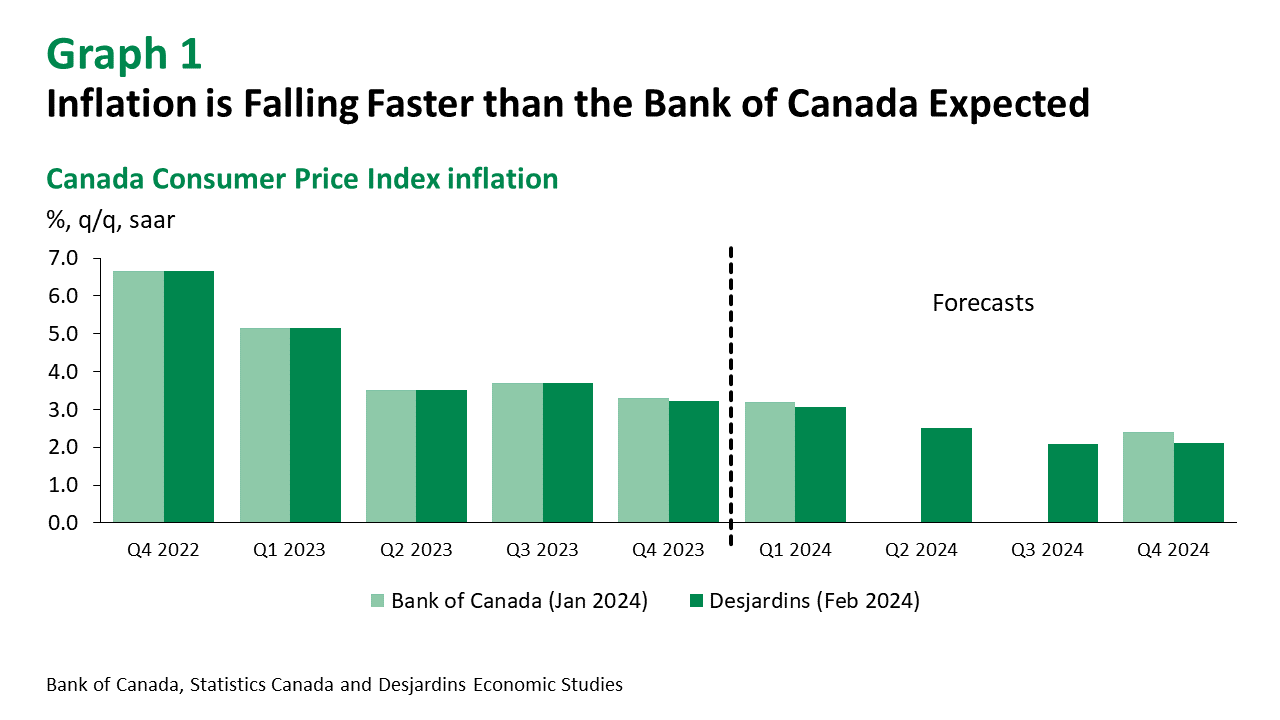

Most importantly, inflation is coming in below the Bank of Canada’s forecast in the January 2024 Monetary Policy Report (MPR)—a trend that we think is set to continue (graph 1). Indeed, at this point, the primary driver of headline inflation is the shelter component, and within that mortgage interest cost reflecting the elevated level of interest rates. As the Bank begins to cut rates, further pressure will start to come off this key driver of price growth. Our Macro Strategy team has also pointed out that the measures of core inflation preferred by the Bank of Canada—trimmed mean and median—are subject to substantial bias when the distribution of price growth is highly skewed as it is now. As such, correcting for the bias suggests core inflation is below 3%, putting it within the Bank’s 1% to 3% operating range.

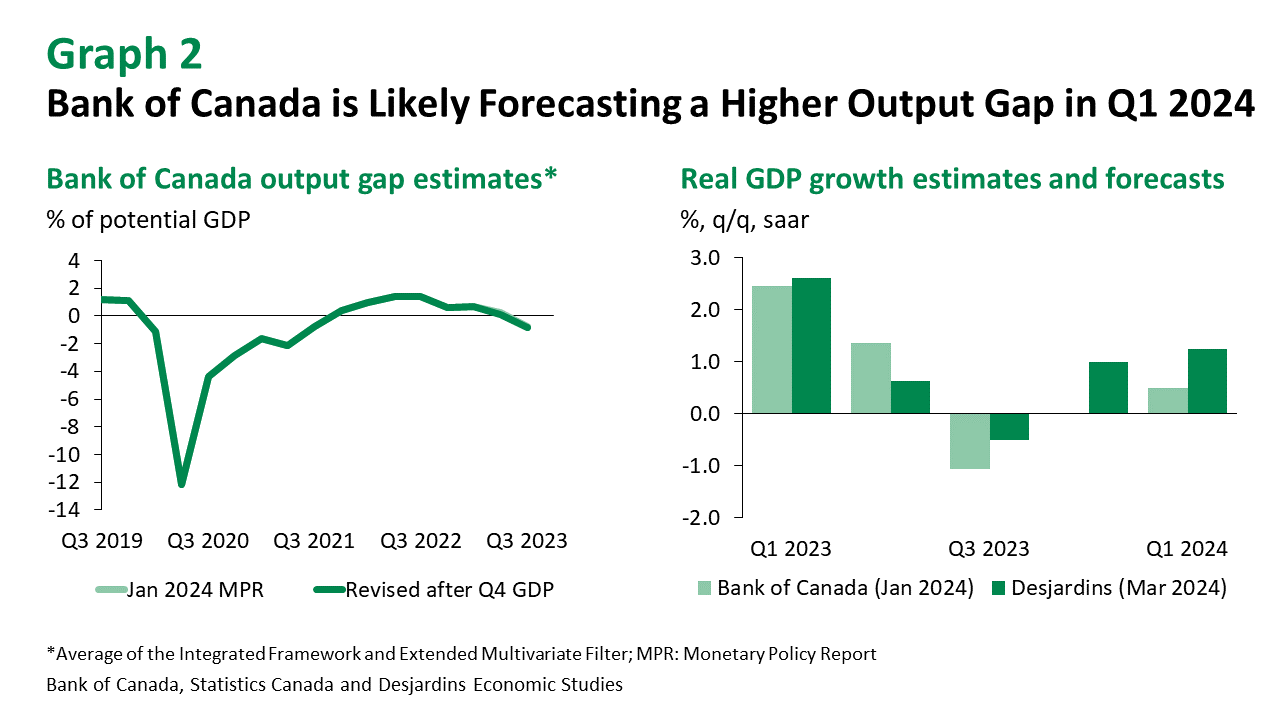

Growth is providing a more mixed picture, with output having topped the Bank of Canada’s estimates and forecasts in the second half of 2023 (graph 2). But the details under the hood of the latest real GDP release painted a bleaker picture of the state of the Canadian economy than the headline would suggest. Final domestic demand contracted for the first time since 2022. In fact, if it wasn’t for surging exports, real GDP growth would have looked a lot worse than it did. As such, while Canada may have avoided a recession in 2023, there wasn’t much else to celebrate in the Q4 data.

Looking ahead, growth is tracking above the Bank’s forecast for Q1 2024 real GDP growth as well. As a result, the Bank of Canada is likely to revise up its real GDP growth and output gap forecast for 2024. But this weak growth outlook would lead to further excess slack in the economy, thereby applying additional downward pressure on price growth. And weakness is likely to persist throughout the first half of year, matching the weak consumer and business survey data to date. This was illustrated most clearly by the surge in business bankruptcies observed in January.

Taken together, while the Bank of Canada may not have been prepared to fully commit to rate cuts at this meeting, by recognizing the progress made, it is setting the stage for cuts to come. We continue to be of the view that the Bank will begin cutting interest rates at its June meeting.

2024 Schedule of Central Bank Meetings