- Marc-Antoine Dumont, Senior Economist • Florence Jean-Jacobs, Principal Economist

Commodity Trends

Monthly Update: OPEC+ Cuts Production Again

December 7, 2023

Highlights

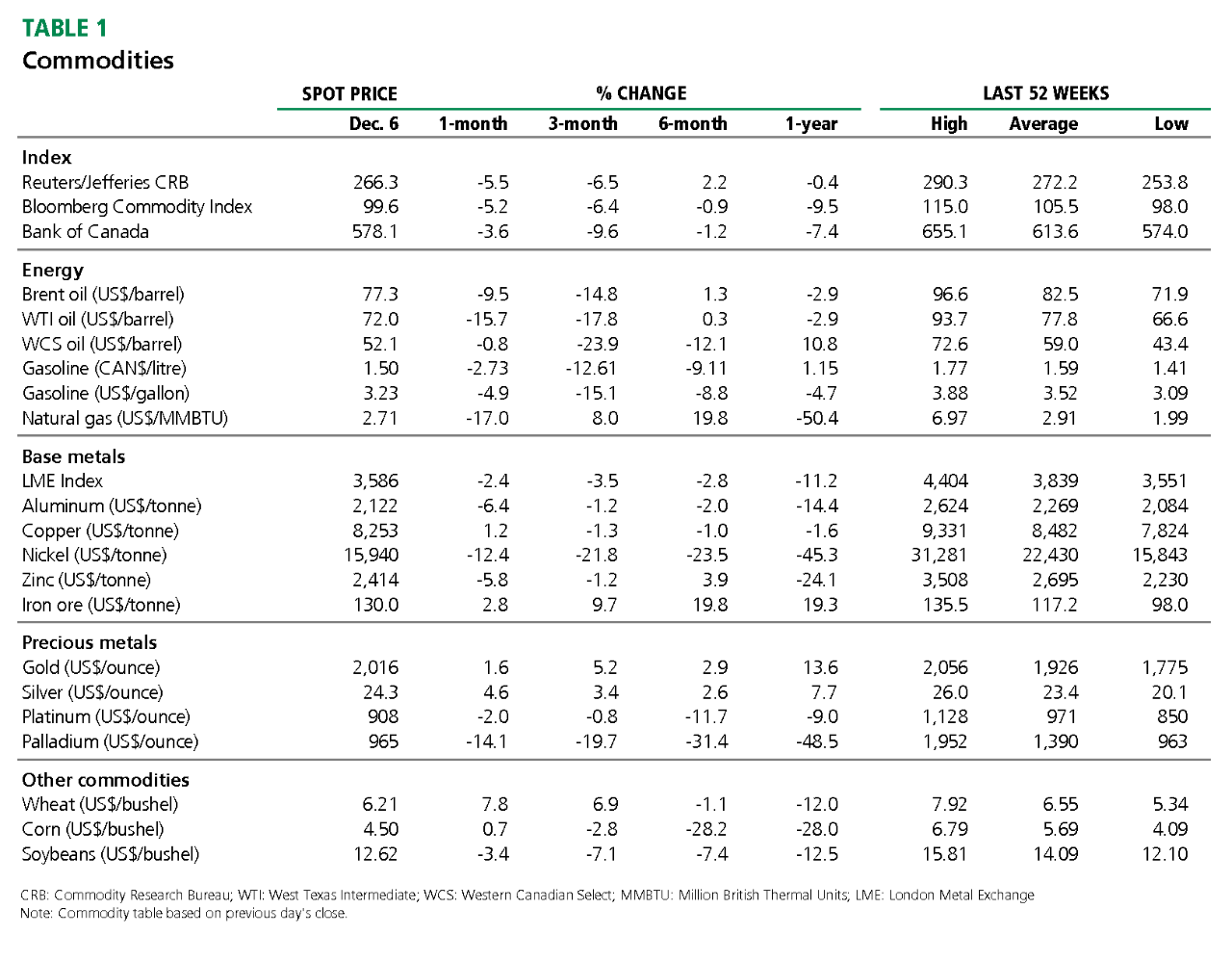

- The Organization of the Petroleum Exporting Countries and its partners (OPEC+) cut production again, by 2 million barrels per day (MMb/d). Each member will have to decide how much they'll contribute to this goal. This latest voluntary cut means that OPEC+ has reduced its production target by 7 MMb/d—or 7% of global oil supply—in just under 2 years. If these cuts materialize fully and no member backs out, it could prevent the market from reaching a surplus in early 2024. That said, the cartel's announcement was accompanied by a drop in oil prices, indicating that the markets aren't confident that the members will comply with this agreement.

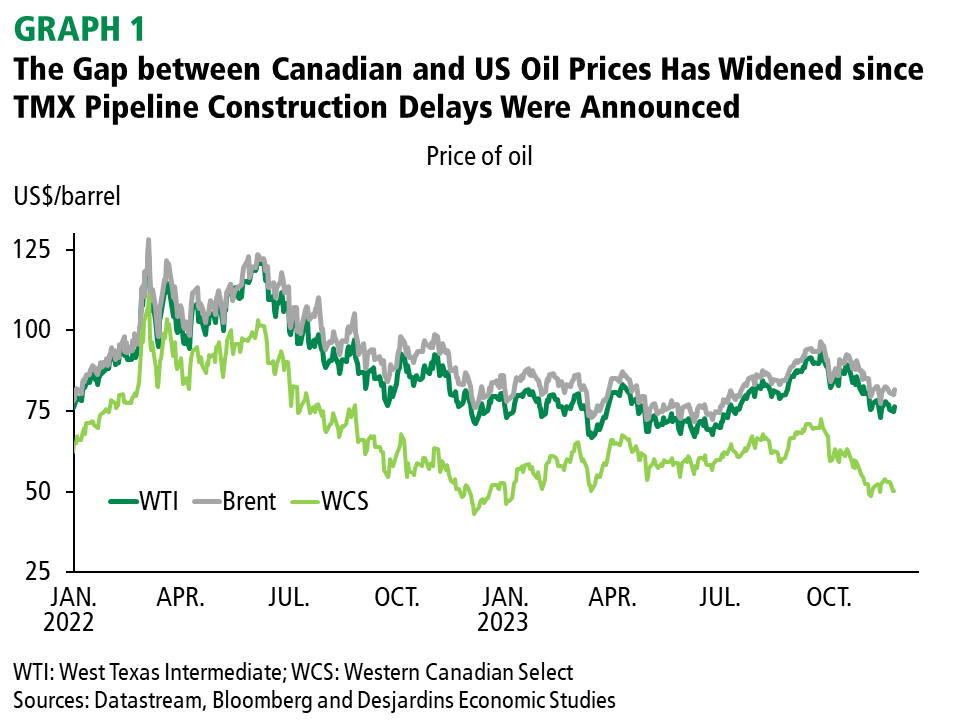

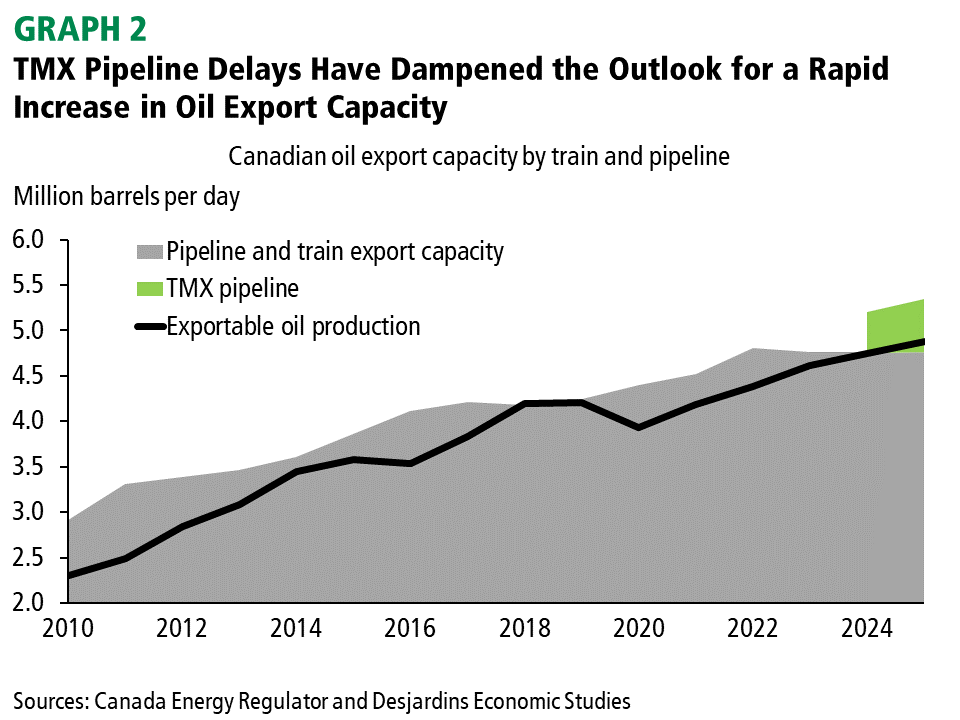

- The spread between West Texas Intermediate (WTI) and Western Canada Select (WCS) rose above US$28 per barrel—its widest level since December 2022—due to the maintenance period in the US, higher Canadian production, and delays to the TMX pipeline construction. We don't expect to see the gap narrow until Canada's export capacity increases once the TMX pipeline comes online in the spring.

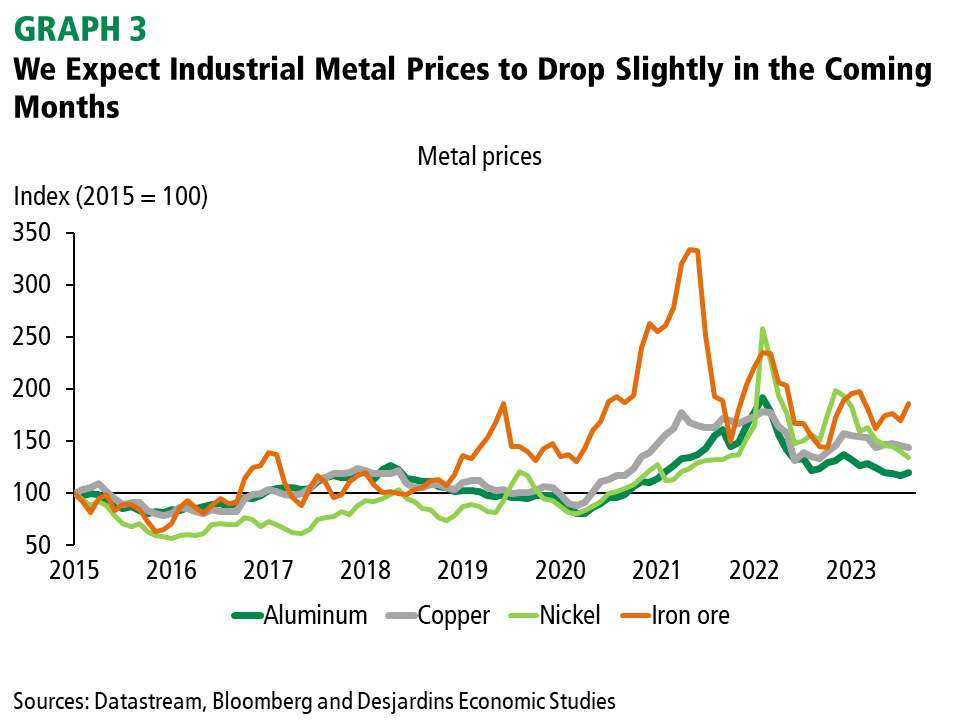

- Iron prices rose above US$130 per tonne in response to a possible rebound in the Chinese property market. Although the rebuilding in recently flooded Chinese regions will underpin demand somewhat, other fundamentals point to a slight decline in prices. Surprisingly, nickel prices fell faster than expected, given the more pessimistic short-term demand outlook.

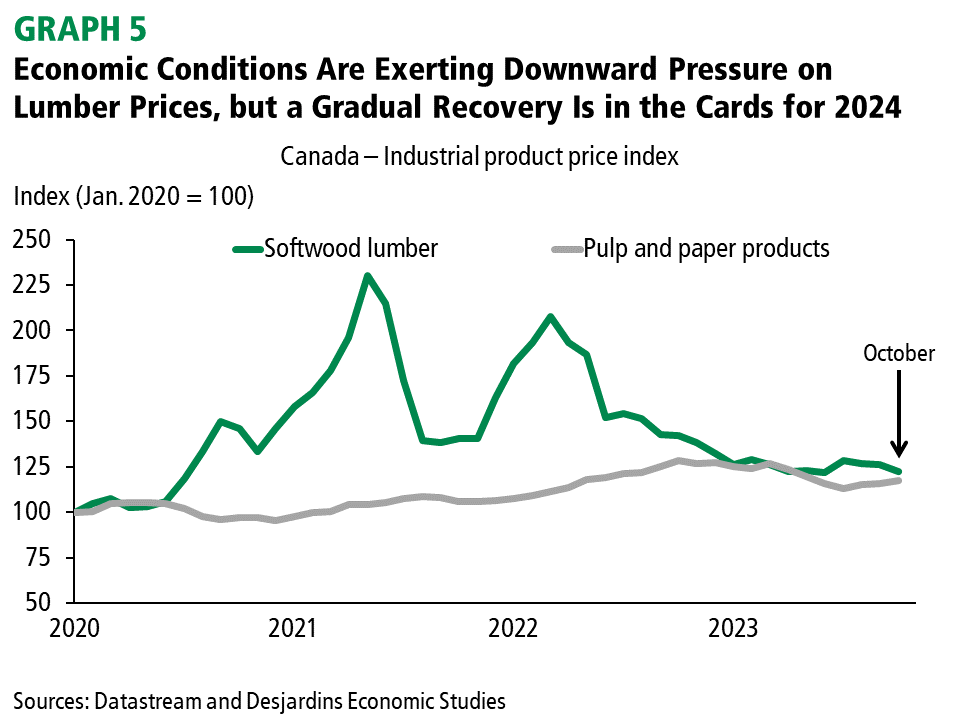

- Lumber prices remain relatively low due to the economic environment but are expected to rise in 2024.

- The Saint Lawrence Seaway strike ended in less than two weeks, so any serious disruption to Canada's grain supply chain was avoided. Grain prices are expected to stabilize as global supply and demand seem to be more balanced. Wheat supply exceeded expectations, which put a dent in prices recently. However, demand—especially from China—is likely to boost prices in the months ahead. Corn prices may have bottomed out, while the price of soybeans is likely to rise in 2024 due to adverse weather in Brazil.

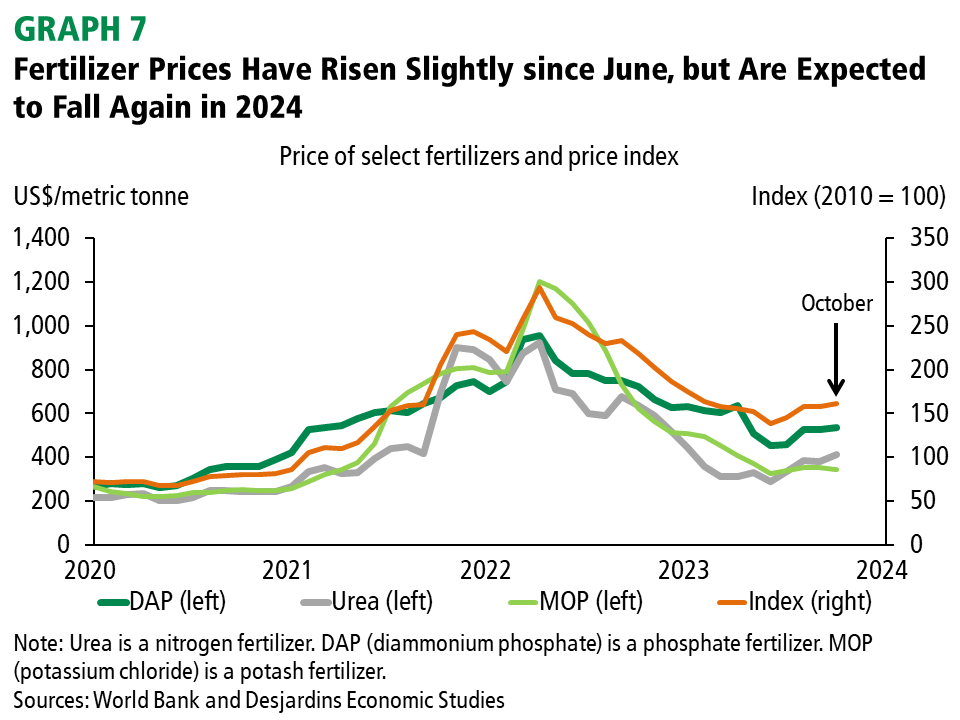

- Fertilizer prices have risen slightly since June but remain well below last year's record highs. Increased supply is also expected to drag prices down in 2024, barring an unexpected shock involving natural gas, which is a key input for nitrogen fertilizers. The conflicts in Ukraine and the Middle East pose upside risks to grain and fertilizer prices and could generate volatility.

Main factors to watch

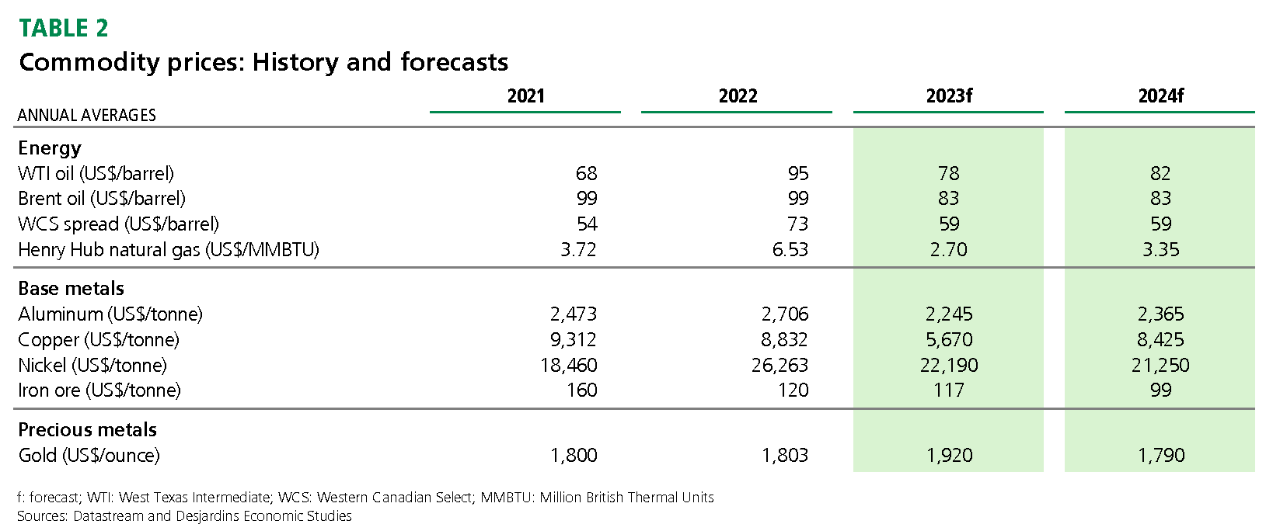

- Energy: 2023 year-end target revised down.

- Industrial metals: Price of nickel revised down and price of iron revised up to reflect higher demand.

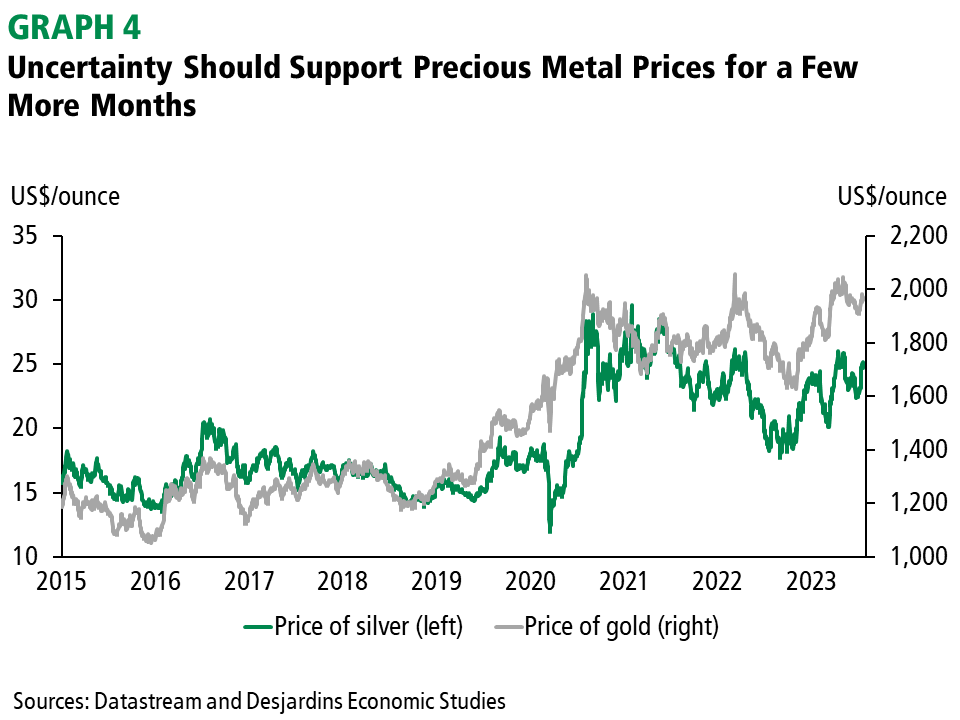

- Precious metals: No change.

Jimmy Jean, Vice-President, Chief Economist and Strategist • Marc-Antoine Dumont, Economist • Florence Jean-Jacobs, Principal Economist

NOTE TO READERS: The letters k, M and B are used in texts and tables to refer to thousands, millions and billions respectively. IMPORTANT: This document is based on public information and may under no circumstances be used or construed as a commitment by Desjardins Group. While the information provided has been determined on the basis of data obtained from sources that are deemed to be reliable, Desjardins Group in no way warrants that the information is accurate or complete. The document is provided solely for information purposes and does not constitute an offer or solicitation for purchase or sale. Desjardins Group takes no responsibility for the consequences of any decision whatsoever made on the basis of the data contained herein and does not hereby undertake to provide any advice, notably in the area of investment services. The data on prices or margins are provided for information purposes and may be modified at any time, based on such factors as market conditions. The past performances and projections expressed herein are no guarantee of future performance. The opinions and forecasts contained herein are, unless otherwise indicated, those of the document’s authors and do not represent the opinions of any other person or the official position of Desjardins Group. Copyright © 2023, Desjardins Group. All rights reserved