- Randall Bartlett

Senior Director of Canadian Economics

Weekly Commentary

The Population Boom Is Masking Economic Gloom in Canada

September 8, 2023

It came as little surprise this week that the Bank of Canada dusted off its pause playbook and kept the overnight rate unchanged. For many of the reasons discussed in last Friday’s Weekly Commentary External link. This link will open in a new window., the Bank’s press release made clear that the central bank believes it’s done enough for now. We expect the Bank of Canada to remain on the sidelines for the foreseeable future to survey the impacts of past rate hikes as they continue to ripple through the economy. Indeed, we anticipate the Bank’s next move is likely to be a cut in the first half of 2024.

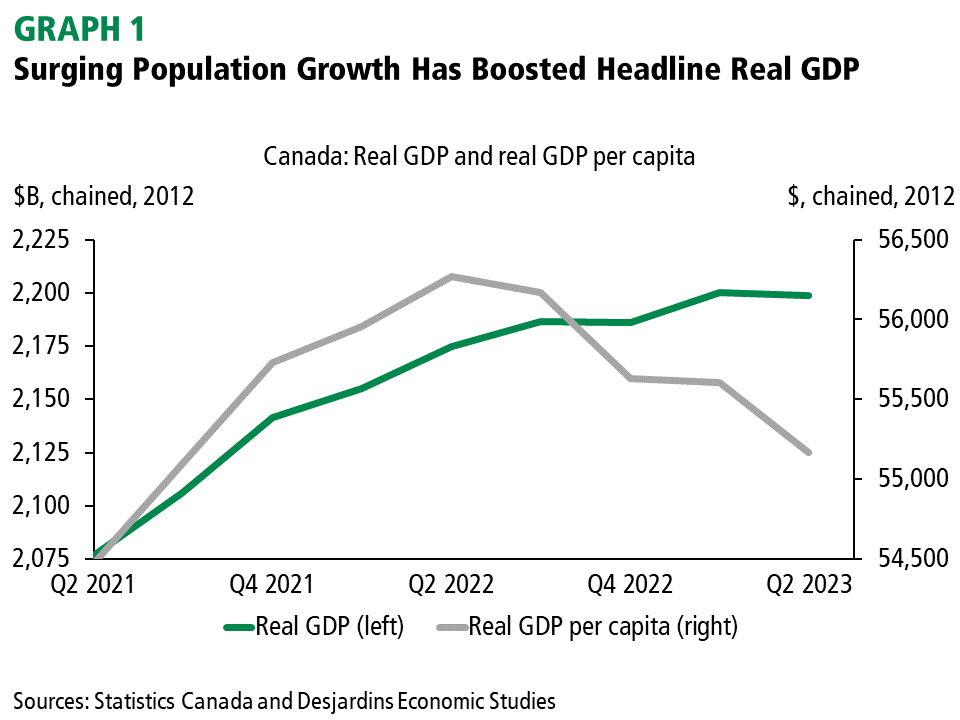

But while the Bank’s public statements have largely focused on the headline economic indicators—real GDP, employment and CPI inflation—looking at these numbers on a per capita basis where possible provides an even more downbeat picture of the Canadian economy. Starting with real GDP, while staccato moves over the past year have created a see-saw pattern of modest contractions followed by sharp accelerations, real GDP per capita has declined in each of the past four quarters (graph 1). Growth in domestic demand per capita has fared even worse. Not surprisingly, a lot of the weakness can be chalked up to a sustained drop in highly-interest-rate-sensitive residential investment. However, other sectors like consumption of non-durable goods (e.g., gasoline and food) and investment in machinery and equipment have also contracted consistently on a per capita basis. In contrast, growth in per capita spending on consumer durables has largely bucked this trend, thanks in large part to a jump in pandemic-delayed auto sales.

None of this is a coincidence. Surging population growth—the highest since the 1950s—has provided a tailwind to headline economic activity since mid‑2022. This is entirely driven by newcomers to Canada. And given newcomers’ need to purchase cars, home furnishings and the like, household expenditures have been boosted in a way that economists hadn’t expected as recently as a year ago and seemed to defy the gravitational pull of high interest rates.

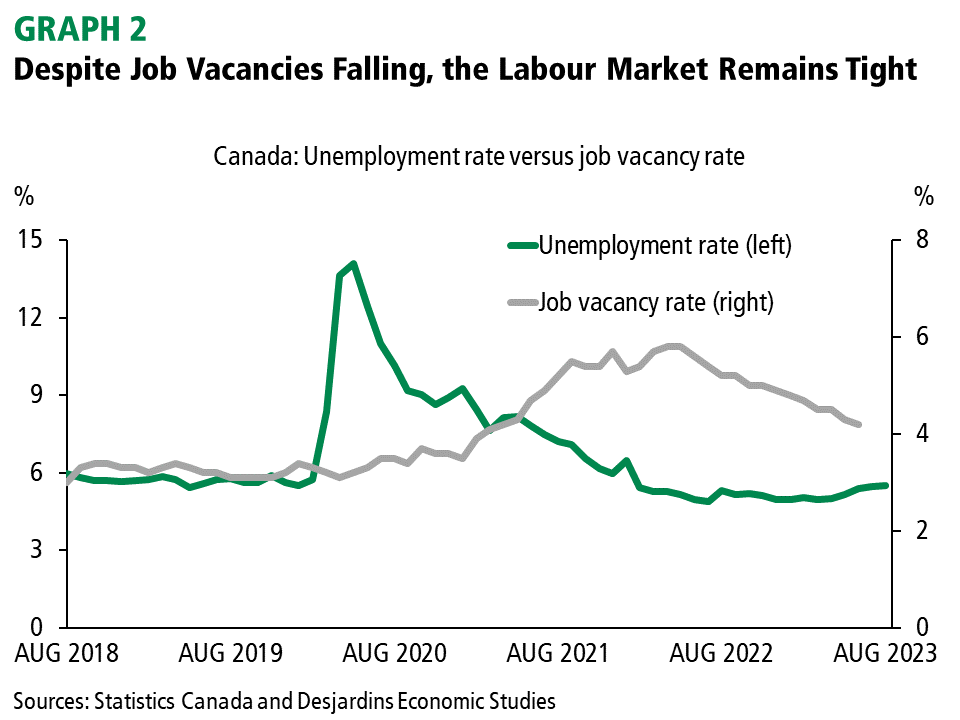

Importantly, this unprecedented number of newcomers primarily comprises non-permanent residents, such as temporary foreign workers and foreign students. Since many of these individuals came here to meet specific labour market needs, they have been able to quickly find work and earn an income. As a result, Canada’s unemployment rate has hardly budged from historic lows even as the job vacancy rate has gradually trended lower from the record highs reached last year (graph 2). This has supported elevated disposable income growth and a savings rate above the pre-COVID average despite high prices and interest rates having eroded household purchasing power.

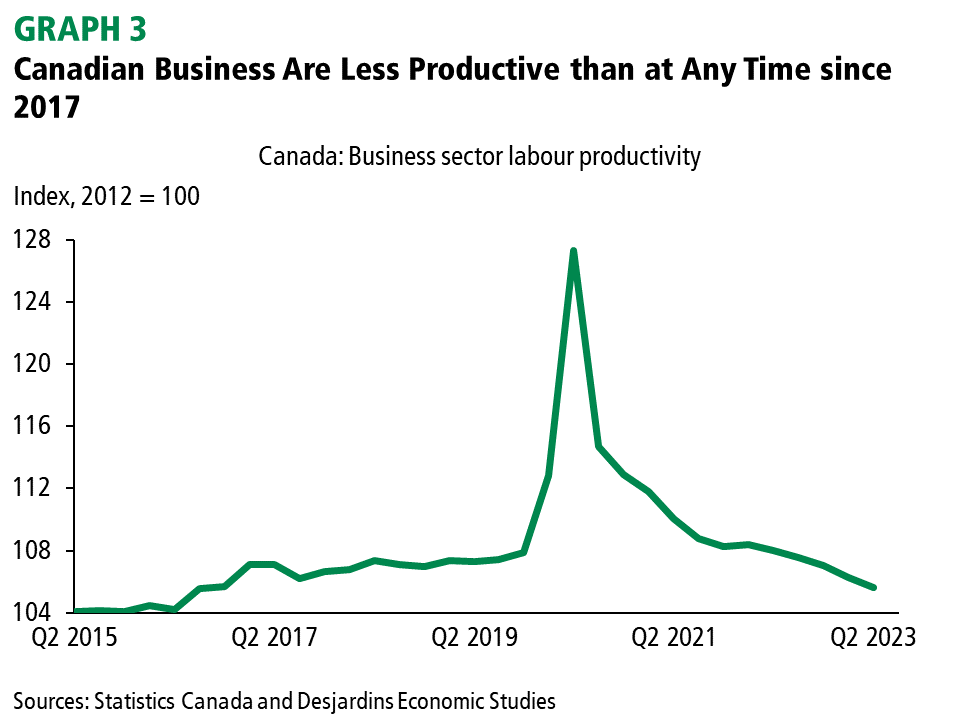

More alarming is the lack of business investment in Canada. While investment in non-residential structures has been supported by high commodity prices, capital expenditures on machinery and equipment have been very soft. Instead of investing in productivity-enhancing technology, it appears that businesses have been addressing labour shortages with temporary foreign labour. This has boosted hours worked in Canada but has pushed productivity consistently lower throughout the post-pandemic recovery. Indeed, the Q2 2023 data released earlier this week revealed that Canadian businesses are less productive now than at any point since 2016 (graph 3). And it doesn’t look like the situation is going to get better anytime soon. For instance, the Bank of Canada’s latest Business Outlook Survey showed the lowest investment intentions since 2020 for firms not tied to natural resource activity.

This moribund productivity performance is not new. As our recent research External link. This link will open in a new window. pointed out, anemic productivity growth is primarily responsible for Canada’s lacklustre real GDP per capita since 2014. A lack of capital expenditures in mining and oil and gas extraction due to low commodity prices and an uncertain long-term investment environment are largely to blame. But even as that sector has become more productive to preserve profitability, the rest of the Canadian economy has seen its productivity slide.

Looking ahead, souring sentiment suggests business investment isn’t likely to pick up anytime soon. Flagging consumer confidence portends a similar fate for household consumption. Given that a recession could begin any day, real GDP and domestic demand per capita can be expected to dip further, particularly if population gains continue apace. While falling labour demand on slumping sales is likely to prompt net non-permanent resident admissions to slow, it probably won’t be enough to alter the long-standing sluggishness in real GDP per capita in Canada. That will take an acceleration in Canadian productivity that has been sorely lacking for some time and shows little sign of improving.