- Kari Norman

Economist

Economic News

Canada: We May Be Starting to See a Thaw in the Housing Market

April 12, 2024

Highlights

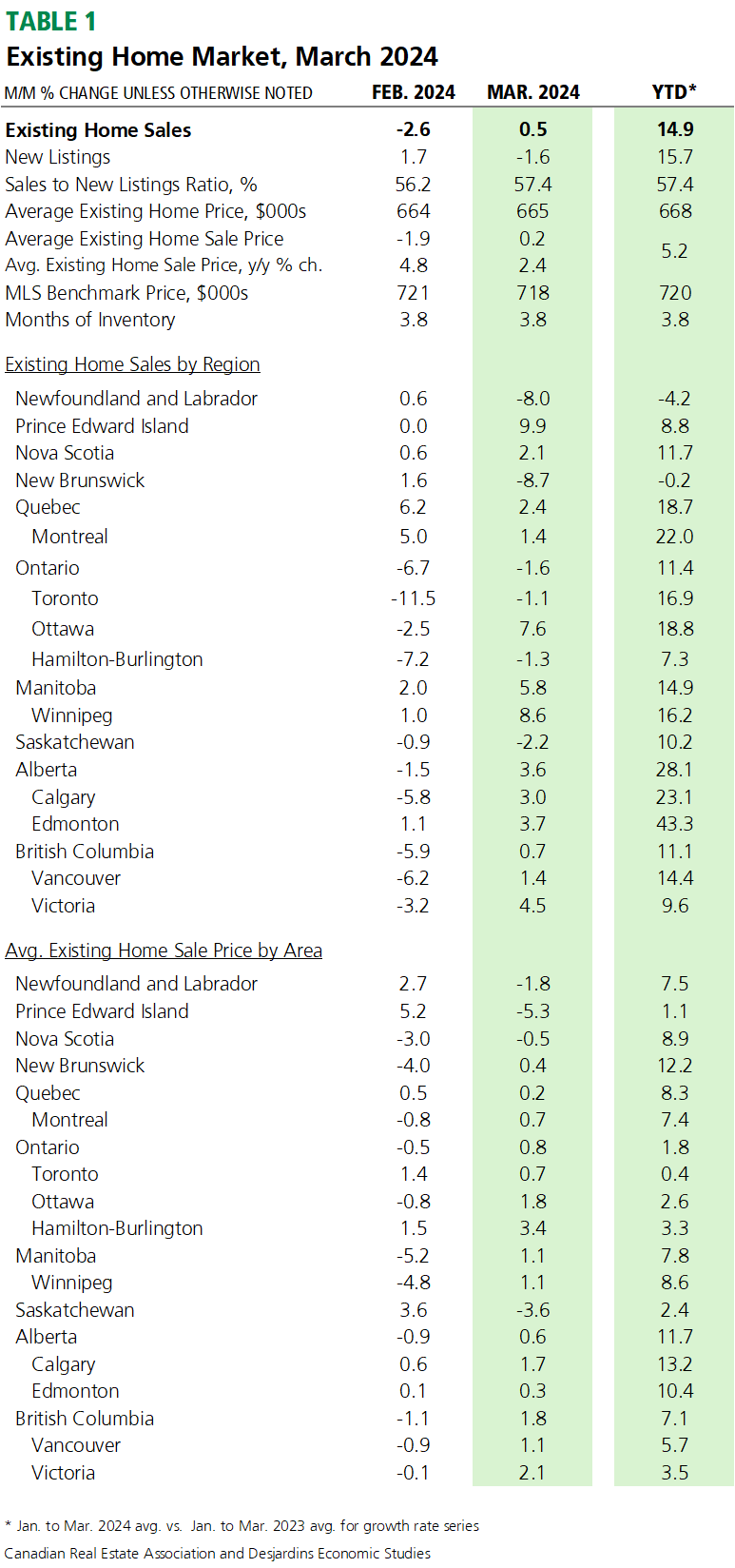

- Home sales in Canada rose by 0.5% in March 2024, after falling slightly in February. Table 1 below summarizes key data points.

- Our tracking suggests real annualized GDP growth in the range of 2.5% to 3% annualized in the first quarter of 2024. That’s in line with the Bank of Canada’s latest forecast of 2.8% published this week External link..

Implications

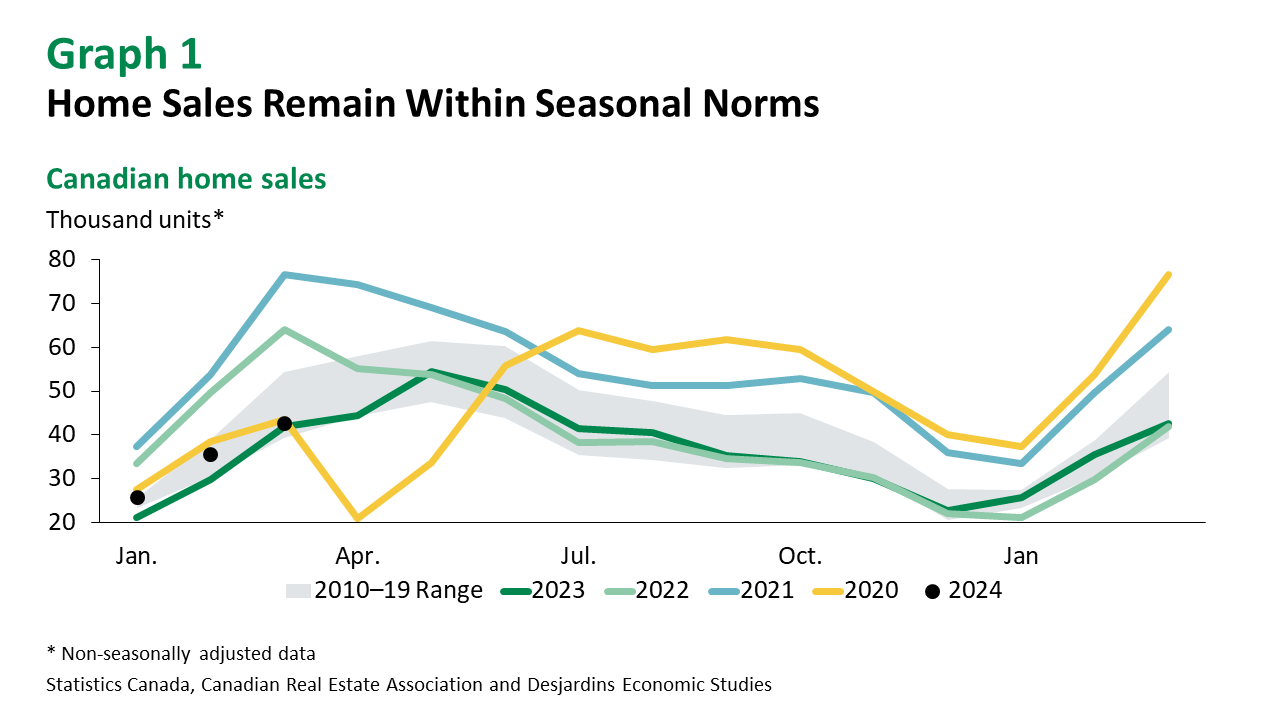

The frost may be starting to thaw in Canada’s housing market. Home sales in March were essentially flat—an improvement from the drop in February—but remain within seasonal norms (graph 1). At the same time, national average and benchmark prices remained little changed. This likely reflects a mix of economic factors. On the one hand, the easing of inflationary price pressures coupled with recent wage gains has begun to restore purchasing power. The labour market also remains relatively healthy, despite a modest setback recently. On the other, anticipated lower mortgage rates may be keeping potential buyers on the sidelines.

The Government of Canada announced a basket of new measures External link. yesterday with the hopes of improving affordability, particularly for young first-time homebuyers. These include increasing the amounts they can withdraw from RRSPs under the Homebuyers’ Plan as well as extending the grace period to five years before they need to start repayments. The announcement also included that first-time homebuyers of newly-built homes will be permitted to have a 30-year amortizations. And amortization relief will be made available to existing homeowners to reduce their monthly mortgage payments, which should be good news to owners who fear they might be forced to sell at mortgage renewal time. This followed a deluge of other measures announced since the end of March meant to improve housing affordability in Canada.

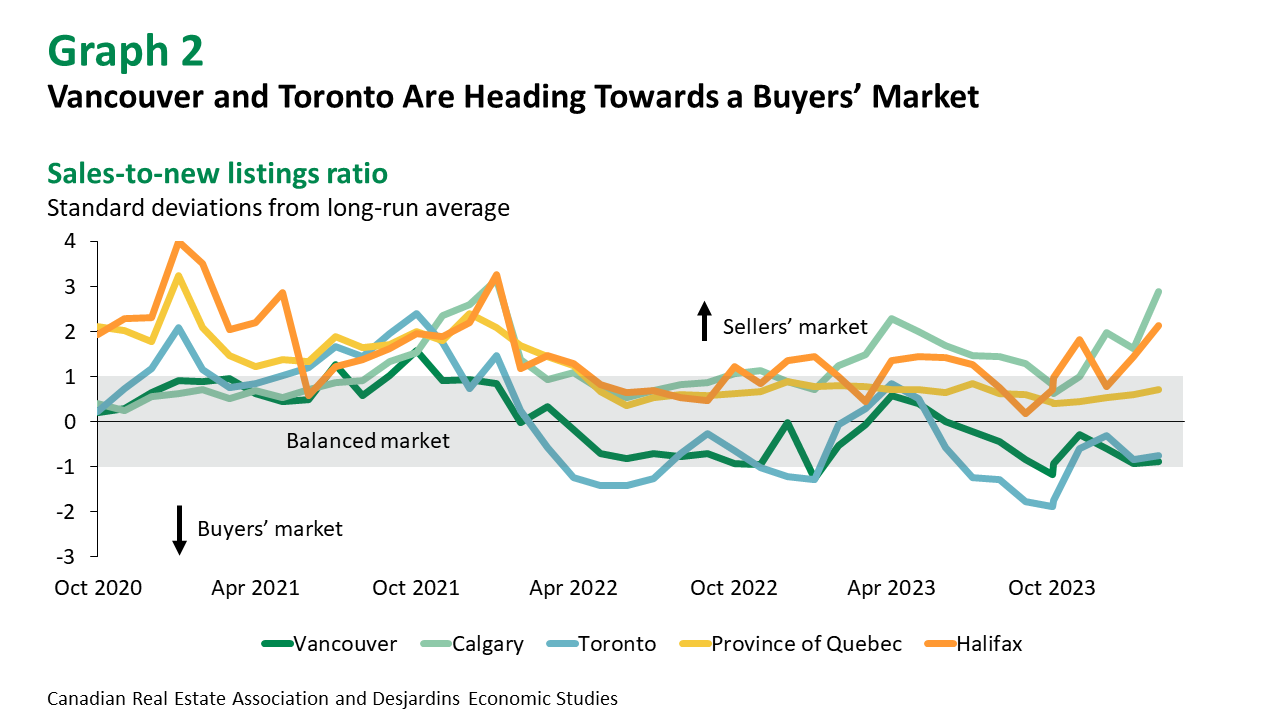

On a regional basis, the impact of these national trends has been notably diverse. Toronto has experienced declining sales over the past two months (seasonally adjusted), while Vancouver bounced back in March after a decline the prior month. Regardless, both are flirting with buyers’ market territory (graph 2). Montreal has had the highest sales growth in the first three months of this year of all the large cities we cover. At 22.0% over the same period a year ago, it best the 16.9% and 14.4% in Toronto and Vancouver, respectively.

New listings remain an indicator to watch. After two months of increases, new listings pulled back slightly in March by 1.6%. Time will tell whether this reflects prospective sellers waiting for mortgage rates to fall in the hopes of seeing increased buying activity.

We remain of the view that the Bank of Canada will begin cutting rates in June, further enhancing affordability which could stimulate demand. But given the pickup in home sales following the pause in monetary policy tightening in early 2023, the BoC will be watching carefully to avoid a repeat this year.