- Marc Desormeaux

Principal Economist

Economic News

Canada: Labour Market Shows Some Cracks

June 9, 2023

Highlights

- Net total Canadian employment fell by about 17k in May 2023, with a 77k plunge in youth employment offset by gains for the prime-working age population.

- A 33k decrease in full-time employment was partly offset by a 16k gain in part-time positions.

- Job losses were concentrated in the services industries. Leading total employment weakness were business, building, and other support services (-31k), and professional services (-13k). The goods sector fared better, with a notable 13k gain in manufacturing.

- The unemployment rate edged 0.2% higher to 5.2%—still near all-time lows—but the participation rate was incrementally lower at 65.5%.

- Total hours worked fell by 0.4% in May but were up more than 2% versus year-earlier levels. Hours fell more in services (-0.6% m/m), which is where the Bank of Canada hopes to see some moderation in economic activity.

- Advances in hourly earnings of permanent employees—important for the Bank of Canada in its assessment of wages’ inflationary impacts—remained above 5% y/y. However, on a three-month annualized basis, hourly wage growth came in at only 2%. This measure has hovered between 2% and 3% in the last three months, which suggests that the year-over-year measure should slow further in the second half of the year.

- Ontario (-24k) accounted for most of the layoffs; Nova Scotia and Newfoundland and Labrador also experienced meaningful losses. Alberta and British Columbia reported little change in total employment despite the effect of severe wildfires in May.

It’s one month of data and hardly the magnitude of weakness one might expect following rapid and aggressive rate hikes, but May’s report did show some cracks in the labour market. It was the first net employment loss in nine months, with layoffs concentrated in full-time positions. Another highlight was the 0.4% drop in hours worked, with the dip concentrated in interest rate-sensitive services industries like real estate and construction.

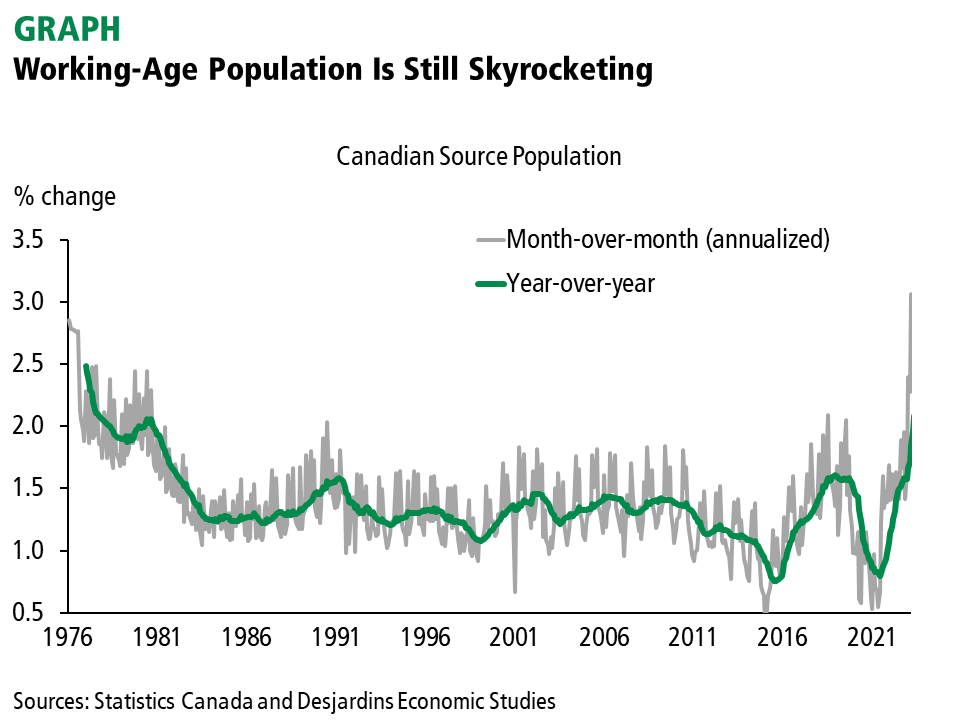

Source population growth reaccelerated in May to reach a new record (graph). This pushed the employment rate 0.3 percentage points lower. We think the recent employment surge at least partly reflects immigrants and net non-permanent residents filling job openings that became available over the course of the pandemic.

Implications

This was the second employment release of the second quarter, and it leaves our estimate of Q2 2023 real GDP growth at almost 2% (q/q annualized). That is better than the 1% penciled in by the Bank of Canada in its last Monetary Policy Report. So, despite an employment slowdown in May, the print does not change our call for another 25bp hike at the Bank’s July meeting.

Record rates of population growth adds a wrinkle to the central bank’s rate calculus. On the one hand, labour supply is increasing, which is working to ease labour market tightness. On the other, the boost to economic activity from population growth seems to have been ramping up just as the Bank intended to pause rates and expected inflation to drift lower.

Comments