- Randall Bartlett

Senior Director of Canadian Economics

Economic News

Canada: Lower April Inflation Supports a June Rate Cut

May 21, 2024

Highlights

- Headline CPI rose 2.7% y/y in April, in line with economists’ expectations. Prices rose 0.5% m/m, but only 0.2% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Implications

Another month, another CPI inflation print that came in at or below the expectations of economists. Total inflation has now been within the Bank of Canada’s 1% to 3% target range for four consecutive months—the first time that’s happened since the disinflationary days of late-2020, early-2021. Slowing momentum in the year-over-year price growth of food purchased from stores (1.4%); household operations, furnishings and equipment (-2.1%); and clothing and footwear (-2.6%) all played a role. Indeed, even the normally cautious Statistics Canada went so far as to characterize the release as a “broad-based deceleration in the headline CPI.”

Despite this good news, growth in shelter prices (6.4% y/y) continues to drive overall CPI inflation (graph 1). Excluding shelter, inflation is tracking just 1.2% and has been below the central bank’s 2% target for most of the past seven months. High and rising shelter costs, combined with the recent increase in gasoline prices (6.1%) on the back of higher oil prices, continues to put strain on the household finances of Canadians.

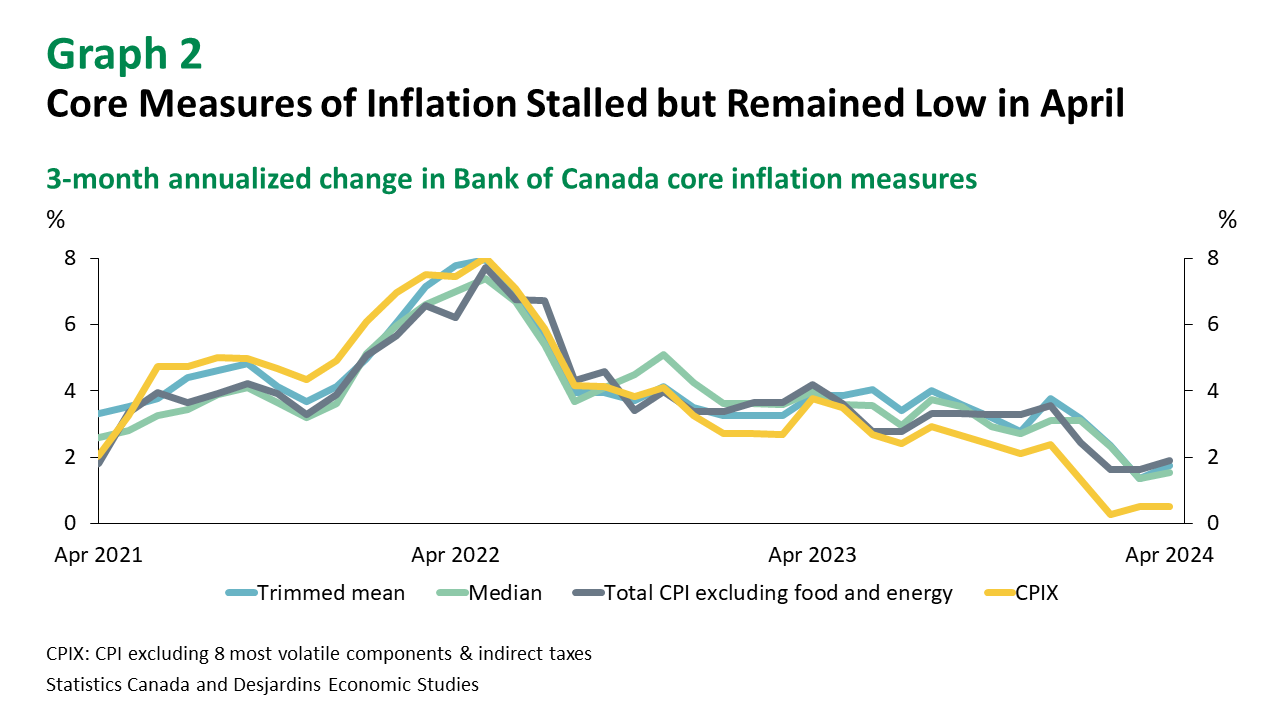

Turning to underlying inflation, the Bank of Canada’s preferred measures of core year-over-year price growth—CPI median and trimmed mean—decelerated again in April and are now both below 3%. But on a 3-month annualized basis, these measures reaccelerated on average by 0.2 percentage points to reach 1.5% and 1.8%, respectively (graph 2). Looking to the more universally referenced total CPI inflation excluding food and energy, inflation on a 3-month annualized basis rose three ticks to 1.9% in April. Finally, growth in the Bank’s former preferred measure of core inflation—CPIX (CPI excluding the 8 most volatile components & indirect taxes)—was unchanged at 0.5% when calculated the same way, under 2% for the fourth consecutive month. While this reprieve in the near-term disinflationary momentum seen recently may raise eyebrows, the fact that these measures were below the Bank’s 2% target remains a positive sign that price growth is headed in the right direction.

At 2.7% y/y, headline inflation in April came in well below the Bank’s forecast of 2.9% for Q2 in the April 2024 Monetary Policy Report. Most measures of underlying inflation are now comfortably under 3% as well. At the same time, real GDP growth is also tracking below the Bank’s most recent forecast to start 2024 (see our latest Economic and Financial Outlook External link. for more information). And on a per capita basis, economic activity looks even worse. Taken together, these economic indicators help to reinforce our call that rate cuts are likely to begin at the Bank of Canada’s upcoming June interest rate announcement.